Download

1 / 3

90 likes | 523 Views

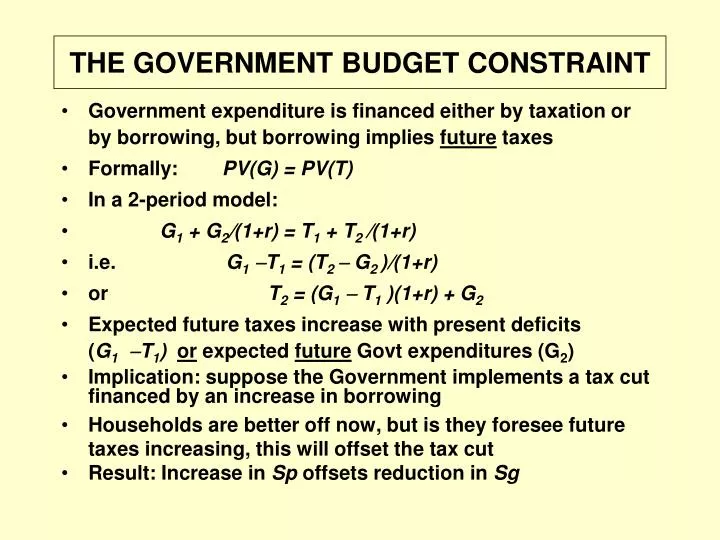

THE GOVERNMENT BUDGET CONSTRAINT. Government expenditure is financed either by taxation or by borrowing, but borrowing implies future taxes Formally: PV(G) = PV(T) In a 2-period model: G 1 + G 2 (1+r) = T 1 + T 2 (1+r)

E N D

THE GOVERNMENT BUDGET CONSTRAINT • Government expenditure is financed either by taxation or by borrowing, but borrowing implies future taxes • Formally: PV(G) = PV(T) • In a 2-period model: • G1 + G2(1+r) = T1 + T2 (1+r) • i.e. G1T1 = (T2 G2 )(1+r) • or T2 = (G1 T1 )(1+r) + G2 • Expected future taxes increase with present deficits (G1T1)or expected future Govt expenditures (G2) • Implication: suppose the Government implements a tax cut financed by an increase in borrowing • Households are better off now, but is they foresee future taxes increasing, this will offset the tax cut • Result: Increase in Sp offsets reduction in Sg

RICARDIAN EQUIVALENCE (1) • More realistically suppose a very large increase in the Government deficit is expected in the next 4 years • Rationally, households expect large tax increases and reductions in future disposable income. • Result: possible large increases in Sp, which of course will reduce government revenue from expenditure taxes, etc…. • Recent developments: USA; Ireland where Sg has turned strongly negative, but Current a/c deficit of BOP has reduced significantly: implication Sp must have increased (Sp + Sg = BOP) • The Barro-Ricardo equivalence theorem throws doubt on the efficacy of discretionary fiscal policy. • While there are some historical episodes which might support it there are also severe doubts:

RICARDIAN EQUIVALENCE (2) • Are government bonds net wealth? No, if Barro is right. • But do people discount the future at a higher rate than the long-term bond rate? If so, then the theorem falls • Empirically there are doubts: e.g. US tax cuts in the 80s and 2000s have been associated with reduced personal savings, contrary to the theorem (assuming unchanged government expenditures and hence larger deficits, people should have expected future tax increases and saved more in the present…) • However the Irish fiscal correction of the late 80s was not accompanied by the deflation feared by some: did private consumption and investment expand in response to lower expected taxes and higher expected disposable incomes?