Download

1 / 5

50 likes | 50 Views

DK Goel Solutions Class 11 Chapter 14 Trial Balance and Errors as per latest DK Goel Book available for free. Download Now<br><br>https://dkgoelsolutions.com/class-11/chapter-14-trial-balance-and-errors/

E N D

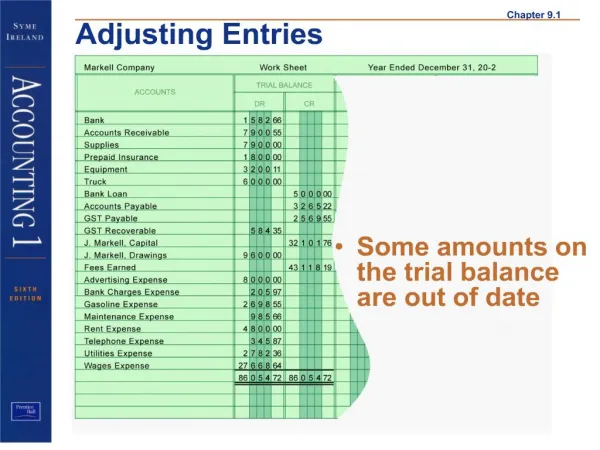

DK Goel Solutions Class 11 Chapter 14 Trial Balance and Errors DK Goel Accountancy Class 11 Solutions Chapter 14 Trial Balance and Errors, which is laid out by master Accountancy instructors from the most recent form of DK Goel Class 11 Accountancy books. We, at Dk Goel Solutions help students to fathom every one of the hypotheses, specifically. There are various ideas in Accountancy, however the ideas of Trial Balance, Depreciation and Bank Reconciliation Statement (BRS) are required. DK Goel Solutions Class 11 – Chapter 14 Question 1: What is a Trail Balance? State any four functions of a Trail Balance. Solution 1: Trail Balance is a statement showing the balances, or total of debits and credits, of all the accounts in the ledger with to verify the arithmetical accuracy of posting into the ledger accounts.

(i) Ascertain the Arithmetical Accuracy of Ledger Accounts: The purpose of preparing a trial balance is to ascertain whether all debits and credits are properly recorded in the ledger or not and that all account have been correctly balanced. (ii) Help Prepare the Final Accounts: when the trail balance does not tally, we know that at least one error has occurred. The error may have occurred at one those stages in the accounting process like totalling of subsidiary books, posting of journal entries in the ledger, calculating account balances, carrying account balance to the trial balance and totalling the trial balance columns. (iii) Summary of Each Account: The Trial Balance contains the Ledger summary. The Ledger can only have to be listened to when further evidence is needed in relation to an account. (iv) To Help in Locating Errors: The Trial Balances help to find mistakes in the work of record keeping. It should, however, be held in mind that not all the mistakes in Record Keeping are revealed, but only the arithmetical inaccuracies. Question 2: Trail Balance is a link between ledger and final accounts. Solution 2: At any time, at the end of a month, quarter, half-year, or year, a trial balance can be prepared. It is usually prepared at the close of the accounting cycle to validate the arithmetical consistency of the records in the ledger before the actual accounts are prepared. It should be noticed that it is often cooked on a specific date and not for a specific time. Solution 3: 1. Errors of Principle:- Where the accounting principle is broken while a transaction is registered, it is considered a principle mistake. For instance, instead of the machinery account, the purchase of machinery is debited to the purchase account. 2. Errors of Omission:- There will be no effects on the trail balance where a transaction has been overlooked to report. If all parts of a transaction go unrecorded and despite being registered in the main entry books, a transaction is not posted in the ledger at all. Purchases of Rs. 20,000, for instance, were excluded from being posted in the purchase day book. Question 4: Give two examples of compensating errors. Solution 4: 1.) Goods sold to Mr. Kunal amounted Rs. 6000/- was recorded to the debit side of Mr. Kunal’s account by Rs. 600/- 2.) Commission account overcast by Rs. 2,000 and Electricity bill under cast by Rs. 2,000. Question 5: What is meant by error of omission? Give any one example.

Solution 5: An error of omission is named whether a transaction lies unrecorded in the journal or subsidiary books. For instance:- Rs. 20,000 sales skipped to be posted in the daily book of purchases. Question 6: What is error of principle? Give two examples. Solution 6: Where the accounting principle is broken while a transaction is registered, it is considered a principle mistake. For Instance: 1. Machinery purchase is debited to the account of purchase instead of the Machinery Account. 2. Instead of a furniture account, purchases of old furniture are attributed to a sales account. Question 7: Name four errors which cannot be disclosed by preparing a Trail Balance. Solution 7: Below are the errors cannot be disclosed by preparing a Trail Balance:- 1. Compensatory Errors 2. Error of Duplication 3. Errors of Principle 4. Errors of Omission Question 8: What is a suspense account? When is it opened? Solution 8: An account in which the disparity is held in the trail balance before errors are found and rectified. And where the trail balance does not tally, it encourages the planning of financial statements. Question 9: On which side of the Trail Balance, the following Ledger balances will appear:- i. Purchases Return ii. Furniture iii. Bank Loan iv. Discount allowed v. Capital vi. Drawings vii. Return Inwards viii. Bills Receivables

Solution 9: Debit Balance (ii) Furniture (iv) Discounts Allowed (vi) Drawings (vii) Return Inwards (viii) Bills Receivable Credit Balance (i) Purchases Return (iii) Bank Loan (v) Capital Question 10: State whether the balance of the following accounts should be placed in the debit (or) the credit columns of the Trail Balance: i. Plant and Machinery ii. Discount Allowed iii. Bank Overdraft iv. Sales v. Interest Paid vi. Bad Debts Solution 10: Debit Balance (i) Plant and Machinery (ii) Discount Allowed (v) Interest Paid (vi) Bad Debts

Credit Balance (iii) Bank Overdraft (iv) Sales Also read - Dk Goel Solutions Class 12 Download Free study materials for your Examinations at DK goel Solutions