Download

1 / 10

110 likes | 839 Views

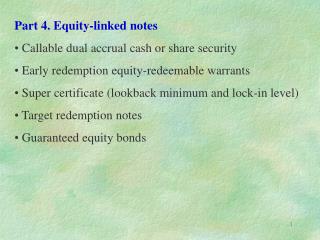

Private Equity – A case study June 24, 2008 Contents Typical investment / operating structure Outline of the structure Income-tax issues Analysis Conclusion Typical investment / operating structure US based Fund Manager US investors Non-US investors GP Company 100%

E N D

Private Equity – A case study June 24, 2008

Contents • Typical investment / operating structure • Outline of the structure • Income-tax issues • Analysis • Conclusion

Typical investment / operating structure US based Fund Manager US investors Non-US investors GP Company 100% Cayman Islands Fund Investment management agreement 100% Mauritius Company Investment advisory agreement Invest in shares of Indian Cos Outside India In India Indian Co 1 Indian Co 2 Indian Co 3 Indian advisory company

Outline of the structure • Offshore investors invest in a Cayman Islands Fund (‘CIF’) • CIF established to make investment in growth companies across geographies (including India). For this purpose, the CIF invests in a Mauritius based subsidiary (‘M Co’) which in turn makes investment in shares of Indian companies and other companies in the Asia Pacific region • A US-domiciled Fund management company (‘FMC’) is appointed to manage the investments of CIF and M Co • The FMC establishes an Indian sub-advisory company (‘IAC’) for provision of investment advisory and incidental support services in respect of potential Indian investments • Decisions to make investments in Indian companies are taken by the Board of Directors of M Co based on recommendations received from investment committee constituted in M Co. Investment committee considers investment recommendations from FMC. Investment committee comprises of individuals with necessary expertise in considering and evaluating investment opportunities

Outline of the structure (contd…) • The IAC broadly provides the following services to FMC on a non-discretionary basis: • Undertake research and identify potential investment targets • Make non-binding recommendations to FMC as to the purchase/ sale of investments by M Co • Assist in negotiating purchase and sale of Indian investments • Act as an interface in India with external consultants (including securities firms, investment consultants, investment banks, financial institutions, solicitors and accountants) in relation to investments • Assist in review of agreements relating to acquisition/ sale of shares and other agreements • Send periodic reports on the performance of the investee companies on a regular basis

Income-tax issues • Whether IAC constitutes a permanent establishment (‘PE’) in India of FMC/M Co? • Even if IAC constitutes a PE of M Co, can capital gains earned by M Co from divestment of shares of Indian companies be liable to tax in India?

Analysis Permanent Establishment • Fixed Place PE: • There must be a place of business in India, for example, any office space (owned or rented) • The place of business must have a degree of permanence • Agency PE: • An agent of a non-resident acts in India • The agent is dependent legally and economically on the non-resident principal • The agent has and habitually exercises in India, an authority to negotiate and conclude contracts for or on behalf of the non-resident principal Capital Gains (India Mauritius tax treaty) • Capital gains from the alienation of movable property forming part of the business property of a permanent establishment may be taxed in India • Capital gains earned from the alienation of Indian securities (other than the above), shall be taxable only in Mauritius

Conclusion The following supports the argument that IAC should not constitute a PE of the FMC/M Co in India: • IAC’s premises not at disposal of the FMC/M Co. Hence, IAC cannot constitute a fixed place PE of the FMC/M Co [Ericsson, Motorola and Nokia ruling (95 ITD 269) Delhi ITAT SB] • IAC represents FMC/M Co vis-à-vis third parties in India. Therefore, IAC will be regarded as an agent of FMC and/or M Co • IAC could be subject to detailed instructions and control with respect to the conduct of its business. Therefore, IAC is potentially legally dependent • IAC is setup as a risk free capital service provider in India. Therefore, the entrepreneurial risks are borne by the enterprise that IAC represents in India. Thus, IAC is economically dependent • IAC cannot therefore be regarded as an agent of independent status • IAC has no authority (express or implied) to negotiate and conclude contracts on behalf of the FMC/M Co • Thus, it will not constitute a agency PE of FMC/M Co [DIT v Morgan Stanley & Co (2007) 292 ITR 416 (SC)]

Conclusion • If IAC constitutes an agency PE of M Co in India on the basis that it has and exercises an authority to conclude contracts on behalf of M Co, gains earned by M Co on divestment of Indian securities should still not be subjected to tax in the hands of its PE in India due the following reasons: • The Indian securities are beneficially owned by M Co • The risk arising from the price fluctuations of the investment is borne by M Co • The funding for making the investment is made by M Co out of its own or borrowed capital • Therefore, the Indian securities do not form part of the business property of the IAC (ie PE of M Co). • Hence, the gains arising on sale of investments should not be taxable in India.