Analyzing U.S. Economy Recovery & Challenges Post-Crisis

Explore key themes impacting the U.S. economy post-crisis, including recovery strength, inflation, employment, and debt. Dive into housing, consumption, GDP growth trends, and the impact of speculative episodes. Understand the shift in household spending and debt dynamics, government interventions, and the need for long-term economic adjustments. Analyze industrial production, non-manufacturing sector trends, retail sales, and exports in relation to the overall economic recovery. Discover the complex interplay of factors influencing the U.S. economy's recovery path.

Analyzing U.S. Economy Recovery & Challenges Post-Crisis

E N D

Presentation Transcript

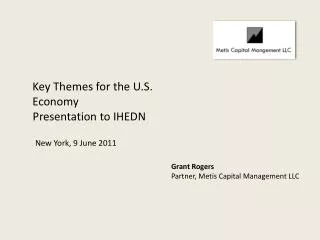

Presentation to IHEDN Key Themes for the U.S. Economy New York, 9 June 2011 Grant Rogers Partner, Metis Capital Management LLC

Key Themes for the U.S. Economy • How Strong is This Recovery? • Inflation • Employment • Debt

Recovery: How Strong? • Not as strong as previous, classic recoveries. Unlike traditional economic recessions, this is a financial crisis, meaning that “deleveraging” taking place in the economy will elongate the recovery cycle. • Wall Street economists are now downgrading prospects for growth in the U.S. GDP growth was 1.8% in the first quarter, and economists foresaw that number picking up to the 3% range in the 2nd quarter. However, manufacturing is beginning to slow, the housing market is still weakening, consumption in the U.S. is weak, and unemployment is not improving. Estimates for 2nd quarter growth are now being revised down to 2%, not enough to improve unemployment. • Housing: U.S. home prices are in a “double dip” and have erased any gains since the recession began • Consumption: Consumption represents roughly two-thirds of the American economy. Food and fuel prices slowed consumption in the first quarter.

Recovery: How Strong?GDP Growth • Recessions following speculative episodes traditionally are substantially worse than after non-speculative episodes. Reviewing US history, this appears to be true over the last 140 years, where income levels went down by 6% following speculative episodes that resulted in financial crises, as opposed to only 1% for non-speculative periods. (This figure strips out the Great Depression, or it would be considerably worse). • Recoveries after speculative episodes tend to be stronger than after non speculative ones. Using the same time period, income rose by 7.1% for the former and by only 2.4% in the latter case. • The current recession/recovery is notfollowing this pattern; it is much weaker because the government stimulus put in place to cushion the recession (government spending, tax cuts, and monetary stimulus) stopped the recession from being as bad as it "needed to be". Let’s examine household spending and household debt: • Spending increased during the boom - from about 83% of income in 2000 to about 87% by 2005 and currently about 86% This meant "savings" (or what's left over after taxes and spending) went way down and debt went way up • The aftermath of the financial crisis was about household adjusting spending downwards and savings upwards to deleverage and pay down debt • Unfortunately, lower spending = recession (which is painful) • The government stepped in to help cushion the recession. They cut taxes which allowed households to increase savings (start paying down their private debt) without a big cut in spending. • But the debt burden was simply transferred over from households to government (which eventually comes back to households anyway) so that the debt is still hanging over us all which puts a damper on spending and investment. • Before we can have sustained long-term growth we need to have a substantial adjustment of spending downwards to a level where households are comfortable long-term - maybe from 86% of income to 83% of income. Unfortunately this means either another short and sharp recession or, as seems to be happening, a long period of mediocre growth. • The aftermath of a speculative crisis is about two things: liquidity crisis and re-adjusting behavior • We had the liquidity crisis and this time (unlike in 1930) the Fed did the right thing and averted disaster with the big liquidity injection of QE1 • We have not had the adjustment of behavior - household spending as percent of income is still high (85.5%).

Industrial Production Beginning to Decline U.S. industrial production was at multi-decade highs, due to a weak dollar, but slowed in May to 53.5 from 60.4 in April. Readings above 50 indicate expanding activity. June 30 will see the end of the Fed’s fiscal stimulus (QE2) at which time the dollar may begin strengthening, which may have a negative effect on the manufacturing sector.

But Adjusted For Population Growth and Inflation, and Stripping Out Gasoline, A Different Picture Emerges…This chart would suggest that the recovery is weak and may be stalling Source: Dshort.com, St. Louis Fed, Consumer Price Index.

Exports Are Climbing, Helped by a Weak DollarU.S. growth is being driven by exports, and the chief beneficiaries are multinational companies like Caterpillar, G.E., or Intel. Since the recovery started in the third quarter of 2009, exports have contributed about 1.4 percentage points to the nation's 3.0% annualized growth rate. Exports benefit from a lower U.S. dollar, but this is not necessarily helping small companies of 250 people or less, which employ half the country. Furthermore, a lower dollar places a heavy burden on the U.S. consumer, who relies on imported goods which are now more expensive.

Employment Improving, Yet Still Very Weak…Source: Bureau of Labor Statistics

But Statistics can be Misleading…… • Employment is still down by 6.5 million from its 2007 peak • While at the same time, the work age population has increased by 6.5 million. • The U.S. unemployment numbers do not measure unemployed who are “underemployed”, or who have been looking for more than a year. • “Underemployment “ rate was 19% in 2010, highest in Illinois, California, and Michigan.* *Source: Gallup

The “Real” Unemployment Rate Alternate Unemployment Charts • The chart below, by Shadow Government Statistics (SGS), attempts to measure “underemployed” plus long-term discouraged workers, who were defined out of official existence in 1994. • The U-3 unemployment rate (in red) is the official monthly headline U.S. unemployment number. • The U-6 unemployment rate is the Bureau of Labor Statistics’ (BLS) broadest unemployment measure, including short-term discouraged and other marginally-attached workers as well as those forced to work part-time because they cannot find full-time employment. • The SGS Alternate Unemployment figure adds their estimate of long term discouraged workers back in to the statistic.

Housing • House prices are now 33% below their peak in 2006, which is a larger fall than the 31% drop recorded during the Great Depression. • U.S. home prices fell 4.2% in the first quarter of this year, after a fall of 3.6% in the fourth quarter of last year. Traditionally, the spring is the strongest period for housing transactions. In April, however, the pending home sales index fell by 11.6% from its March level. • At the end of 2010, 23% of all mortgage borrowers were “underwater”, meaning that their homes were worth less than what they owed. • If house prices fall another 5% that number will increase to 28%. If house prices fall 10% from here, more than one third of all U.S. borrowers will be underwater. • Falling home prices slow economic growth, because people spend less when from this “negative wealth effect”. Furthermore, if underwater borrowers are stuck in a home that is worth less than they owe, they become immobilized in regions which are often economically depressed (Florida, California, Michigan). • There are now a record 2.2 million homes foreclosed and owned by banks. There are an additional one million homes in the foreclosure process. It will take years to remove this inventory. Banks tend to cut prices in order to quickly sell foreclosed properties. • Banks have been hit with sweeping penalties by regulators for improper home-foreclosure practices. Accordingly, many banks have stopped foreclosing on homes until their procedures are improved. Were it not for this, foreclosures would be considerably higher. Conclusion: Home prices will continue to fall substantially, with corresponding “negative wealth effect” on consumers.

Quantitative Easing, Part One Quantitative easing is an unconventional monetary policy used by central banks to stimulate their economy when Conventional monetary policy has become ineffective. The central bank buys government bonds and other types of bonds, with new money that the bank creates electronically in order to increase money supply and the excess reserves of the banking system. This action also raises the prices of the financial assets bought, which lowers their yield. Quantitative easing shifts monetary policy instruments away from interest rates, towards targeting the quantity of money. In the mid 1990’s, there was an increase in productivity linked to • Computers • An increase in global trade • The integration of China into the global economy (Cheaper goods from China was an increase in productivity). U.S. consumers mistook that increase in productivity. They overestimated how large the increase in future productivity and income would be. Consumption and debt rose accordingly relative to income, while savings rates went down dramatically. There had to be a readjustment. With the credit crisis, there was the appearance of a readjustment, whereby the savings rate went from around 2% to 6% Between 2007 and 2010. However, this adjustment was due almost entirely to a decrease in taxes, not a decrease in savings. In other words, up until 2008, household debt increased dramatically, until the 2008-2011 period when government debt took over. This represents a transfer of debt from households to government, but amounts to the same thing. Nothing has really changed since 2008 households are still spending, and not investing much. At some point, there will be another crisis.

Quantitative Easing, Part One The crisis might be blamed on former Fed chairman Greenspan for keeping “real” interest rates negative in the 2003-2005 periods. But whoever is to blame, the resulting policy response by the Federal Reserve was without historical precedent. The first major policy response came to be known as “Quantitative Easing”, which involved the Federal Reserve Bank buying treasury bonds with electronically created money. Banks absorbed this liquidity provided by the Fed, willingly. In fact, they wanted to hold reserves at the Federal Reserve, because they thought it was safe. Usually, a bank takes one dollar of deposits and lends out 9 dollars. This is called the reserve ratio. The reserve ratio during the credit crisis went from 9:1 to 1:1. In other words, for every dollar of deposits, banks were only willing to lend out only one dollar. This fact was largely missed by the media, because it was one of the most extraordinary changes in the banking landscape in the past 200 years. Individuals, companies, and banks ALL wanted cash, because it was considered a safe way of storing wealth. Demand for cash increased to record levels, and it led to deflation in 2008 and 2009. Prices and inflation are a balancing act between the supply and demand for money. If the demand for cash explodes, what happens if you don’t add supply? You get deflation because the demand for money goes up relative to the supply of money. An excess of money meant that there were more dollars per unit of things to buy.

Quantitative Easing, Part One • The first round of quantitative easing was simply an effort to keep up with the demand for money. One of the great lessons of the Great Depression was that when money is in great demand, if money is not supplied to meet that demand, the result is deflation. ……(Bernanke speech of 2001). • So banks were interested in holding their reserves at the Federal Reserve out of fear, and this represented a major change in their behavior. But there was another change happening at the time. In late 2008, the Fed began paying interest on these reserves. In the past, banks never received any interest on these reserves, and were therefore uninterested in keeping any money there because it represented a large opportunity cost. So the cost of holding reserves at the Fed changed as well as the desire to hold reserves there. Quantitative Easing 1 was an answer to this change in behavior and cost. • Banks now want to hold higher levels of reserves, which is a change in behavior which will be with us for some time.

Quantitative Easing, Part Two Quantitative Easing II, on the other hand was something completely different. Whereas in QE1 the Fed acted as a monetarist should, QE2 was a Keynesian exercise. By the end of 2010, the demand for money was coming down because the level of panic in the U.S. and worldwide was subsiding. In November of last year, the Fed decided to purchase another $600 billion of treasury securities. The supply of money was now increasing significantly, and this is inflationary. The second round of quantitative easing was intended to increase consumer demand for goods and services by increasing money supply. A monetarist would say that this will simply lead to inflation. QE2 really should have had a different name from QE1. The Fed thinks that when inflation begins, they will be able to drain liquidity quickly enough to stop it. They feel they will be able to counter rising inflation by: • Raising interest rates • Selling the bonds they hold, taking in cash and withdrawing money from the economy. There are three problems with this however. • One is that inflation may get started and last 2 years or more before it is contained, and, • Its difficult to tell how much inflation there is, and how much liquidity you need to drain from the system. Economics is a very inexact science, and there is a great deal of uncertainty here. • The third problem is political. You need to raise rates and drain liquidity before the inflation starts, which is difficult to carry off politically.

Quantitative Easing, Part Two Is the Fed ready to act proactively against inflation? This is the important question. The weakness in the economy will not hold back inflation. This is a very Keynesian concept, and an incorrect one. You need only look at Argentina and Brazil in the 1980’s, where inflation was not linked to the strength of the economy. It was related to money, the absolute amount of money in the economy. These countries were creating money through the payrolls of government employees. The risk we face today in the U.S. economy is that the Federal Reserve Bank governors may not understand the difference between QE1 and QE2. There seem to be a number of them who appear to be Keynesian. In their speeches they aren’t being tough on inflation at all, saying that inflation can’t take off because the economy is still weak. But this is a myth. Historically, there is little evidence that inflation and output are related. Increased money supply (relative to demand) actually has a much bigger impact on speculative asset bubbles, such as the one that we are currently seeing right now in commodities. In 2005 and 2006, the relative increase in supply vs, demand for money didn’t show up in traditional inflation, but in asset bubbles: housing, commodities, and oil. This leads to boom/bust cycles.

Government Spending: Both Parties to Blame Bush Presidency Source: May 2010 CBO Deputy Director Robert Sunshine's presentation to the Fiscal Commission Congressional Budget Office

Government Debt Comparisons General Gross Government Debt (% of GDP) 22

Federal Debt$14.3 Trillion U.S. Federal debt is now at $9.7 Trillion. This is what the U.S. Treasury owes the public from their sales of short term bills, medium term notes, and long term bonds. This number includes all debt owed to U.S. and international investors, money market funds, central banks of other countries, and private banks. This figure does not include $4.6 trillion in IOU’s that the federal government has promised to its own programs like Social Security and federal employee pensions. The federal debt limit that we read about in the press, that is currently being debated in the Congress, is the total of the two, or $14.3 trillion. 23

Military Retirement/Disability Benefits:$3.6 Trillion This is the size of the pension, medical care, and disability benefits for former members of the U.S. armed forces. Federal Employee Retirement Benefits: $2 Trillion This is funded with taxes or borrowing. The federal government employs around two million people. State and Local Government Obligations:$5.2 Trillion Only half of this debt is explicit. The rest is hidden in the form of pension shortfalls and promises made to medical costs for retired workers. 24

Now, Include Unfunded Government Obligations Official vs. Unofficial Debt Ratios 25

EntitlementsSocial Security: $21.4 Trillion Unfunded Liability A record 18.3% of the nation's total personal income was a payment from the government for Social Security, Medicare, food stamps, unemployment benefits and other programs in 2010. Wages accounted for the lowest share of income — 51.0% — since the government began keeping track in 1929. According to projections by the U.S. Congress, the Social Security fund will run deficits every year until its resources are completely drained in 2037. At that point, Social Security would collect enough in payroll taxes to finance 78% of the benefits. More than 54 million people receive retirement, disability, or survivor benefits from Social Security today, and the average monthly check they receive is $1,076. In 2011, Social Security will run a $45 billion deficit and continue to run deficits which will total $547 billion over the next ten years. The Social Security Act was created by Roosevelt in 1935 when average life expectancy in the U.S. was 61.7 years. Now, life expectancy is 78 years. (Source: National Center for Health Statistics, National Vital Statistics Reports, vol. 54, no. 19, June 28, 2006.). While the retirement age has now been raised from 65 to 67 in the U.S., the problem is both demographic and due to increased longevity. JagadeeshGokhale, CATO Institute, Consultant to the U.S. Treasury “The United States would need to save and invest an amount equal to 8.2% of its GDP beginning now and continuing every year forever to pay expected future benefit without future tax increases. This could be accomplished by more than doubling the current 15.3 percent payroll tax on employers and employees, immediately and forever. Alternatively, the federal government could imme- diately stop spending nearly four out of every five dollars on programs other than Social Security and Medicare — eliminating most discretionary spending on such programs as education, national defense, environmental protection and welfare — forever. Each year that the United States does not take action to reduce the projected shortfall, it grows by more than $1.5 trillion, after adjusting for inflation .”

EntitlementsMedicare: $24.8 Trillion Unfunded Liablity • Medicare is a social insurance program administered by the government that provides health insurance coverage to people 65 or over, OR to those under 65 who are permanently physically disabled. • The first of 77 million Baby Boomers turn 65 this year and qualify for Medicare. Enrollment will grow from 48 million in 2010 to 64 million in 2020 and 81 million in 2030, according to Medicare actuaries. That 33 million increase in the next 20 years compares with 13 million in the last 20. • The present value of future Medicare obligations is now $24.8 trillion, or $212,500 per family, beyond what Medicare taxes will bring in. • The alarming increase in the value of this obligation is due to • 1) demographics • 2) The prescription drug benefit passed in 2006 • 3) Rising health costs • The $25 trillion estimate is probably understated because it relies on cost saving changes in the Health Care Reform Law which are unrealistic, like cutting payments to doctors by 30% by 2012. • Spending on Medicare will increase from $523 billion last year to $676 billion in 2011 and is projected at $861 billion next year. • The U.S. Congress is debating solutions. Republicans have proposed giving senior citizens a fixed amount to subsidize the purchase of private health insurance. Democrats propose better management and bringing down the cost of healthcare to match what other countries spend. Either way, Americans can expect less healthcare, higher taxes, or both.

InflationGold: What Is It Telling Us?QE1 and QE2 Contributing to a Loss of Confidence in the Dollar

Chinese Buying of Gold: Preparing the Yuan for Convertibility? In Dec. 2009, the head of the Chinese state owned Assets Supervision Commission said “we recommend China increase its gold reserves to 6,000 metric tons within three-to-five years and possibly to 10,000 tons in eight to 10 years.” Considering that China now has reserves of 1,054 tons, this would imply buying about two and a half to 4.5 years of annual gold production. Some speculate that China is trying to replace its $2 trillion + dollars with gold, but there is reason to believe that it is preparing to launch the Yuan as a convertible currency and would like to back its credibility with gold. The Chinese government is encouraging openly its citizens to put at least 5% of their savings into precious metals.

US Dollar Decline… The Federal Reserve’s Trade Weighted Index measures the US dollar’s performance against seven currencies, and hit record lows last month.

Combined with Soaring Raw Materials Demand, Leading To Commodity Inflation • China has become the largest consumer of Copper, Aluminum, Nickel, Coal, Steel, and Iron Ore. Copper Iron Ore • China needs copper for rural electrification, and foresees an increase in demand by • 1 million tons over the next 2.5 years. Yet Chile, the world’s largest copper • producer, can only increase demand by 56,000 tons per year. (Source: Standard Charter Bank) • Bob Friedland, Chairman of Ivanhoe Mining: “We need more copper in the next • twenty years than was mined in the last 110 years…Those of us in the business • don’t have any idea where this metal is going to come from”.

Agricultural Commodity Inflation Corn Wheat Soybean Cotton

Agricultural Commodity Inflation Also caused by: • Climate Change: Droughts, floods, and fires (China, Russia, France, Australia, Canada, U.S.) • Demand from China and India • Ethanol Production (The U.S. grows 40% of the world’s corn, 30% of which is being used for ethanol production). • High Petroleum Prices (Boosting transportation costs and fertilizer prices). • Political Instability (Disruption of supply chains).

Oil Price Increases Cause a Mechanical Negative Effect on the Dollar • The U.S. is a net importer of oil. (9.44 Million barrels per day) • The higher the oil price is, the higher the transfer of wealth from US to Middle East. • The outbound dollars create a current account deficit. The higher the oil price, the larger the gap in that deficit. • This creates downward pressure on the US Dollar.

Crude Oil Supply: Reserves Harder To Find No Reserve Growth In Middle East Source: Bloomberg, BP Statistical Review

Emerging Markets: Strong Energy Demand Burgeoning BIC Electricity Demand Source: Bloomberg

World Demand: Projected To Grow at 1.5% p.a. ChIndiaA Key Driver In World Energy Demand Source: US Energy Information Administration

Inflation This chart reflects an estimate of inflation today as if it were calculated the same way it was in 1980.

Inflation and Civil Unrest Food prices have been identified as one trigger for North African uprisings. In this and recent years (2008), food riots have impacted: Argentina Morocco Mozambique Jordan Tunisia Yemen Senegal Peru Egypt Sudan Bangladesh Bolivia India Pakistan Morocco Haiti Indonesia China Peru Cameroon Chad Somalia Ethiopia Mexico Guinea Mauritania Senegal Uzbekistan

U.S. Defense Spending Defense is not the Problem • The U.S. spends relatively little on defense today. The 2011 budget of $530 billion represents only 3.5% of GDP. Adding in the cost of Iraq and Afghanistan it amounts to 4.5% During the Cold War, the U.S. spent around 7.5% of its GDP on defense. • Through 2016, the Pentagon will see no growth in spending and will cut 47,000 troops from the Army and the Marine Corps. • Robert Gates, retiring as Secretary of Defense this month, projected that 2-3% “real” budget growth was needed to sustain what the DoD was doing now, but that it could “make do” with only 1% growth. The White House gave him 0% • “If you cut the defense budget by 10%, which would be catastrophic in terms of force structure, that’s $55 billion out of a $1.4 trillion deficit…..”We are not the problem”. • “The reality is that the entitlement state is crowding out national defense” Source: Wall Street Journal

U.S. Defense Spending“America Can Be A Superpower or a Welfare State, But Not Both” –Robert Gates • The three largest entitlements, Social Security, Medicare, and Medicaid accounted for 9.8% of GDP last year, and will rise to 10.8% by 2020, while defense spending goes down to 2.7% by 2020. • Historians often refer to imperial Roman “overstretch” and conclude that the same forces brought down the British Empire, and that the same may be happening to the U.S. right now. Rather than “imperial” overstretch, some military analysts are now discussing “entitlement” overstretch. • The first great inflation occurred in third century AD Rome. Up until that time, the Roman army served as the engine of growth for the Empire. With each new conquest of land, they were able to increase the tax base for Rome. When the territorial limits of the Roman empire were reached the army’s primary mission focused on protecting the empire’s borders from barbarians invaders. • After, military pay rose sharply as civil unrest and political instability increased in successive waves. Sustaining the payroll of public sector employees grew increasingly difficult. • Today, it is not the military ,but the entire baby boom generation which served as the postwar engine of growth but has now become an unsustainable financial burden. The Romans debased their currency to meet their financial obligations. In 180 A.D., the silver content of a Denarius was 75%. By 270 A.D., it was 0.02% Imperial Rome never regained its greatness.