Download

1 / 34

340 likes | 496 Views

Health Care Reform: When the Rubber Hits the Road FERMA Conference July 16, 2014. What the ACA Is Supposed To Do . 3. Policy Objectives of the ACA. Cover the uninsured . Bend the cost curve downward . Not increase the Federal deficit. ACA Compliance

E N D

Health Care Reform: When the Rubber Hits the Road FERMA Conference July 16, 2014

What the ACA Is Supposed To Do 3 Policy Objectives of the ACA Cover the uninsured Bend the cost curve downward Not increase the Federal deficit

ACA Compliance Your Top TenList for 2014 and Beyond

1 Employer Mandate and Penalties Begin in 2015 Or Doomsday Penalty Bull’s Eye Penalty • Employer does not offer Minimum Essential Coverage (“MEC”) to at least 95% of all FTEs and their eligible dependents, and • At least one FTE enrolls in Exchange and receives Federal subsidy • $2,000 per year for each FTE (minus first 30 FTEs) within controlled group entity • Employer offers MEC to FTEs but coverage is either • “Unaffordable” or • Not “minimum actuarial value” • $3,000 per year per each FTE who enrolls in an Exchange and receives a Federal subsidy

What Keeps Employers Up At Night Measurement period Period of time over which employer tracks variable hour and seasonal employee’s hours of service Cannot be less than three months or more than twelve months in duration Seasonal employee is one whose employment runs six months or less Initial measurement period for new employees will be based on each employee’s start date Standard measurement period for ongoing employees will be uniform period of time set by employer Administrative period—optional (up to 90 days in duration) Employer looks back at employee’s hours of service in measurement period May be utilized for conducting calculation and open enrollment Stability period Period of time employer must offer coverage to FTE to avoid ACA penalties Stability period can be between six months and one year but not less than Measurement Period If employee is considered full-time in measurement period but falls to part-time in stability period, benefits must be offered through the end of the stability period • Special note for schools: Summer recess may not be used as part of measurement period 5

Employer Mandate – Recent Update Updated rules were issued by the Department of the Treasury on February 10th providing more flexibility for employers to meet the employer mandate. Among the changes are: • Shared Responsibility requirements do not take effect for employers between 50 – 99 full-time equivalent employees until their plan renewal date in 2016. For employers with 100+ full-time equivalent employees, it will take effect on their plan renewal date in 2015; • Option to include a six month transition measurement period in 2014 in preparation for a 12 month stability period in 2015; • Previously, there was a 95% rule that an employer could abide by in order to avoid the $2,000 “failure to offer” shared responsibility penalty (i.e. if an employer offered coverageto at least 95% of their full-time employees, they would only be subject to the $3,000 per impacted employee penalty if coverage for any employee is unaffordable or not of minimum value). The new rules allow a 70% threshold in 2015 before the 95% rule goes into effect in 2016; • The policy that employers offer coverage to their full-time employees’ dependents to age 26 will not apply in 2015 to those employers that are taking steps to arrange for such coverage in 2016. Also, coverage for foster children or step-children does not need to be offered. • There was a further transition made on the “nuclear” penalty.” For 2015, there would be a waiver of 80 full-time lives which will then be lowered to 30 full-time lives in 2016.

2 THE EMPLOYER MANDATE AND ELIGIBILITY for Exchange Subsidies Individual is not eligible for subsidized coverage if offered affordable health care coverage of minimum value from an employer • Employer must offer dependent coverage (not spousal coverage) to employee to avoid penalty, but coverage does not have to be “affordable” • Individual enrolled in employer-sponsored MEC not eligible for a subsidy • Regardless of whether coverage is affordable or minimum value What happens if an employed individual is offered “affordable” employee-only coverage, but family coverage is “unaffordable”? • Employee and family will not be eligible for subsidy in the exchange

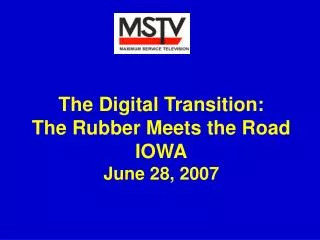

Half of States Are Expanding Medicaid in 2014 ME AK NH WA VT ND MO MN MA OR WI ID NY SD WY MI PA RI IA NE NJ OH NV HI IN UT IL WV CO VA CT KS MO KY CA NC TN DE OK AZ SC AR NM GA AL MS MD LA TX 14 States Will Expand Medicaid Democrat Governor FL 6 States Leaning toward expanding Medicaid Republican Governor 8 States Won’t Expand Medicaid 6 States Leaning toward Not Expanding Medicaid 16 States Undecided on Medicaid Expansion

Substitutes and Part-Time Workers Educational institutions face unique challenges as it relates to the employer mandates, due to scheduling issues and to the large number of variable workers that are an integral part of the workforce. The variable workers fall largely into two categories: • Substitute teachers • Part-time workers with two jobs (i.e. maintenance workers and security) In order to manage the potential additional liability of including these employees in the medical program, schools are implementing various strategies. These include the following: • Implement a time management system that ensures no variable employee exceeds 30 hours a week on average • Establish a “monthly” measurement period • Create a limited bank of variable workers that will receive benefits • Utilize a staffing company • Limit part-timers to one job

Retirees Florida law requires that retiree rates cannot exceed active rates. The significant issue associated with Retirees is OPEB liability. As such, retirees present their own unique issues, pre-65 vs. Post-65: • Pre-65 Retirees • This segment of the population is the most costly due to ineligibility for Medicare and subject to Disease Management Conditions; • They are eligible for public exchange subsidies • Strategy: Offer fund to cover cost net of subsidy • Post-65 Retirees • Generally cost less than actives and pre-65 retirees; • Similar to Medicaid, Medicare eligible retirees are not eligible for public exchange subsidies; • Strategy: Initiate a Senior Exchange

3 Proposed Regulations on Reporting Rules Code Section 6055 requires reporting to IRS by plan sponsors and health insurers about health care coverage offered to individuals and requires statements to individuals • When to File with IRS? February 28, 2016 for 2015 coverage year • When to Provide to Individuals? January 31 following calendar year of coverage Code Section 6056 requires employers to file a return with the IRS about health care coverage provided to FTEs and provide a written statement to FTEs • When to File with IRS? For 2015, March 1, 2016 or March 31, 2016 (if filed electronically) • When to Provide to FTEs?January 31 following coverage year

Final Regulations on Employer Reporting • A single consolidated form has been created for both sections 6055 and 6056. The combined form will have two sections: the top half for Section 6055 and the bottom half for Section 6056. • Employers with fewer than 50 full-time employees are exempt; • Employers that are self-funded and are large enough to be subject to the shared responsibility penalties will be required to fill out both sections; • Employers that are not self-funded but are large enough to be subject to the shared responsibility penalties need only fill out the top portion of the form • Information required: • Section 6056 • Information about the entity providing coverage including contact information • Which individuals are enrolled, with identifying information and the months they were covered • Section 6066 • Information about the employer offering coverage, including contact information and # of full-time employees • For each full-time employee, information about the coverage (if any) offered to the employee, by month, including the lowest employee cost of self-only coverage offered • The new rules omit length of waiting period, employer share of the total allowed costs of benefits, and the amount of advance payments of the premium tax credit and cost-sharing reductions

Final Regulations on Employer Reporting (cont’d) • Due date is by January 31st based on the prior year’s data. The first report is due January 31, 2016. • The report can be submitted to the employees with their W-2. However, in order to be sent electronically, there must be written employee consent. • The penalty is $100 per report not delivered. • There are four different options for reporting of data: • General Reporting Method; • Qualifying Offer Method; • 98% Offer Method; • Optional Method (available only for 2015)

Additional Reporting Requirement: HPID • Recently, new standards and operating rules forhow electronic transactions are conducted among HIPAA covered entities like health plans, clearinghouses, and health care providers. • For self-funded clients, the due date for application of a Health Plan Identifier is November 15th. If they have at least $5 million in annual receipts, then their due date is in 2015. If they have less, then it is in 2016. • CMS distributed a presentation which shows a step by step process for the application of an HPID. Aon is not in a position to apply for the HPID on behalf of their clients. However, we can assist with any questions they may have.

4 Transitional Reinsurance Fee Designed to Stabilize Exchanges Reinsurance fund stabilizes insurers in exchanges during their first three years in the event of losses due to adverse selection • 2014 per capita payment ($63) due in two installments • 2015 per capita payment ($44) due in two installments Fees are due in installments Fees are required only for “major medical coverage”

Transitional Reinsurance Fee Calculation Options • Purpose of the Transitional Reinsurance Fee is to cover the cost of the high risk pools in the public marketplaces. The fee for 2014 is $63 per member per year; 2015 will be $44 pmpy • By November 15th, self-funded plans must report to HHS the number of members. • There are three different options for calculating the number of members that can have financial implications: • Actual Count or Snapshot Count – Take the average number of members that are on the plan for the first nine months of a plan year • Ex. Client averaged 2,016 members per month based on 854 employees) = $63 x 2016 = $127,008 • Snapshot Factor - Take the number of employees in all non-single tiers, multiply by 2.35 and then add the number of enrolled single employees one time for each of first three quarters • Ex. Jan 2013: 296 ee only + ((131 ee + sp) + (132 ee + ch) + (282 ee + fam)) x 2.35 = 1,576 Apr 2013: 304 ee only + ((135 ee + sp) + (133 ee + ch) + (280 ee + fam)) x 2.35 = 1,592 July 2013: 302 ee only + ((133 ee + sp) + (135 ee + ch) + (275 ee + fam)) x 2.35 = 1,578 (1,576 + 1,592 + 1,578)/3 = 1,582 x $63 = $99,666 • Form 5500 Method – Add the number of total participants at the beginning and end of the year • Ex. Jan 2013: 845 enrolled Dec 2013: 854 enrolled 845 + 854 = 1,699 x $63 = $107,037

Transitional Reinsurance Fee Payment • In May, HHS released the following link to an FAQ that addresses how self-funded employers will need to process the Transitional Reinsurance Fee: • http://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/Downloads/Reinsurance-contributions-process-FAQ-5-22-14.pdf • The process begins with registration through the website Pay.gov. • On June 30th, CMS conducted a webinar on the process for registering through Pay.gov. • The calendar is as follows: • November 15, 2014 Submit Annual Enrollment Count • Not later than January 15, 2015 Remit First Contribution of $52.50 per Covered Member • Fourth Quarter 2015 Remit Second Contribution of $10.50 per Covered Member

5 Cost-sharing Limits Start in 2014 • Health plans must limit annual cost-sharing to same cost-sharing limits as HDHP/HSA plans in 2014 • $6,350 (individual) and $12,700 (family) • OOP limits apply only to payments for essential health benefits (“EHBs”) • Payments for non-network providers and non-covered services do not count • Transition rule for 2014 for multiple service providers • For 2015, medical and Rx • carve-out may use separate OOP limits, as long as combined OOP limit applicable to all EHBs does not exceed maximum OOP limit

Impact of Copayment/Deductible Change • Application of copayments applies to all copayments, not just office visit and pharmacy. They apply all copayments, including inpatient, outpatient surgical, high end radiology. • Carriers may have 3rd party PBM that is not completely visible. The option to postpone pharmacy copayments until 2015 should be addressed carrier by carrier. • Projected impact: • Adding non-Rx copayments and deductibles: 1 – 3% • Adding Rx copayments: 1 – 2% • In order to attain claim neutrality, consideration should be given to increasing the out-of-pocket maximum, with potential range of $500 - $1,000. Plans that are very lean (i.e. high copayments) could have larger impacts.

6 What Is—And Isn’t—Minimum Essential Coverage? • Minimum Essential Coveragedoes not include “excepted benefits” • FSA is an excepted benefit only if employee has other health care coverage available • FSA cannot exceed greater of (1) 2 x salary reduction amount or (2) $500 plus salary reduction amount • Must be offered through a Section 125 cafeteria plan • Limited scope dental and vision benefits • Disability coverage, AD&D coverage, liability insurance, Workers’ Comp • EAPs that do not provide significant benefits in the nature of medical care or treatment Excepted benefits don’t have to comply with ACA group market rules but won’t satisfy mandates

Minimum Essential Coverage Under Health Care Reform, numerous limited medical plans, such as Starbridge, have been sunset because of their inability to meet regulatory requirements. To adapt, vendors have been developing new products in order to meet new needs. To assist both individuals and employers meet the Health Care Reform mandates, new products are being marketed that blend a MEC plan with a Limited Medical Benefit plan option. • Under the current Health Care Reform guidelines, preventive care covered under a self-funded arrangement would meet the MEC requirement for both the individual mandate and the “nuclear” mandate for employers. Some of the preventive care that is being covered would include: • Immunizations • Screenings • Preventive Colonoscopies for individuals 50+ years of age • Preventive Mammograms for women 40+ years of age • Some of the vendors that have been putting forth such products include: • Ternian • Pan American • Transamerica • United Healthcare • Aetna • Century Healthcare

Minimum Essential Coverage • As a means by which to further provide protection against the “targeted” employer mandate, vendors are also attaching a Limited Medical Plan that provides scheduled coverage for a variety of procedures on a per dollar per incident basis with no dollar maximums. In addition, they may also include: • Prescription drug discount cards; • Employee Assistance Program (EAP); • Network discounts; • Telemedicine; • Group term life insurance • Short Term Disability • Depending on the vendor and the level of coverage quoted, the single rate can range from $80 - $110 for single coverage. • General enrollment requirements are 51+ lives and there may be some geographic issues of availability due to state filing issues (specifically in the upper Northeast). Employer contribution requirements will vary based on the total number of eligible employees. • If an employer were to offer such a product while covering 100% of the premium, it is unlikely that an employee would seek coverage in a public exchange, thus limiting the potential exposure to the targeted penalty for an employer.

7 HRAs and the ACA HRAs must be integrated with another ACA-compliant group health plan in order to comply with ACA group market reforms • Stand-alone HRAs and employer payment plans violate ACA rules prohibiting annual dollar limits and requiring 100% preventive care coverage • Stand-alone retiree-only HRAs are not subject to the ACA group market reforms Previous guidance outlined minimum value and non-minimum value options for an HRA to be considered “integrated” • HRA can only be available to employees enrolled in other group health plan coverage • Employer does not have to sponsor the other coverage • Participant must be able to permanently opt out and waive HRA coverage • Participant must have the option of permanently forfeiting the HRA upon termination of employment

HDHP and PPACA Health Care Reform is impacted in several areas by HDHPs: The new limits for non-HSA plans effective January 1, 2015 will be $6,600 for single and $13,200 for family. HSA limits will be $6,450 and $12,900. Although Health Care Reform covers dependents until age 26, the tax code only allows an employer to allow for reimbursements through an HSA for dependents to age 24. Employers are not allowed to deposit funds into an HRA that is not tied to a plan that meets Market Reforms, such as removal of annual maximums and coverage of preventive care. The penalty would be $100 per day per employee ($36,000 annually).

8 Implementing U.S. v. Windsor After Windsor, IRS confirmed that a same-sex spouse is a spouse for federal tax purposes, even if the married couple is domiciled in a state that does not recognize the validity of same-sex marriages A participant who is lawfully married to a same-sex spouse • Can add spouse to the plan mid-year under the cafeteria plan mid-year change in status rules • Can pay for health care coverage on a pre-tax basis under a cafeteria plan • Can reimburse spousal medical expenses from an FSA • Is subject to HSA and DCSA limits for a married couple

Taxation of Health Care Coverage FSA and HSA funds can now be used to reimburse employees for same-sex spouse’s medical expenses As long as state law recognizes the spousal relationship Does not apply to medical expenses for same-sex or opposite-sex domestic partners who do not qualify as dependents Employee can pay for cost of health care coverage for same-sex spouse on a pre-tax basis through a 125 plan Employers should not impute income or require payment with after-tax contributions IRS needs to address retroactivity of decision and application to spouses who move from recognition state to non-recognition state Same-sex marriage and same-sex divorce constitute change in status under cafeteria plan rules Allows employees to change cafeteria plan elections on a pre-tax basis California, Connecticut, Delaware, Hawaii, Illinois, Iowa, Kentucky, Maine, Maryland, Massachusetts, Minnesota, New Hampshire, New Jersey, New Mexico, Ohio, Pennsylvania, Rhode Island, Utah, Vermont, Virginia, and Washington now allow same-sex marriages. Additional court cases are pending in many other states, including Florida. Consulting | U.S. Health & BenefitsProprietary & Confidential | Health Care Plans after DOMA.PPT/002-J8-09749 07/2013

What Employers Need to Do Adjust employee benefit practices to reflect new federal definition of “spouse” Imputed income Health care coverage Taxation issues COBRA HIPAA FMLA Maintain current imputed income practices in states that do not recognize same sex marriage Guidance from government will be needed on transition issues Will application of Federal laws to spouse be retroactive? January 1, 2013? Earlier? Social Security survivor benefits? Income tax filings and refunds? If so, to what date? Consulting | U.S. Health & BenefitsProprietary & Confidential | Health Care Plans after DOMA.PPT/002-J8-09749 07/2013

9 FSA Carryover Option Employers can allow FSA participants to carry over up to $500 of unused FSA funds for use in subsequent plan years • Does not count toward $2,500 health FSA maximum amount • Employers cannot utilize both the grace period rule and the $500 carryover rule • Consider impact on HSAs Employers who want to adopt the $500 carryover rule must amend their plan documents on or before the last day of the plan year from which the amounts may be carried over • For 2013, amendment can be made by last day of plan year that begins in 2014

Considerations to Allow FSA Rollover • Can your FSA Administrator handle the rollover? • Will your FSA Administrator charge for managing the rollover? • What is your turnover rate? • Potential loss of forfeitures • Potential for Increased number of overspent accounts • Potential financial impact from Health FSA rollover • Revenue from the Health FSA for 2012 (we need to use a year that has already ended to perform the calculation) • Total FICA savings from Health FSA contributions in 2013 (7.65% for those below $110,000 and 1.45% for those above $110,000 in total compensation for 2013 + Total forfeitures from 2013 = Total Revenue from Health FSA • Cost of Operating Health FSA for 2013 • Total Health FSA plan administration charges for 2012 + Total amount of overspent accounts in 2012 = Total Cost of Health FSA Total Revenue minus Total Cost is the amount the employer currently • Total revenue minus total cost is the amount the employer currently benefits from having Health FSA

10 Excise Tax on High Cost Employer Health Care Coverage • Effective in 2018, 40% excise tax is imposed on excess employer health care benefits • The excess benefit is coverage over certain indexed thresholds • Self-Only Coverage: $10,200 • $11,850 for “qualified retirees” and high risk professions • Other than Self-Only Coverage: $27,500 • $30,950 for “qualified retirees” and high risk professions • Coverage includes employer contributions and employee pre-tax contributions under cafeteria plans

Employers Need to Comply with ACA andReduce Costs Your Health Care Compliance Strategy What do you have to do? When? What are your options? Your Health Care Strategy What is your long-term plan to reduce your health care costs?