Download

1 / 101

1.02k likes | 1.14k Views

Second-Quarter 2013 Sheep Industry Review Prepared by American Sheep Industry Association for the American Lamb Board July 2013. Contents Executive Summary Feeder and Slaughter Lamb Market Trends Feeder and Slaughter Lamb Price Projections Carcass and Boxed Lamb Market Trends

E N D

Second-Quarter 2013 Sheep Industry Review Prepared by American Sheep Industry Association for the American Lamb Board July 2013

Contents Executive Summary • Feeder and Slaughter Lamb Market Trends • Feeder and Slaughter Lamb Price Projections • Carcass and Boxed Lamb Market Trends • Retail Feature Activity • Price Spreads • Pelts • Replacement Sheep • Domestic Production and Trade • Nontraditional Market • Total Lamb and Mutton Availability • Price Comparison to Imported Product • Exchange Rates

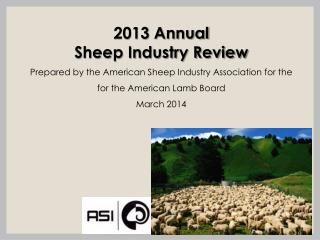

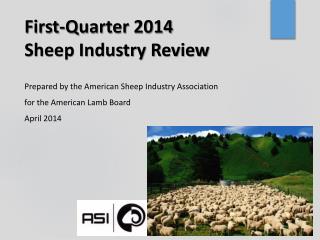

Executive Summary The lamb industry is finding it footing after record-high prices in 2011 followed by a record collapse in 2012. In 2013, the carcass market was flat, the wholesale market continued to lose value—albeit at a slower pace—and the feeder and slaughter lamb markets were down 25% to 42% from a year ago. This year the industry is challenged to keep the slaughter chain moving and maintain quality, while facing a surge of imports at retail. Lamb imports totaled 63.5 million lbs. in January through May – up 17% year-to-year. A combination of forces prompted the influx of lamb imports. Meat and Livestock Australia reported that widespread dry conditions across most sheep growing regions and heavier weights over the past five years prompted high slaughter and production (7/5/13). Sheep and lamb slaughter from January to May was at a three-year high. Coupled with increased Australian production has been the recent strengthening of the U.S. dollar against the Australian dollar. Since January, the Australian dollar lost 12% against the US$ to land at 94 Australian cents per USD. It is anticipated that the Australian dollar will fall even further. In January through May, total lamb availability (imports plus domestic production, subtracting exported lamb) in the U.S. was 124.7 million lbs., up 8% year-on-year. However, cold storage stocks were still high. When cold storage is subtracted from disappearance, a downward trend is 2013 availability is revealed. Uncertainty prevails in estimating volume marketed: We don’t know what percent of cold storage is imported product.

Executive Summary, page 2 In July a light supply of old and new crop lambs continued to move to market out of Colorado feedlots. Tight domestic supplies in the third quarter, coupled with a slowdown in imports will help support both feeder and slaughter lamb prices in coming months. In early July, LMIC forecasted that third-quarter national direct slaughter lambs on a carcass weight could range from $235 to $245 per cwt., up from an estimated $225 per cwt. in the second quarter, but down 5% year-on-year. Sixty- to 90-lb. 3-market feeder lamb prices at auction were forecasted to range between $125 and $135 per cwt., up 29 percent from a year ago and up from an estimated $114 per cwt. in the second quarter. Through July and into early August, the Muslim observance of Ramadan will likely encourage increased retail lamb featuring activity. In early July, the New Holland auction saw an uptick in slaughter lamb prices. Feeder & Slaughter Lamb Markets The 3-market feeder lamb auction price saw a 29-percent quarterly drop to $114.01/cwt., down 42% year-on-year. Markets included San Angelo, Ft. Collins and Sioux Falls.

Executive Summary, page 3 Feeder lambs in direct trade averaged $98.65 per cwt. in the second quarter, down 10% quarterly and down 32% year-to-year. Live, slaughter lamb prices at auction lost 6% quarterly to $109.20/cwt. and lost 27% from $141/cwt. a year ago. Slaughter lamb prices on a carcass-based formula averaged $224.87/cwt. ($112.21/cwt. live-converted) in the second quarter, down 0.5% quarterly and down 25% year-on-year. Feedstuffs remained high into the second quarter with minimal relief. Corn averaged $6.99 per bu., down 1% quarterly and up 10% year-on-year. High cost of gain meant weights going into feedlots were lower in 2013 over 2012. Weighted average carcass prices were $249.67/cwt. in the second quarter, 0.5% lower quarterly and down 24% from a year ago. The gross carcass value averaged $284.88/cwt. in the second quarter, down 2% quarterly and down 20% year-to-year. Federally-inspected slaughter lamb weights averaged 142 lbs. in the second quarter, down 7% year-on-year. Yield Grade 4 & 5 in lbs. was 24% of total slaughter in the first-half 2013 compared to 30% in 2012.

The 3-market feeder lamb auction price saw a 29-percent quarterly drop to $114.01/cwt., down 42% year-on-year. • Markets included San Angelo, Ft. Collins and Sioux Falls. • Prices averaged $120.34/cwt. in April, $116/cwt. in May and $105.70/cwt. in June. Auction Feeder Lamb (60- to 90-lb.) Prices Down 42% in a Year

Feeder lambs averaged $98.65 per cwt. in Q2, down 10% quarterly, and down 32% year-to-year. • Feeders averaged $97.92/cwt. in April, $100.71/cwt. in May and $97.31/cwt. in June. Feeder Lambs in Direct Trade Fell Quarterly

Feeders in Direct Trade Down 57% in Value from Record High

Q2 Volume of Direct Feeder Lambs Down 10% Quarterly to 55,350 Head;Down 32% Year-to-Year

Feed Costs Still High Historically • Corn averaged $6.99 per bu. in Q2, down 1% quarterly and up 10% year-on-year. • Corn averaged $6.97 per bu. in April, $6.97 per bu. in May and $7.02 per bu. in June.

Alfalfa averaged $217.33per ton in the quarter ending April (season’s end), up 0.5% quarterly and 8% higher year-to-year. • Alfalfa was $218 per ton in April, $219 per ton in May and $215 per ton in June.

Live, slaughter lamb prices at auction lost 6% quarterly to $102.53/cwt. and lost 27% from $141/cwt. a year ago. • Prices averaged $98.59/cwt. in April, $101.88/cwt. in May and $107.13/cwt. in June. Auction Slaughter Lamb Prices Weakened Quarterly

At 155,100 head, formula trades were down 3% quarterly and up 14% year-on-year. • Slaughter lamb prices on a carcass-based formula averaged $224.87/cwt. ($112.21/cwt. live-converted) in Q2, down 0.5% quarterly and down 25% year-on-year. • Weighted-average prices were $227/cwt. in April, $222.76/cwt. in May and $224.85/cwt. in June. Carcass-Based Formula Slaughter Lamb Prices Up Quarterly & Down Year-to-Year

Second-Quarter Slaughter Lamb Prices on Formula Hit a 4-Year Low

Auction Slaughter Lamb Still Lower than Slaughter Lamb Prices on Formula

The “market” is selecting for value and cost minimization: Reduced $ for heavies. -- Heavier lambs often have higher fabrication costs.

LMIC early July forecast: • National direct slaughter lambs on a carcass weight: $235 to $245 per cwt., up from $225 per cwt. quarterly, but down 5% year-on-year. • Sixty- to 90-lb. 3-market (CO, SD, TX) feeder lamb prices at auction: $125 and $135 per cwt., up 29% from a year ago and up from an estimated $114 per cwt. in Q2. • These volatile times means any price forecast should be used with caution. Feeder & Slaughter Lamb Q3 Forecasts

Price trends--up or down--depend on which factor dominates, supply or demand. • During the summer, slaughter lamb supplies tighten, supporting prices. The third quarter is typically the highest-priced quarter. • When feeders come to market in the fall and supplies increase, prices tend to weaken. • The index shows the average relationship of prices in each month to the average for the year. An index of 105 means prices are 5% above the annual price average. Seasonal Index Lends Predictive Insight

Slaughter lambs on formula are expected to gain one-half percent in Q3 quarterly. LMIC forecasted tight supplies and lower imports could provide even stronger Q3 price support.

In Q3, feeder lambs at auction could weaken by 8% from the second quarter by historical trend.LMIC forecast differed: prices expected to gain in Q3

Q3 commercial slaughter numbers could slow 6% quarterly, 3% below a year ago. • Estimated commercial lamb supplies on feed in Colorado were the lowest going into Q3 in 5 years. • This forecasted quarterly slaughter drop is the largest in over 5 years. • At the LMIC-forecasted Q3 dressed weight of 66 lbs., lower slaughter weights will translate into much lower production. • Production is estimated to fall 10% quarterly and 9% year-on-year. LMIC Forecasted Sharp Q3 Production Contraction

Lamb Demand Forecast?Tighter Q3 Supplies, Strong Beef Prices (Although a bit softer),Stronger Income Growth, andQuality Consistency….Could Support Lamb Demand**Demand growth is key to stronger prices.

Slowly, but Surely Real Incomes Making a Sustained Come Back Source: U.S. Dept. of Commerce

Weaker Beef Prices Could Hurt Lamb Demand All fresh retail beef was $487.97 per cwt. in Q2, down 1% quarterly, up 5% year-on-year.

Likely significant yield growth over last year and modest acreage expansion drive corn price forecasts lower. • The LMIC forecast is currently at $4.60 per bushel, down 33% from 2012-13. • The farm price for corn in 2012/13 is estimated at $6.75 to $7.15. The projected price range for 2013/14 is $4.40 to $5.20 per bushel (USDA, 7/15/13). • Improved pasture & range conditions and lower-priced competing feed could mean softer hay prices this year (LMIC, 6/2013). Relief in Sight for High Lamb Feed Costs

Recall the breakeven analysis is only one snapshot of feedlot marketing. • In April/early May, over 22,000 head traded out of CA at $96.50/cwt. and 106 lbs. • July estimated break-even was $114 to $121 per cwt. compared to $114 per cwt., the live-converted formula carcass-based price. Lower Feeders, Stable Feed Helped Improve Margins

Sensitivity Break-Even Analysis A: July kill of April/May California lambs with a $1.30 per lb. cost of gain.

Sensitivity Break-Even Analysis B: July kill of April/May California lambs with a $1.50 per lb. cost of gain.

Weighted average carcass price averaged $249.67/cwt. in Q2, 0.5% lower quarterly and down 24% from a year ago. Carcass price was $247.99/cwt. in April, $249.73/cwt. in May and $251.29/cwt. in June. Carcass Prices Down 35% from Record High

Yield Grade determination is positively correlated with heavier slaughter lambs and increased deposits of back fat. • Yield Grade 4 & 5 in lbs. was 24% of total slaughter in the first-half 2013 compared to 30% in 2012. Carcasses Trimmer: YG 4s and 5s Coming Down

Yield Grades for Federally Inspected Lamb and MuttonPercentages, Fiscal YearSource: USDA, AMS, Livestock and Seed Division.

The gross carcass value averaged $284.88/cwt. in Q2, down 2% quarterly and down 20% year-to-year. • Gross carcass value was $288.76/cwt. in April, $283.13/cwt. in May and $282.76/cwt. in June. Q1 Gross Carcass Value (Wholesale Average) Weakened Quarterly and Year-to-Year

The rack averaged $509.30/cwt. in Q2, down 0.25% quarterly and down 25% year-on-year. • The rack was $510.25/cwt. in April, $501.97/cwt. in May and $515.68/cwt. in June. Wholesale Rack Gained in Late Q2

Loins, trimmed 4x4, averaged $452.11/cwt., down 1% quarterly and down 13% year-to-year. • Loins were $450.22/cwt. in April, $450.50/cwt. in May and $455.60/cwt. in June. Q2 Loins Down Quarterly

The leg averaged $314.89/cwt. in Q2, down 2% quarterly and down 24% year-to-year. • The leg was $322.38/cwt. in April, $312.48/cwt. in May and $309.81/cwt. in June. Leg, Trotter-Off, Down Quarterly & Down Year-to-Year

The shoulder averaged $231.05/cwt. in Q2, down 4% quarterly and down 8% year-on-year. • The shoulder was $236.44/cwt. in April, $232.01/cwt. in May and $224.71/cwt. in June. Shoulder Lost Greatest % Among Primals in Q2

Ground lamb averaged $531.81/cwt. in Q2, down 2% quarterly and down 10% year-on-year. • Ground lamb was $528.17/cwt. in April, $531.89/cwt. in May and $535.38/cwt. in June. Ground Lamb Gained in Q1, Lost in Q2