Download

1 / 41

420 likes | 446 Views

Reflecting on a 20+ year journey, exploring consumption models, CAPMs, international finance, and empirical methods in asset pricing. Insights on what works and what doesn't in the field.

E N D

Empirical Asset Pricing: Impressions and Lessons from a 20+ Year Journey For the 2005 FMA Doctoral Program By: Wayne Ferson October, 2005

Overview • Some things I have learned (in 20+ years as an empirical asset pricer) • Some things I still wonder about (after 20+ years as an empirical asset pricer). 3. My “Top Ten.”

About Consumption Models: JFQA 83 – thesis JFE 87 – Merrick JFE 91 – Constantinides JF 92 - Harvey EER 93 – Braun, Constantinides Things I have Learned

About Consumption Models: JFQA 83 – thesis JFE 87 – Merrick JFE 91 – Constantinides JF 92 - Harvey EER 93 – Braun, Constantinides They Don’t Work (they don’t even calibrate). Things I have Learned

About Consumption Models: JFQA 83 – thesis JFE 87 – Merrick JFE 91 – Constantinides JF 92 - Harvey EER 93 – Braun, Constantinides They Don’t Work (they don’t even calibrate). They have great economic intuition. Things I have Learned

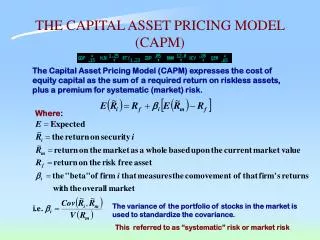

About Conditional /Multifactor CAPMs: JFE 85 – Gibbons JF 87 – Kandel and Stambaugh JF 89,90 JPE 91 – Harvey JF 93 – Foerster and Keim JF 99 - Harvey Mansci 98 – Locke WP 05 - Siegel Things I have Learned

About Conditional /Multifactor CAPMs: JFE 85 – Gibbons JF 87 – Kandel and Stambaugh JF 89,90 JPE 91 – Harvey JF 93 – Foerster and Keim JF 99 - Harvey Mansci 98 – Locke WP 05 - Siegel They Don’t Work Very Well. Things I have Learned

About Conditional /Multifactor CAPMs: JFE 85 – Gibbons JF 87 – Kandel and Stambaugh JF 89,90 JPE 91 – Harvey JF 93 – Foerster and Keim JF 99 - Harvey Mansci 98 – Locke WP 05 - Siegel They Don’t Work Very Well. They are algebraically Beautiful! Things I have Learned

About Conditional /Multifactor CAPMs: JFE 85 – Gibbons JF 87 – Kandel and Stambaugh JF 89,90 JPE 91 – Harvey JF 93 – Foerster and Keim JF 99 - Harvey Mansci 98 – Locke WP 05 - Siegel They Don’t Work Very Well. They are algebraically Beautiful! Practitioners Really want them! Things I have Learned

About INTERNATIONAL Conditional /Multifactor CAPMs: RFS 93 – Harvey JBF 94 – Harvey JBF 97 - Harvey SEPR 98 - Harvey Things I have Learned

About INTERNATIONAL Conditional /Multifactor CAPMs: RFS 93 – Harvey JBF 94 – Harvey JBF 97 - Harvey SEPR 98 - Harvey They Don’t Work Very Well, either. (See Above) Things I have Learned

Conditional Performance Evaluation and Mutual Funds: JF 96 - Schadt FAJ 96 – Warther RFS 98 – Christopherson and Glassman JPM 99 – Christopherson and Turner JFE 99 – Becker, Myers and Schill JB 02 – Farnsworth, Jackson and Todd JFE 02 – Khang RFS 06 – Kisgen and Henry WP 05 – Chen and Peters WP 05 - Qian Things I have Learned

Conditional Performance Evaluation and Mutual Funds: JF 96 - Schadt FAJ 96 – Warther RFS 98 – Christopherson and Glassman JPM 99 – Christopherson and Turner JFE 99 – Becker, Myers and Schill JB 02 – Farnsworth, Jackson and Todd JFE 02 – Khang RFS 06 – Kisgen and Henry WP 05 – Chen and Peters WP 05 - Qian Conditioning Seems to Work! Things I have Learned

Conditional Performance Evaluation and Mutual Funds: JF 96 - Schadt FAJ 96 – Warther RFS 98 – Christopherson and Glassman JPM 99 – Christopherson and Turner JFE 99 – Becker, Myers and Schill JB 02 – Farnsworth, Jackson and Todd JFE 02 – Khang RFS 06 – Kisgen and Henry WP 05 – Chen and Peters WP 05 - Qian Conditioning Seems to Work! Some Portfolio Managers Hate it! Things I have Learned

About Empirical Methods: JFE 94 - Foerster JFM 99 – Sarkissian and Simin JF 03 – Sarkissian and Simin RFS 03 - Siegel Review chs: 95, 03 JFQA 06 – Siegel and Xu Wp 05 - Siegel Things I have Learned

About Empirical Methods: JFE 94 - Foerster JFM 99 – Sarkissian and Simin JF 03 – Sarkissian and Simin RFS 03 - Siegel Review chs: 95, 03 JFQA 06 – Siegel and Xu Wp 05 - Siegel The Generalized Method of Moments (GMM): a workhorse! Things I have Learned

About Empirical Methods: JFE 94 - Foerster JFM 99 – Sarkissian and Simin JF 03 – Sarkissian and Simin RFS 03 - Siegel Review chs: 95, 03 JFQA 06 – Siegel and Xu Wp 05 - Siegel The GMM: a workhorse! Beautiful Combination with Stochastic Discount factors: E{mR}=1 “M-Talk!” Things I have Learned

About Empirical Methods: JFE 94 - Foerster JFM 99 – Sarkissian and Simin JF 03 – Sarkissian and Simin RFS 03 - Siegel Review chs: 95, 03 JFQA 06 – Siegel and Xu Wp 05 - Siegel The GMM: a workhorse! E{mR}=1 “M-talk!” HML sorts are tricky (hard to distinguish from data mining)! Things I have Learned

About Empirical Methods: JFE 94 - Foerster JFM 99 – Sarkissian and Simin JF 03 – Sarkissian and Simin RFS 03 - Siegel Review chs: 95, 03 JFQA 06 – Siegel and Xu Wp 05 - Siegel The GMM: a workhorse! E{mR}=1 “M-talk!” HML sorts hard to distinguish from data mining ! Even a Simple Regression might steer you wrong ! Things I have Learned

About How to “Play the Game.” Wharton, 81-83 Chicago, 83-92 Arizona State (V), 94,95,98 South Carolina (V), 98 U. Washington, 92-2001 Miami (V), 98 IAS Vienna (V), 99 Atlanta Fed (V), 2004 Boston College, 2001- . . . . Things I have Learned

About How to “Play the Game.” Wharton, 81-83 Chicago, 83-92 Arizona State (V), 94,95,98 South Carolina (V), 98 U. Washington, 92-2001 Miami (V), 98 IAS Vienna (V), 99 Atlanta Fed (V), 2004 Boston College, 2001- Be valuable to your colleagues. . . . Things I have Learned

About How to “Play the Game.” Wharton, 81-83 Chicago, 83-92 Arizona State (V), 94,95,98 South Carolina (V), 98 U. Washington, 92-2001 Miami (V), 98 IAS Vienna (V), 99 Atlanta Fed (V), 2004 Boston College, 2001- Be valuable to your colleagues. Drill down, but keep your eye on the Big Questions. . . Things I have Learned

About How to “Play the Game.” Wharton, 81-83 Chicago, 83-92 Arizona State (V), 94,95,98 South Carolina (V), 98 U. Washington, 92-2001 Miami (V), 98 IAS Vienna (V), 99 Atlanta Fed (V), 2004 Boston College, 2001- Be valuable to your colleagues. Drill down, but keep your eye on the Big Questions. Juggle the balls, but have FUN with the work. . Things I have Learned

About How to “Play the Game.” Wharton, 81-83 Chicago, 83-92 Arizona State (V), 94,95,98 South Carolina (V), 98 U. Washington, 92-2001 Miami (V), 98 IAS Vienna (V), 99 Atlanta Fed (V), 2004 Boston College, 2001- Be valuable to your colleagues. Drill down, but keep your eye on the Big Questions. Juggle the balls, but have FUN with the work. Follow the “Golden Rule.” Things I have Learned

Some Things I still Wonder about (after 20+ years as an empirical asset pricer)

Some Things I still Wonder about (after 20+ years as an empirical asset pricer) • Why Do some stocks return more than others? . . . .

Some Things I still Wonder about (after 20+ years as an empirical asset pricer) • Why Do some stocks return more than others? • How do Macro forces determine asset prices? . . .

Some Things I still Wonder about (after 20+ years as an empirical asset pricer) • Why Do some stocks return more than others? • How do Macro forces determine asset prices? • Are stock returns Really Predictable over time? . .

Some Things I still Wonder about (after 20+ years as an empirical asset pricer) • Why Do some stocks return more than others? • How do Macro forces determine asset prices? • Are stock returns Really Predictable over time? • How many of our “stylized facts” are really Data Mining? .

Some Things I still Wonder about (after 20+ years as an empirical asset pricer) • Why Do some stocks return more than others? • How do Macro forces determine asset prices? • Are stock returns Really Predictable over time? • How many of our “stylized facts” are really Data Mining? • When will we move beyond the Fama French 3-factor “Model” and FF25 Portfolios?

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • . . • . • . • . • . . • . • .

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • . . • . • . • . • . . • . • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • . . • . • . • . • . . • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • . . • . • . • . • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • . . • . • . • I meet practitioners who actually read my papers! • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • . . • . • Neighbors share their investment wisdom at parties • I meet practitioners who actually read my papers! • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • . . • My doctoral students are teaching me Mandarin • Neighbors share their investment wisdom at parties. • I meet practitioners who actually read my papers! • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • . . • My Dean wonders why I get paid so much to study models that don’t work. • My doctoral students are teaching me Mandarin • Neighbors share their investment wisdom at parties. • I meet practitioners who actually read my papers! • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • . • We make more money than Corporate Finance scholars! • My Dean wonders why I get paid so much to study models that don’t work. • My doctoral students are teaching me Mandarin • Neighbors share their investment wisdom at parties. • I meet practitioners who actually read my papers! • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • . • I get to work on SDFs, use the GMM, stuff like that! • We make more money than Corporate Finance scholars! • My Dean wonders why I get paid so much to study models that don’t work. • My doctoral students are teaching me Mandarin • Neighbors share their investment wisdom at parties. • I meet practitioners who actually read my papers! • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!

Top 10 Reasons I’m Glad to be an Empirical Asset Pricer: • “M Talk” is better than a secret handshake! • I get to work on SDFs, use the GMM, stuff like that! • We make more money than Corporate Finance scholars! • My Dean wonders why I get paid so much to study models that don’t work. • My doctoral students are teaching me Mandarin • Neighbors share their investment wisdom at parties. • I meet practitioners who actually read my papers! • My parents think I’m not working when I’m not teaching. • It kills the conversation so I can work on the airplane. • All my data are machine readable – no hand collection!