Download

1 / 8

80 likes | 176 Views

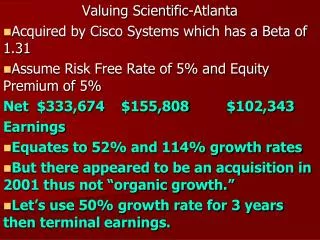

Valuing Scientific-Atlanta Acquired by Cisco Systems which has a Beta of 1.31 Assume Risk Free Rate of 5% and Equity Premium of 5% Net $333,674 $155,808 $102,343 Earnings Equates to 52% and 114% growth rates

E N D

Valuing Scientific-Atlanta Acquired by Cisco Systems which has a Beta of 1.31 Assume Risk Free Rate of 5% and Equity Premium of 5% Net $333,674 $155,808 $102,343 Earnings Equates to 52% and 114% growth rates But there appeared to be an acquisition in 2001 thus not “organic growth.” Let’s use 50% growth rate for 3 years then terminal earnings.

Valuing Scientific-Atlanta Finding Cost of Capital Cost of Capital = RF+(EP*B) 5+(5*1.31)=11.55

Valuing Scientific-Atlanta Year Projected Discount PV Earnings Rate 2002 500,511 11.55 448,687 2003 750,767 11.55 603,345 2004 1,126,151 11.55 811,312 1,863,344 1,126,151 = 9,750,225 6,297,038 .1155 $ 8,160,382 P/E of 24.5 Shares outstanding in 2001 164,899,158 $49.49 per share

Valuing Scientific-Atlanta Alternatives Use unleveraged Beta (but this company has no real debt capital. Use a different measure of earnings like EBITDA for 2001 $577,155 2002 865,733 2003 1,298,600 2004 1,947,900 Yields a value of $11,069,908 Or use an EBITDA multiple (13x 2002 EBITDA, top of the range in the boom of broadband telecom) $11,254,529

Cisco bought it in 2006 for $43 per share or $6.9 billion. There appear to have been a little over 160 million outstanding shares.

Selected Financial Data (Dollars in Thousands, Except per Share Data) 2005 2004 2003 2002 2001 Sales $1,910,892 $ 1,708,004 $ 1,450,353 $ 1,671,117 $ 2,512,016 CostofSales1,195,667 1,073,202 947,581 1,086,961 1,718,160 Sales and Admin 203,118 199,118 191,134 186,579 220,161 R and D 163,543 149,233 146,596 148,652 154,346 Restructuring Expense (291) 1,325 17,446 28,164 — Earnings before Income Taxes 322,907 308,333 152,098 158,435 510,402 Net Earnings$210,760 $ 218,001 $ 100,345 104,384 $333,674 Thus they paid 37.3 times earnings compared to our P/E of 24.5

Net Earnings 210,760 Depreciation 78,954 Interest Expense (298,222) Taxes 112,147 EBITDA 103,639 (price is about 66x) Cash provided by operating $349,614

But press release says the price net of cash balances is really $5.3 billion which is: • PE of 25 and EBITDA multiple of 51