Download

1 / 23

230 likes | 246 Views

Learn how to effectively manage working capital to improve cash flow and ensure financial stability for your firm. Explore the different aspects of working capital accounts and understand the importance of a well-balanced cash flow cycle.

E N D

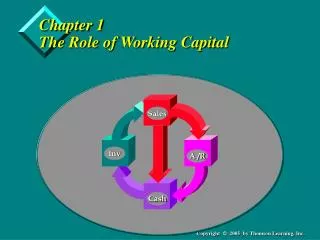

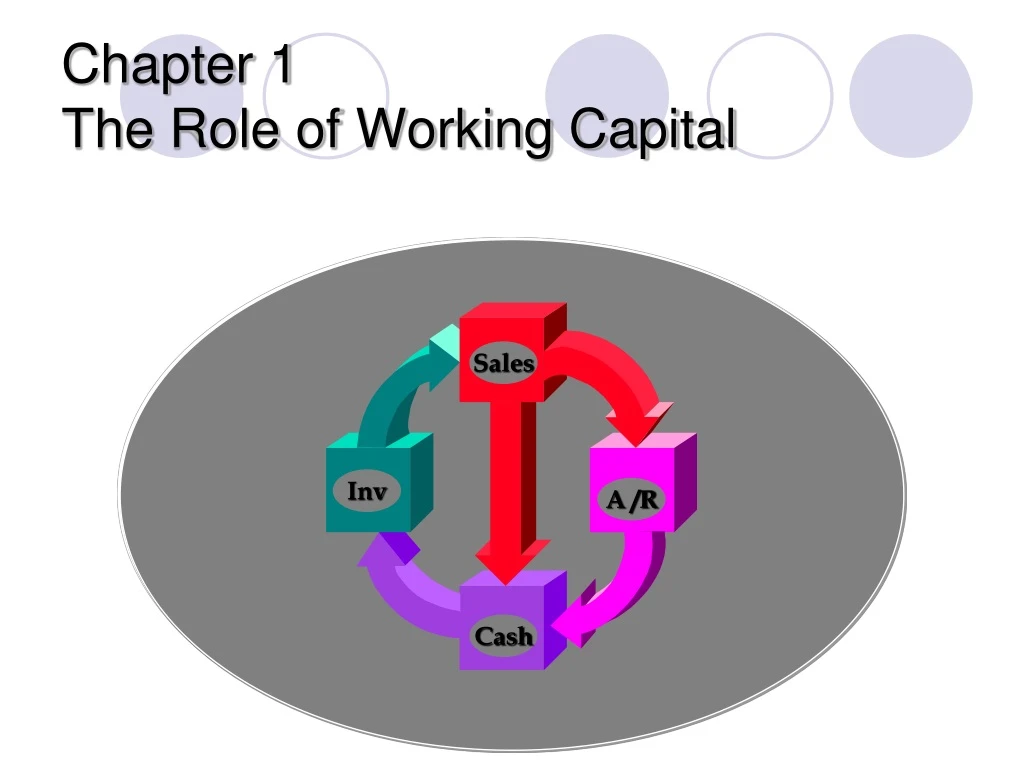

Chapter 1The Role of Working Capital Sales Inv A /R Cash

Objectives View firm as a system of cash flows How Working Capital and depreciation create disparities between profit and cash flow Management aspects of various Working Capital accounts

The Cash Flow Timeline • Order Inventory Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

- Cash conversion period – difference between the date cash is received and cash is paid. • Shorter cash conversion periods imply more efficient working capital policies which leads to increased shareholder wealth.

...in the beginning • Balance Sheet - June 1 • Cash $1,000 Debt $500 • Equity 500 • Total $1,000 Total $1,000

The Next Day, June 2 • The company purchases • Fixed Assets (for $600 cash) • And Inventory (for $300 on account)

The Next Day, June 2 • Balance Sheet - June 2 • Purchase Fixed Assets and Inventory • Cash $ 400 A/P $ 300 • Inventory 300 Debt 500 • Fixed Assets 600 Equity 500 • Total $1,300 Total $1,300

End of June • The company • Sells its inventory for $700 on account • Incurs unpaid operating expenses of $200 • Paid interest and taxes worth $75 • Accumulates $100 of depreciation on its fixed • Assets • Generates profits of $25

End of June • Balance Sheet - June 30 • Sale of product, incur operating expenses, • incur depreciation, and generate profit • Cash $ 325 A/P $ 300 • A/R 700 Accruals 200 • Inventory 0 Debt 500 • Fixed Assets 600 Equity 500 • (Accu. Dep.) (100) Retained Earnings 25 • Total $1,525 Total $1,525

July 1 • Balance Sheet - July 1 • Pay operating accruals with cash • Cash $ 125 A/P $ 300 • A/R 700 Accruals 0 • Inventory 0 Debt 500 • Fixed Assets 600 Common Stock 500 • (Accum Depr) (100) Retained Earnings 25 • Total $1,325 Total $1,325

July 15 • Balance Sheet - July 15 • Pay payables with cash • Cash $ ( 175) A/P $ 0 • A/R 700 Accruals 0 • Inventory 0 Debt 500 • Fixed Assets 600 Common Stock 500 • (Accum Depr) (100) Retained Earnings 25 • Total $1,025 Total $1,025

Profit of $25 but short of cash, -$175, lack of liquid resources • Expenses were paid with cash but cash has not been collected from sales • Needs short term bank loan or a line of credit

July 31 • Balance Sheet - July 31 • Collect accounts receivable • Cash $ 525 A/P $ 0 • A/R 0 Accruals 0 • Inventory 0 Debt 500 • Fixed Assets 600 Common Stock 500 • (Accum Depr) (100) Retained Earnings 25 • Total $1,025 Total $1,025

Profit versus Cash Flow Question: Why did the firm end up with $125 in additional cash while earning a profit of $25? Answer: Some expenses are not cash expenses. Question: Why did the firm run out of cash during its operating cycle? Answer: The cash deficit was due to the differences between the timing of cash disbursements and cash receipts.

Important Points Two basic aspects (objectives) of managing daily operations: The firm must manage its cost structure so that operations are profitable. WC accounts must be managed so that adequate liquidity is maintained.

Managing the Working Capital Cycle The working capital cycle refers to the continual flow of resources through the various working capital accounts. Expansion of the WC asset accounts absorb resources Expansion of WC liability accounts provide resources. Managing Inventory Managing Receivables Managing Payables

Managing Inventory Trade-offs between: stock out costs cost of excess inventory ordering costs Just-In-Time

Managing Receivables Who should receive credit and how much? 5 C’s of Credit Character Capacity to Pay Collateral Condition Capital

Managing Receivables Credit terms: n/30 or 2/10, n/30 Monitoring the outstanding balance Speeding up the receipt of payments Reducing collection float Collection float – delay in collecting payment on behalf of the seller Disbursement float – delay in collecting payment on behalf of the supplier

Managing Payables Considered as interest-free-financing Search for terms that match with cash receipts Timing of payment Controlled disbursement

Cash and Short-term Investments Working Capital Cycle concludes with collection of cash Liquid reserves Distributions to shareholders New investment Amortization of debt Rationale for liquid reserves include: Funding daily operations Buffering against adverse conditions Attracting new shareholders by serving as a marketing tool Funding strategic acquisitions

Is Working Capital Needed? One view Optimal level is zero WC is an idle resource Provides little or no value How much in resources to commit? -The optimal investment in working capital is debatable

Summary Firm must operate at a profitable level. A profitable firm may still struggle financially. Working capital soaks up cash flow and may cause an otherwise profitable firm to fail. A successful firm’s operation is managed from a Profit, and a Cash flow perspective.