Download

1 / 7

70 likes | 82 Views

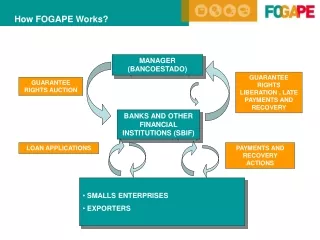

How FOGAPE Works?. MANAGER (BANCOESTADO). GUARANTEE RIGHTS LIBERATION , LATE PAYMENTS AND RECOVERY. GUARANTEE RIGHTS AUCTION. BANKS AND OTHER FINANCIAL INSTITUTIONS (SBIF). LOAN APPLICATIONS. PAYMENTS AND RECOVERY ACTIONS. SMALLS ENTERPRISES EXPORTERS. Auction example.

E N D

How FOGAPE Works? MANAGER (BANCOESTADO) GUARANTEE RIGHTS LIBERATION , LATE PAYMENTS AND RECOVERY GUARANTEE RIGHTS AUCTION BANKS AND OTHER FINANCIAL INSTITUTIONS (SBIF) LOAN APPLICATIONS PAYMENTS AND RECOVERY ACTIONS • SMALLS ENTERPRISES • EXPORTERS

Auction example Auction Amount: US$ 39.600.000, Max. Rate: 80%. 19.360.000 US$. 39.600.000 US$. - Institutions Demand US$ 49.720.000 - It is sorted by lowest rate guarantee - Institutions with the same bid rate receive amounts in proportion to their bid amount

Leverage Effect Guarantee System 10 Times Resources Financial Institutions Capital mitigation Financial Institutions Legal leverage: Equity x 10 (maximum) Increase the resources of FS

Leverage with reinsurance Guarantee System Insurance Company, Multilateral organism, etc. More than10 Times Capital mitigation Financial Institutions Financial Institutions With reinsurance: More resources (guarantee rigths) to financial institutions

Reinsurance: Potential scheme 100% of Portfolio Excess losses 2% (Income from commission) 1,9% Expected Losses Max. (Total Assets)

BASEL II Requirements for guarantees admissible as mitigating risk in Basel II 1. Legal certainty: the documentation that formalizes the guarantee is legally binding and enforceable. 2. Direct protection: the guarantee represents a creditor's right in front of the financial guarantor. 3. Explicit protection: the guarantee must be explicitly documented, so that the scope of coverage is clearly defined and unquestionable. The documentation should make explicit reference to the operation or operations endorsed. 4. Irrevocable protection: the contract contains no clause allowing the guarantor to unilaterally cancel coverage issued or to increase the cost of the guarantee in the case of deterioration in the quality of the covered position. 5. Unconditional protection: No clause of the contract should allow the guarantor to not pay if there is a default. No clause should escape the direct control of the financial institution. 6. Protection Policy: For the recovery of the coverage in the event of default, there is no requirement that the financial institution previously performed legal actions against the debtor. The guarantor requirement covers only the amount subject to coverage, or assumed future payment of the obligations under coverage. 7. Protection fitted temporarily: The residual maturity of protection must be equal to or greater than the underlying exposure.