Download

1 / 11

110 likes | 320 Views

Cost-Benefit Analysis. Delia Prieto University of Miami December 10, 2011. Purpose & Uses of CBA. Purpose : To determine whether a program brings a net gain (total benefits should outweigh the costs) and to facilitate efficient allocation of resources. Uses :

E N D

Cost-Benefit Analysis Delia Prieto University of Miami December 10, 2011

Purpose & Uses of CBA Purpose: To determine whether a program brings a net gain (total benefits should outweigh the costs) and to facilitate efficient allocation of resources. Uses: • To determine continuation (or discontinuation) of the program • To determine the need for changes • To verify the cost-effectiveness

3 Basic Steps • Establish a common measurement unit - usually money • Quantify the costs of doing the project and the resultant benefits • Calculate the “pay-back” time for the project (time to get to the “break even” point)

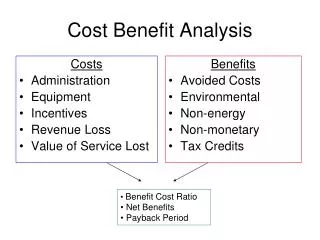

Benefits Cost-Benefit Ratio = Costs

Types of Costs • Variable costs: those that vary depending on the level of program activity (i.e. costs may increase if number of participants increase) • Fixed costs: those that remain the same throughout the program • Incremental costs: those covered daily which are essential for the program to run (i.e. staff salaries) • Sunk costs: those that have been incurred since inception (i.e. the difference between the original cost of a car and its current value) • Opportunity costs: those that would be incurred to implement a policy

Types of Benefits • Primary benefits: occur as a direct result of the program (i.e. participant quits drug-use) • Secondary benefits: received as a consequence of the participant making some changes as a direct result of the program (i.e. successful drug rehab leads to less crime) • Discounting: calculating the current value of future benefits. Benefits expected to occur in the future should be included; however, assumptions will inevitable if discounting occurs.

Comparing outcomes to costs • Calculate how much money would have been saved if the program was not implemented • i.e. how much money would a student have earned if worked instead of going through college for the four years? (Cost of tuition, books, fees minus living expenses) • Difficulty converting the costs and benefits to the same units • Money vs. Life/health • Consider how long it will take to get to the “break even” point (the calculated point in time where cost savings match accumulated development expenses)

CBA of Prevention programs Return on investment of prevention programs range from $2-$20.

Criticisms of CBA • Psychological benefits are hard to price • Value of lives cannot be estimated in a dollar amount • Cost-benefit analyses require major assumptions when estimating future costs and benefits • To address this issue, some calculate a range of cost-benefit ratios by using different assumptions (sensitivity analysis). If the program appears to be cost-effective regardless of the assumptions made, conclusions take on more credibility