Download

1 / 2

20 likes | 30 Views

Check out the TDS rates with effect from 1st April 2021. Tax Deduction at Source (TDS) rates for the following non-salaried defined payments made to residents have been reduced for the period from 14 May 2020 to 31 March 2021, in order to provide more funds to taxpayers to deal with the economic situation caused by the COVID-19 pandemic. The following are the TDS and TCS thresholds in effect as of April 1, 2021.

E N D

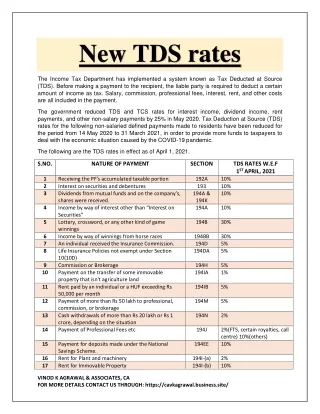

New TDS rates The Income Tax Department has implemented a system known as Tax Deducted at Source (TDS). Before making a payment to the recipient, the liable party is required to deduct a certain amount of income as tax. Salary, commission, professional fees, interest, rent, and other costs are all included in the payment. The government reduced TDS and TCS rates for interest income, dividend income, rent payments, and other non-salary payments by 25% in May 2020. Tax Deduction at Source (TDS) rates for the following non-salaried defined payments made to residents have been reduced for the period from 14 May 2020 to 31 March 2021, in order to provide more funds to taxpayers to deal with the economic situation caused by the COVID-19 pandemic. The following are the TDS rates in effect as of April 1, 2021. S.NO. NATURE OF PAYMENT SECTION TDS RATES W.E.F 1ST APRIL, 2021 1 2 3 Receiving the PF's accumulated taxable portion Interest on securities and debentures Dividends from mutual funds and on the company’s, shares were received. Income by way of interest other than “Interest on Securities” Lottery, crossword, or any other kind of game winnings Income by way of winnings from horse races An individual received the Insurance Commission. Life Insurance Policies not exempt under Section 10(10D) Commission or Brokerage Payment on the transfer of some immovable property that isn't agriculture land Rent paid by an individual or a HUF exceeding Rs 50,000 per month Payment of more than Rs 50 lakh to professional, commission, or brokerage Cash withdrawals of more than Rs 20 lakh or Rs 1 crore, depending on the situation Payment of Professional Fees etc 192A 193 194A & 194K 194A 10% 10% 10% 4 10% 5 194B 30% 6 7 8 194BB 194D 194DA 30% 5% 5% 9 10 194H 194IA 5% 1% 11 194IB 5% 12 194M 5% 13 194N 2% 14 194J 2%(FTS, certain royalties, call centre) 10%(others) 10% 15 Payment for deposits made under the National Savings Scheme. Rent for Plant and machinery Rent for Immovable Property 194EE 16 17 194I-(a) 194I-(b) 2% 10% VINOD K AGRAWAL & ASSOCIATES, CA FOR MORE DETAILS CONTACT US THROUGH: https://cavkagrawal.business.site/

In budget 2021, the finance minister proposed higher TDS (tax deducted at source) or TCS (tax collected at source) rates in order to encourage more citizens to file income tax returns (ITR). The budget proposes adding new Sections 206AB and 206CCA to the Income Tax Act as a special provision for the deduction of higher TDS and TCS rates for non-filers of an income tax return, respectively. Individuals that have not paid income tax returns but have a TDS or TCS deduction of more than Rs 50,000 in the previous two years would be required to pay TDS or TCS at a rate of at least 5%. The deductor will also be in charge of obtaining ITR evidence from individuals in order to ensure compliance. VINOD K AGRAWAL & ASSOCIATES, CA FOR MORE DETAILS CONTACT US THROUGH: https://cavkagrawal.business.site/