1 / 2

20 likes | 24 Views

If an assessee sells a capital asset that is part of a block of assets (building, machinery, etc.) on which depreciation has been permitted under the Income Tax Act, the income derived from such capital asset is regarded as short term capital gain under section 50 of the Income Tax Act.

E N D

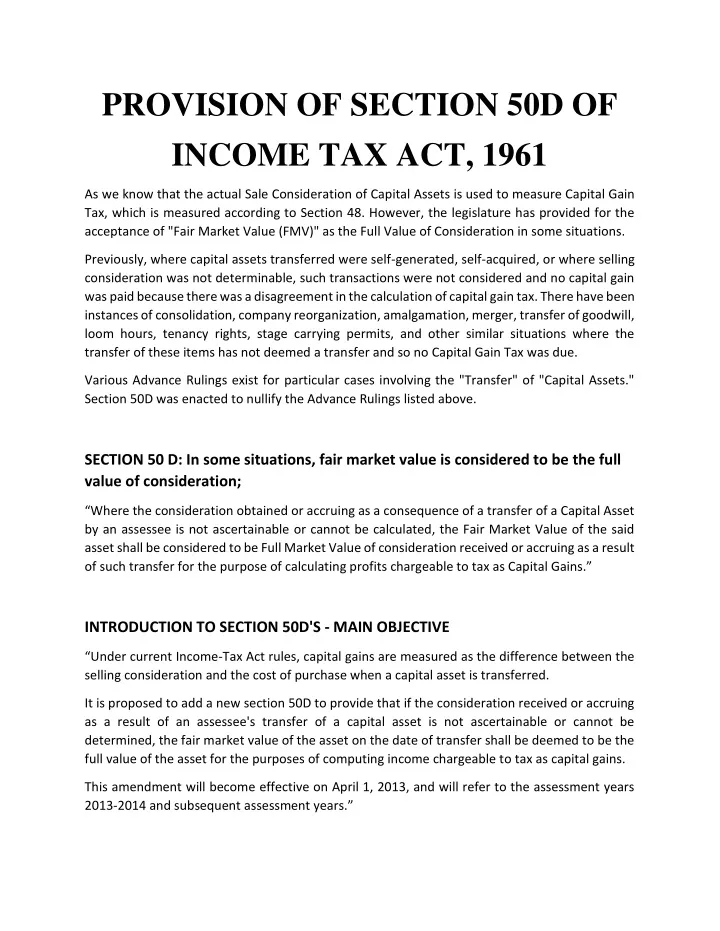

PROVISION OF SECTION 50D OF INCOME TAX ACT, 1961 As we know that the actual Sale Consideration of Capital Assets is used to measure Capital Gain Tax, which is measured according to Section 48. However, the legislature has provided for the acceptance of "Fair Market Value (FMV)" as the Full Value of Consideration in some situations. Previously, where capital assets transferred were self-generated, self-acquired, or where selling consideration was not determinable, such transactions were not considered and no capital gain was paid because there was a disagreement in the calculation of capital gain tax. There have been instances of consolidation, company reorganization, amalgamation, merger, transfer of goodwill, loom hours, tenancy rights, stage carrying permits, and other similar situations where the transfer of these items has not deemed a transfer and so no Capital Gain Tax was due. Various Advance Rulings exist for particular cases involving the "Transfer" of "Capital Assets." Section 50D was enacted to nullify the Advance Rulings listed above. SECTION 50 D: In some situations, fair market value is considered to be the full value of consideration; “Where the consideration obtained or accruing as a consequence of a transfer of a Capital Asset by an assessee is not ascertainable or cannot be calculated, the Fair Market Value of the said asset shall be considered to be Full Market Value of consideration received or accruing as a result of such transfer for the purpose of calculating profits chargeable to tax as Capital Gains.” INTRODUCTION TO SECTION 50D'S - MAIN OBJECTIVE “Under current Income-Tax Act rules, capital gains are measured as the difference between the selling consideration and the cost of purchase when a capital asset is transferred. It is proposed to add a new section 50D to provide that if the consideration received or accruing as a result of an assessee's transfer of a capital asset is not ascertainable or cannot be determined, the fair market value of the asset on the date of transfer shall be deemed to be the full value of the asset for the purposes of computing income chargeable to tax as capital gains. This amendment will become effective on April 1, 2013, and will refer to the assessment years 2013-2014 and subsequent assessment years.”

SALIENT FEATURES OF SECTION 50D PROVISION a)A Capital Asset must be transferred; for this section to apply, the asset transferred must be of the form of a Capital Asset and not a business asset, stock in the broker, or other similar assets; the Capital Assets transferred must be protected by the concept of Capital Assets under Section 2(47) of the Act, 1961. It must be a complete and irreversible transition, not a conditional or partial transfer. b)The consideration for such a transfer is unknown or unable to be determined; the value of the Capital Asset transferred must be unknown or unable to be determined. Provisions apply in cases where the Sale Consideration is listed as NIL in a contract between the parties, but this is a contentious problem. c)The Capital Gain on such a transfer is taxable in the previous year in which the Capital Asset is transferred, regardless of whether or not a selling consideration is obtained. Please keep in mind that the actual realization of the sale consideration has no bearing on the capital gain tax liability. d)The Sale Consideration for capital gains tax purposes is the Fair Market Value of the asset at the time of transition.

![Technicalities of Section 68 to 69D w.r.t 155BBE and Panel Provisions [Under Income Tax Act, 1961]](https://cdn4.slideserve.com/1089885/technicalities-of-section-68-to-69d-w-r-t-155bbe-dt.jpg)

![Presumptive Income u/s 44AD of Income Tax Act, 1961 [w.e.f. AY 2011- 12]](https://cdn2.slideserve.com/4851709/slide1-dt.jpg)