Cost analysis

COST MANAGEMENT BASICS. Cost analysis. Agenda. Cost Estimating Types of Cost Normalization and Inflation Risk Assessment Cost Estimating Methods Labor Costing Optimization Statistical Analysis Tools . Cost Estimating. Cost and Cost Estimating Definition. Cost:

Cost analysis

E N D

Presentation Transcript

COST MANAGEMENT BASICS Cost analysis

Agenda Cost Estimating Types of Cost Normalization and Inflation Risk Assessment Cost Estimating Methods Labor Costing Optimization Statistical Analysis Tools

Cost and Cost Estimating Definition Cost: The monetary representation of resources used or sacrificed, and liabilities incurred to achieve an objective Example: The resources expended in acquiring or producing a good The resources expended in performing an activity or service Cost Estimating: The process of collecting and analyzing data and applying quantitative models, techniques, tools, and databases to estimate the future cost of an item, product, program, or task Cost estimating is thought by some to be difficult, but the skills and knowledge are logical and straightforward.

Purpose of Cost Estimating • Enable managers to: • Make resource-informed decisions • Develop and defend budgets • Identify specific cost drivers • Improve cost controls • Translate system/functional needs associated with programs, projects, proposals, or processes into costs • Determine and communicate a realistic view of the probable costs, which will be used to inform the decision-making process.

Characteristics of a Good Cost Estimate Well documented Includes source data and its significance Clear and detailed calculations and results Contains explanations for choosing a particular method or reference Comprehensive Ensures a level of detail where cost elements are neither omitted nor double counted Accurate Avoids bias and overly conservative or optimistic estimates Bases its assessments on most likely scenarios and assumptions Credible Discusses any limitations of the analysis deriving from the uncertainty/bias of the data or assumptions

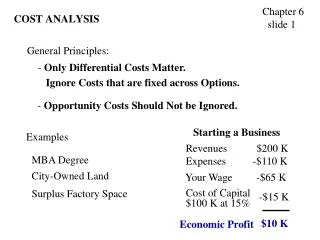

Types of Cost • Sunk Costs • Opportunity Costs • Marginal Costs • Average Costs

Sunk Costs • Costs that have already been incurred and cannot be changed no matter what action is taken in the future are called Sunk Costs Example: Paul is assembling his new home theatre system. He has spent 5 hours thus far and estimates he will complete the assembly in 2 more hours. Joan informs him he is doing it the hard way and describes a simpler approach which will take one hour to undo his work and re-assemble the system. 7

Opportunity Costs • The size of a foregone opportunity of using a resource is the Opportunity Cost Example: The opportunity cost of accepting a job is forgoing the opportunity to do something else with our time If our best alternative to working is playing golf the opportunity cost of working is the forgone opportunity of playing golf If the opportunity to play golf has a value greater than the benefits of working we will choose to play golf 8

Marginal Costs • Marginal Costs are the costs to produce one more additional unit or output • The slope of the ‘Total Cost Curve’ at any given level of production is the marginal cost for one more unit • Marginal costs are highest at very low output rates and at output rates near capacity

B Lowest marginal costs Marginal Costs Total cost C High marginal costs Total (£) A High marginal costs Output 10

Average Costs • Average Costis calculated by dividing the total cost by the total units produced • Average Cost is very high at low levels of output

Cost Drivers Organizations perform work activities to deliver products/services to a stakeholder Definition: Factors, activities, or events that cause costs to be incurred Usually can be quantified/measured - e.g., number of hours spent on a task, supported population Analyst should identify and focus on the primary cost drivers that affect total cost Helps to ensure the accuracy and reliability of the cost estimate Makes it easier to control costs within the organization Examples: The labor cost associated with assembling a HMMWV at a the factory would be driven by the quantity of vehicles produced Energy consumption at the PX is driven by the square footage of the building and the operating hours The cost of printing budget documents for the Office of Management and Budget is driven by the number of pages in each set and the number of sets needed

Comparative Analyses Supporting Resource Informed Decision EA is an OSD MAIS required analysis in support of investment decision at early IT/ERP program concept phase MS-A with an update at MS-B decision. EA is also required by the Army CoE in support of Military construction decision. (MAIS) Major Automated Information System programs AoA is an OSD MDAP required analysis in support of acquisition requirement decision at early program concept phase MS-A with an update at MS-B decision. AoA is a formal and elaborate study that in addition to the program life cycle, often includes an operational model done by TRADOC for the Army ASARC and OSD DAB decisions. (MDAP) Major Defense Acquisition Programs BCA is an OSD MDAP required analysis at post production phase in support of Performance Based Logistics (PBL) Contractor Logistic Support (CLS) vs. organic O&S decision. Risk analysis is an essential component of BCA. BCA term is often synonymous with CBA for non-PBL analysis. CBA is an Army required analysis for all new and existing initiatives at resource decision forums with cost of $10M or more. CBA for Army HQ decision is developed by the initiative advocate and reviewed by the CBA-RB . AMC and TRADOC also have similar process for their internal resource decisions.

Break-Even Point Cost Reduction = Upfront Investment Break-Even Point: Used when a given alternative has a significant investment cost but is expected to experience cost reduction in future years This is also where (in current dollars): savings = investment

Example - Break-Even Point Summary of Break-Even Point: - It’s the year where the savings become positive. - Using inflation indices, constant dollars are converted into current dollars. - Savings are the difference between cumulative costs.

The annualized effective compounded return rate Rate where the present value of cash inflows is equal to the present value of cash outflows IRR = (FV/PV)1/N -1 Internal Rate of Return (IRR)

Net Present Value Net Present Value (NPV): • The difference between the present value of cash inflows and the present value of cash outflows • Used to analyze the profitability of an investment • This works only if values, costs (outflows), and benefits (inflows) are quantified into monetary terms

Net Present Value Formula Net Present Value (NPV): • The amount of dollars that would have to be invested during the base year at the assumed discount (interest) rate to cover the costs, match the revenues, or match the savings at a specific point in the future NPV = PV (benefits) – PV (costs)

Cost Estimating in EA Must consider the “Economic Life” • Period of time over which the benefits to be gained from a project may reasonably be expected to accrue. Benefits are limited by the equipment or facility’s physical and technological life • Measured against a stipulated level of threat, or represent a period during which a given mission or function is required or can be supported

The sum of all costs required to research, develop, test, procure, field, operate, sustain, and dispose a system A planning number that often differs from the sum of budgeted amounts allocated towards or in support of a particular system Total Life Cycle Cost (LCC)

Ratios compare the profits or savings of an investment cost to illustrate the relativity of cost and savings S/IR = OPERATING COST SAVINGS COST OF INVESTMENT If S/IR > 1, then positive investment Investment Multiples/Ratios

Business Cases Analysis (BCA): Key Questions Is the proposed solution: • Financially Viable (Make Economic Sense) • Optimal (Best Value or Increased Effectiveness) • Feasible (Assessing Constraints) • Implementable (Risks & 2nd/3rd Order Effects)

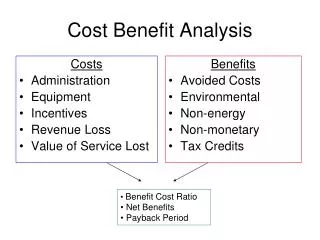

Cost Benefit Analysis (CBA) Within the Department of the Army, one major process which incorporates cost analysis is Cost Benefit Analysis (CBA)

What is a CBA? Cost-Benefit Analysis: • Is a structured methodology used to identify alternative solutions to a problem, determine the costs and benefits of each alternative, define the appropriate decision criteria, and select the best alternative • Produces a strong value proposition – a clear statement that the benefits outweigh the costs and risks. • In Basic Terms: • Define a problem or opportunity • Identify alternatives • Determine their costs and benefits • Evaluate and select the best alternative

Why Do We Need CBAs? Purpose: • Supplement (but not replace) professional experience, subject matter expertise, and military judgment with rigorous analytical techniques • Make best possible use of constrained resources • When making resource decisions: • Ensure that all decisions are resource-informed • Treat cost as a consideration from the outset, not as an afterthought • Understand how much benefit will be derived • Identify billpayers • Consider second- and third-order effects

CBA and the “Cost Culture” CBA is part of a high-priority initiative to inculcate a cost culture throughout the Army. • In any organization, “culture” is the beliefs and principles that guide the behavior of the people in that organization. • Example: The Army’s military culture is based on mission accomplishment, selfless service, valor, and dedication. These concepts establish the foundation for how Soldiers and Civilians go about their duties. • In a cost culture: • Cost is an integral part of every decision • Soldiers and Civilians strive to find better and more cost effective ways to operate the Army enterprise • Leaders at all levels engage in cost control and management activities, which are supported by talented cost staffs

Cost Benefit Analysis CBA – Using analysis to make the case for a project or proposal: Weighing the total expected costs against the total expected benefits over the near, far, and lifecycle timeframes from an Army enterpriseperspective • BENEFITS • The total of quantifiable and non-quantifiable benefits • Quantifiable benefits • Cost Savings • Cost Avoidances • Non-Quantifiable benefits • Greater capability • Faster availability • Better quality • Improved morale • Other? • COSTS • Quantifiable costs • Direct • Indirect • Initial/Start up • Sustainment • Procurement • Non-Quantifiable costs • Life/Safety/Health • Perception/Image • Opportunity • Risk/Uncertainty • Political BENEFITS MUST BALANCE OR OUTWEIGH COSTS

Objective Recommendation Assumptions Sensitivity Analysis Alternatives Compare Alternatives Cost Estimates Benefits Estimate Selection Criteria CBA is NOT a Linear Process • At any step in the process, the team’s findings and analysis might make it necessary to revisit previous steps • Significant findings might require asking the decision maker for revised guidance

Normalization and Inflation • Adjusting for inflation is a specific form of normalization, an adjustment intended to make a given data set consistent and comparable with other data sets • A frequent use of simple normalization is to adjust based on quantities. For example: • In a manufacturing process, COA 1 produces 17,000 widgets per year at a total cost of $33,765 and COA 2 produces 14,500 widgets at a total cost of $28,725. It’s difficult to evaluate these COAs unless we normalize by computing a unit cost, which shows us that COA 2, with a unit cost of $1.95 per widget, is preferable to COA 1, which has a unit cost of $1.99.

What is Inflation? Definition • A rise in the general level of prices • Measure of change in the dollars’ purchasing power • In other words: • A given dollar amount will have less buying power next year than it does this year • To maintain consistent buying power, we must adjust this year’s dollars with the inflation factor from year to year Common methods for normalization: • Discounting • Constant (Base) Year Of all the topics discussed in cost analysis, none will be encountered more frequently than inflation

Inflation Calculation and Examples • Basic calculations: • (Constant Dollars) * (Inflation Factor) = Current (Dollars) • Inflation is compounded from year to year (i.e., multiplied, not added). • Example: A loaf of bread in 1950 cost $0.25. Today, in 2012, it costs $3.00.

Example—Current Dollar Calculation • Data: We’ve calculated the annual cost for a given COA in FY12 constant dollars: • Civilian personnel: $145,000 • Contract support: $100,000 (paid by OMA appropriation) • Applicable inflation factors: • Civilian personnel: 2% per year • OMA appropriation: 3% per year • Calculation for the first three years of the life-cycle:

Risk Assessment and Mitigation The goal of risk assessment is to answer questions like: What risks may occur? What is the likelihood that risks will occur? Are the source of these risks internal or external? What causes these risks? What are the consequences if the risks go unresolved? What assets, operations, activities, functions, etc. will be affected as a result? How much risk is tolerable? What should be done to anticipate and limit risks? Always measure the risk by the potential adverse impacts on alternatives.

Types of Risks Business/Programmatic Risk: Affects the budget and viability of a program Operational Risk: Affects the ability to perform a mission Process Risk: Associated with failing to meet standards and performance benchmarks in a newly established process Technical Risk: Associated with failing to develop or implement technology Schedule Risk: Associated with allocating time to perform and manage tasks Organizational Risk: Associated with managementchanges

Ways to Measure/Address Risk • Methods of measuring and/or addressing risk include, but are not limited to: • Effective Mean • Cost of Risk Mitigation

Effective Mean (Expected Value) • The effective mean, or expected value, of a measurable quantity is the sum of all possible outcomes multiplied by their corresponding probabilities • Example: if the cost of a new ground combat vehicle is judged to be $1.4M with 50% probability, $2M with 25% probability, and $1.2M with 25% probability, then the effective mean (expected cost) is $1.4M x 0.5 + $2M x 0.25 + $1.2M x 0.25 = $1.5M. • Example: if inter-theater transit time for a sustainment brigade is projected to be 5 days with 90% probability and 4 days with 10% probability, then the expected transit time is 5 x 0.9 + 4 x 0.1 = 4.9 days.

Cost of Risk Mitigation If a cost can be associated with reducing risk, then risk can be measured by that monetary value. Example: If for $22K extra, the risk of a schedule over-run can be reduced from 15% to 3%, then $22K can be a measure for the difference in risk.

Cost Estimating Principles and Rules • Use authoritative data sources • Ensure that cost estimates support “apples-to-apples” comparison among COAs • Ensure the cost estimate is well-documented, comprehensive, accurate, and credible • Constant vs. current dollars • Use constant (un-inflated) dollars for even comparison for COAs in CBAs • Convert estimate to current (inflated) dollars to determine POM/budget resourcing requirements

Available Cost Estimating Methods Available methods: • Analogy • Parametric • Engineering • Actual Cost • Expert Opinion • Learning Curves Most CBAs utilize all cost estimating methods

Cost Estimating Methods The use of each method is based on the information available to support it. GROSS ESTIMATES DETAILED ESTIMATES Parametric Actual Costs Engineering Analogy Figure 1: A summary of the usual application of each technique.

Analogy Method • Estimates the cost, based on historical data, of an analogous system or subsystem • Utilizes a current fielded system that is similarly designed to the proposed system • Adjusts historical cost of the current system to account for differences • Adjustments should be made through parameters/scaling factors based on quantitative data • These adjustments should show validity of comparison When is it used? • When an analogous case (that can be applied to a subsystem or component level) exists

Attribute Old System New System Engine: F-100 F-200 Thrust: 12,000 lbs 16,000 lbs Cost: $5.2M ? Q: What is the unit cost of the F-200? A: $5.2M * (16,000/12,000) = $6.9M Analogy Method Example Warning 2: An adjusted analogy is, by definition, estimating outside the range of the data. Warning 1: An adjusted analogy is like a regression, but the slope is just a guess.

Parametric Method • Uses regression or other statistical methods to develop a cost estimating relationship based on observed patterns of how specific parameters influence total cost • Utilizes: • High-level ‘Work Breakdown Structure’ (top down approach) • A database from elements of one or more systems When is it used? • Historical data is available but not detailed • In earlier stages of the system or project life cycle

Parametric Method Example High Mobility Wheeled Vehicles Database Is ‘Cubic Ft Shipping’ a good predictor of cost? Cost of Gross Curb Cubic Ft Net VehicleFirst UnitWeightWeightShippingHorsepower M274 $ 9,585 1,770 970 81.6 12.5 M561 50,002 8,363 5,363 732.3 93 M656 93,262 24,785 14,785 1,227 183 M520 147,889 36,590 10,500 2,368 176

Parametric Method Example (Cont’d) Cost of First Unit = 60.992 * (Cubic Shipping Feet) + 7,957.2 We can estimate the cost of any vehicle given the shipping capacity using the above equation.