Download

1 / 4

40 likes | 52 Views

Gratuity of Rs 12 lakhs received by Mr. Gupta from his employer (Indian Railway and Tourism Corporation Ltd. (IRCTC) u2013 Gratuity income of Mr. Gupta will be exempt from tax as he is a government employee.<br><br>Read more: https://www.taxgyata.com/ap/gratuity-and-its-taxability/

E N D

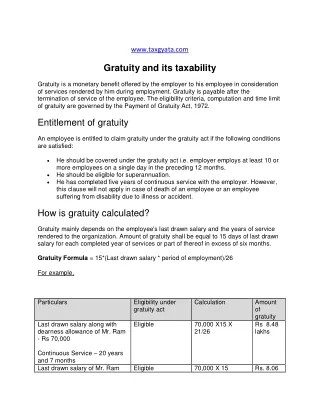

www.taxgyata.com Gratuity and its taxability Gratuity is a monetary benefit offered by the employer to his employee in consideration of services rendered by him during employment. Gratuity is payable after the termination of service of the employee. The eligibility criteria, computation and time limit of gratuity are governed by the Payment of Gratuity Act, 1972. Entitlement of gratuity An employee is entitled to claim gratuity under the gratuity act if the following conditions are satisfied: He should be covered under the gratuity act i.e. employer employs at least 10 or more employees on a single day in the preceding 12 months. He should be eligible for superannuation. He has completed five years of continuous service with the employer. However, this clause will not apply in case of death of an employee or an employee suffering from disability due to illness or accident. How is gratuity calculated? Gratuity mainly depends on the employee's last drawn salary and the years of service rendered to the organization. Amount of gratuity shall be equal to 15 days of last drawn salary for each completed year of services or part of thereof in excess of six months. Gratuity Formula = 15*(Last drawn salary * period of employment)/26 For example, Particulars Eligibility under gratuity act Calculation Amount of gratuity Rs 8.48 lakhs Last drawn salary along with dearness allowance of Mr. Ram - Rs 70,000 Eligible 70,000 X15 X 21/26 Continuous Service – 20 years and 7 months Last drawn salary of Mr. Ram Eligible 70,000 X 15 Rs. 8.06

along with dearness allowance - Rs 60,000 X 20/26 lakhs Continuous Service – 20 years and 4 months Last drawn salary of Mr. ABC - Rs 60,000 Not eligible NA NA Continuous Service – 4 years and 2 months The organisation can choose to pay the employee more, but the maximum amount of gratuity, as per law cannot exceed Rs. 20 lacs. Amounts paid above this will be ex- gratia. Time limit for gratuity payment The employee will send an application to the organization for payment of gratuity. The employer will acknowledge and send a reply to the employee and controlling authority with the amount specified Employer shall pay gratuity within 30 days from the date of acknowledgment. Rules for forfeiture of gratuity According to Gratuity Act, an employer holds the right to forfeit the gratuity payment either wholly or partially if the employee has been terminated from service due to the following reasons. Unlawful act done by him during employment; Violence behavior during employment; Involvement in offence include moral turpitude Gratuity under Income Tax Act Treatment of gratuity under Income Tax depends on the type of employee who is receiving the gratuity. 1. The gratuity received by a government employee is fully exempted from tax. 2. In case of gratuity received by a non-government employee who is covered under The Payment of Gratuity Act, lower of the following will be exempt from tax: a) Gratuity actually received,

b) Rs 20 lakhs, c) Last drawn salary* no. of years of employment * 15/26 3. In case of gratuity received by non government employee who is not covered under The Payment of Gratuity Act, lower of following shall be exempt from tax: a) Gratuity actually received, b) Rs 10 lakhs, c) Last 10 month average salary* no. of years of employment * 15/30 illustrations illustration 1: Gratuity of Rs 12 lakhs received by Mr. Gupta from his employer (Indian Railway and Tourism Corporation Ltd. (IRCTC) – Gratuity income of Mr. Gupta will be exempt from tax as he is a government employee. illustration 2: Gratuity of Rs 21 lakhs received by a non-government employee who is covered under gratuity act. Particulars Scenario 1 Scenario 1 Scenario 3 Last drawn salary 1 lakhs ,1 lakhs 2 lakhs Period of employment 20 years 20 years 20 years Gratuity actually received 21 lakhs 21 lakhs 21 lakhs Exemption least of following: 21 lakhs 21 lakhs 21 lakhs a)Gratuity Actually received b)Last drawn salary*15*20/26 c)Threshold limit 11.54 lakhs 11.54 lakhs 23.08 lakhs 20 Lakhs 20 Lakhs 20 Lakhs Exemption available 11.54 lakhs 11.54 lakhs 20 lakhs Gratuity Taxable 8.46 lakhs 8.46 lakhs 1 lakhs illustration 3: Gratuity of Rs 11 lakhs received by a non-government employee who is not covered under gratuity.

Particulars Scenario 1 Scenario 1 Scenario 3 10 month average salary (X) 1 lakhs ,1 lakhs 2 lakhs Period of employment (Y) 15 years 15 years 20 years Gratuity actually received (Z) 11 lakhs 11 lakhs 11 lakhs Exemption least of following: 11 lakhs 11 lakhs 11 lakhs a) Gratuity Actually received b) X*Y*15/30 7.50 lakhs 7.50 lakhs 15.00 lakhs 10 Lakhs 10 Lakhs 10 Lakhs c) Threshold limit Exemption available 7.5 lakhs 7.5 lakhs 10 lakhs Gratuity Taxable 3.5 lakhs 8.46 lakhs 1 lakhs Retirement BenefitsIncome TaxIncome Tax Act Source: https://www.taxgyata.com/ap/gratuity-and-its-taxability/