Understanding Portfolio Diversification and the Efficient Frontier in Finance

This text explores key concepts in portfolio theory, including the limits of diversification, the role of risk-free securities, and the efficient frontier. It outlines the mathematical foundations of portfolio risk and return, emphasizing the separation theorem and the capital market line. It highlights assumptions such as investors' mean-variance preferences, the distribution of asset returns, and the absence of market frictions. Key relations like the Capital Asset Pricing Model (CAPM) and the contribution of individual stocks to portfolio risk are also examined, providing essential insights for investors.

Understanding Portfolio Diversification and the Efficient Frontier in Finance

E N D

Presentation Transcript

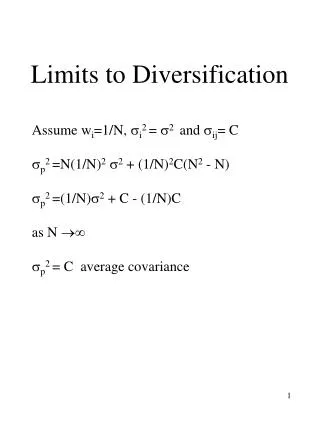

Limits to Diversification Assume wi=1/N, i2 = 2 and ij= C p2 =N(1/N)2 2 + (1/N)2C(N2 - N) p2 =(1/N)2 + C - (1/N)C as N p2 = C average covariance

Presence of Risk free Security Rf = risk free rate 2f = 0 Combining risk free asset and a risky portfolio: E(Rp) = wf E(Rf) + wA E(RA) p2 =wA A2 E(RA) Rf A

Efficient Frontier E(R) Efficient frontier Opportunity set Efficient Frontier: the upper boundary of the opportunity set

Assumptions • Investors can choose on the basis of mean-variance criterion • Normal distribution of asset returns or quadratic utility function • Investors have homogeneous expectations • planning horizon • distribution of security returns • There are no frictions in the capital markets • no transactions costs • no taxes on dividends, capital gains, interest income • Information available at no cost

Efficient Frontier with Risk Free Security E(R) M Rf M is the market portfolio

Risk and Return Capital Market Line: Separation Theorem: The determination of optimal portfolio of risky assets is independent from individual’s risk preferences.

Contribution to portfolio risk The risk that an individual stock contributes to the risk of a portfolio depends on: -proportion invested in that stock, wi -its covariance with the portfolio, iM Therefore, Contribution to risk = wi iM Ratio of stock i’s contribution to the risk of portfolio: wi iM / 2M The ratio iM / 2M = beta coefficient

Capital Asset Pricing Model E(RM) - Rf = Risk premium on the market E(Ri) - Rf = Risk premium on stock i An investor can always obtain a risk premium BA(E(RM) - Rf) by combining M and the risk free asset. Thus: E(Ri) - Rf = Bi(E(RM) - Rf) or E(Ri) = Rf + Bi(E(RM) - Rf)

Security Market Line E(R) E(RM) Rf B BM=1