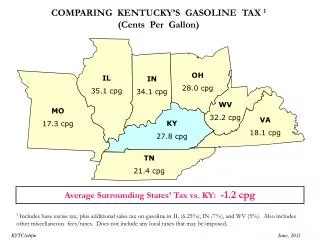

Section 34.1

Section 34.1. Chapter. Buying a Home. 34. Section 34.1 Evaluating Housing Alternatives Section 34.2 The Home Buying Process. What You’ll Learn. How to compare the advantages and disadvantages of buying a home (p. 730)

Section 34.1

E N D

Presentation Transcript

Chapter Buying a Home 34 Section 34.1 Evaluating Housing Alternatives Section 34.2 The Home Buying Process

What You’ll Learn • How to compare the advantages and disadvantages of buying a home (p. 730) • How to determine the amount of down payment you will need and the approximate amount you can borrow to buy a home (p. 730)

What You’ll Learn • How to describe various types of home ownership (p. 733)

Why It’s Important Being able to evaluate housing alternatives will help you to decide whether to purchase a home.

Legal Terms • mortgage (p. 730) • equity (p. 730) • debt ratio (p. 731) • cooperative (p. 735) • condominium (p. 735)

Section Outline Deciding to Buy a Home Advantages to Home Buying Disadvantages to Home Buying How Much Can You Afford?

Section Outline Types of Home Ownership Single- and Multifamily Homes Mobile Homes Cooperatives Condominiums

Pre-Learning Question What do you do before deciding to buy a home?

Deciding to Buy a Home Buying a home may be the most important purchase you will ever make.

Deciding to Buy a Home You will need to: • weigh the advantages and disadvantages • consider how much you can afford • determine the type of house will best fit your needs

Deciding to Buy a Home Most people take out a mortgage to help with the costs. A mortgage is a written instrument by which the buyer (the mortgagor) pledges real property to the lender (the mortgagee) as security for a loan.

Advantages to Home Buying There are several advantages to buying a home. One is the ability to do with it as you wish without having to answer to another owner.

Advantages to Home Buying Another advantage is the increase in equity, or the difference between the fair market value and the mortgage, in the property. Equity increases as you pay off the mortgage and as the property increases in value.

Advantages to Home Buying A third advantage is that you can deduct property taxes and interest paid on your mortgage from your income tax return.

Disadvantages to Home Buying There are some disadvantages. • the inconvenience and cost of upkeep • the inability to move easily and quickly if necessary

How Much Can You Afford? To determine how much you can afford to pay for a house, you must consider: • the amount of down payment • the amount you can borrow based on your income and expenses

Down Payment Down-payment requirements range from zero to 30 percent of the purchase price.

34.1 Down Payment Type of Loan Down Payment Veteran’s Administration (VA) loans (for qualified veterans to buy a house up to $203,000) 0 percent Mortgages backed by federal agencies, such as Fannie Mae and Freddy Mac 3 percent 3 to 5 percent FHA loans (loans insured by the Federal Housing Administration) 10 to 30 percent Conventional bank loans

Loan Qualifications A lender will judge your ability to repay your loan based on your credit report and your debt ratio, or the amount of your monthly payments compared to your monthly income.

Loan Qualifications Your mortgage payment, including taxes and insurance, should not exceed 28 percent of your monthly gross income.

Loan Qualifications Total monthly debt payments (including your new mortgage, credit cards, car payments, and so on) should not exceed 36 percent of your income.

The Elements of Buying a House It’s important to consider the following issues when making a home purchase. • location • down payment • mortgage rates and points

The Elements of Buying a House • closing costs • monthly payments • maintenance costs

Pre-Learning Question What are some different types of homes a person can own?

Types of Home Ownership You have many choices in selecting a home, depending on how much you can afford and the desired size of the house and its location.

Types of Home Ownership Different types include • single-family homes • multifamily homes • mobile homes • cooperatives • condominiums

Single- and Multifamily Homes • Single-family homes are the most popular type of home. • They offer privacy and more overall usable space than other types of housing.

Single- and Multifamily Homes • Multifamily dwellings are less expensive to own because of the income from nonowner-occupied units. • The owner’s monthly mortgage and tax payments can often come from rental income.

Mobile Homes • Mobile homes are also known as manufactured homes. • They are less expensive to purchase and to keep up. • They usually can be sold quickly and easily.

Cooperatives A cooperative (co-op) is a form of home ownership in which buyers purchase shares in the corporation that owns an apartment building and holds the mortgage on it.

Cooperatives Shareholders have a proprietary lease that gives them the right to the individual units.

Condominiums In a condominium (often called a condo), each owner has an absolute individual interest in an apartment unit and an undivided common interest in the common areas of the condo project.

Match the type of home with its description. • Multi-family home • Cooperative • Condominium • Mobile home

A situation in which each owner has an absolute individual interest in an apartment unit and an undivided common interest in the common areas.

A situation in which buyers purchase shares in the corporation that owns an apartment building and holds the mortgage on it.

Less expensive to own that a single-family home because of the income from nonowner-occupied units.

ANSWER • Multi-family home (d) • Cooperative (b) • Condominium (a) • Mobile home (c)

Section 34.1Assessment Reviewing What You Learned • What are the advantages and disadvantages of buying a home?

Section 34.1Assessment Reviewing What You Learned Answer Advantages—the ability to do with it as you wish; equity build up; ability to deduct property taxes and interest paid on your mortgage from your income tax return.

Section 34.1Assessment Reviewing What You Learned Answer Disadvantages—the inconvenience and cost of upkeep and the inability to move easily and quickly.

Section 34.1Assessment Reviewing What You Learned • Is it possible to buy a home with no down payment? Explain your answer.

Section 34.1Assessment Reviewing What You Learned Answer Yes. Qualified veterans can obtain a VA (Veteran’s Administration) loan to buy a house up to $203,000 with no down payment.

Section 34.1Assessment Reviewing What You Learned • Describe the five types of home ownership.

Section 34.1Assessment Reviewing What You Learned Answer (1) Single-family—offer the most privacy and usually have more usable space than other types of house. (2) Multi-family—are less expensive to own because of the income from nonowner-occupied units.

Section 34.1Assessment Reviewing What You Learned Answer (3) Mobile homes—also known as manufactured homes, are less expensive to purchase than ordinary houses and cost less to keep up. They can usually be sold quickly and easily.

Section 34.1Assessment Reviewing What You Learned Answer (4) Cooperatives—buyers purchase shares in the corporation that owns an apartment building and holds the mortgage on it.

Section 34.1Assessment Reviewing What You Learned Answer (5) Condominiums—each owner has an absolute individual interest in an apartment unit and an undivided common interest in the common areas of the condo project.

Section 34.1Assessment Critical Thinking Activity Lender Criteria If you were planning to borrow money to buy a home, why would your employment history be important to a lender?