Download

1 / 18

180 likes | 321 Views

INCOME TAXES ( How much will you keep?). GROSS PAY / DEDUCTIONS & NET PAY. Your paycheck (stub) contains vital information which needs to be reviewed and understood GROSS PAY = Total pay before deductions Net Pay = The amount of your paycheck after deductions (“Take-home Pay”)

E N D

GROSS PAY / DEDUCTIONS & NET PAY • Your paycheck (stub) contains vital information which needs to be reviewed and understood • GROSS PAY = Total pay before deductions • Net Pay =The amount of your paycheck after deductions (“Take-home Pay”) • Regular Wages or Salary + Overtime = Gross Pay • Gross Pay – Deductions = Net Pay • Direct Deposit

Hourly vs. Salaried Employees • Hourly Wages: • (Rate of pay) x (# of hours worked) • Overtime pay must be calculated at 1.5x rate of pay (Fair Labor Standards Act) – standard work week is 40 hours • Minimum wage in IL - $8.25 (subminimum wage) • Commission / Tips / Piecework • Salaried Employees: • Regular hours & a set amount of pay (usually stated as yearly salary & broken into equal increments) • Example - $36,000 annual salary – no overtime unless negotiated • Monthly Pay – ($36,000 / 12 = $3000 per month gross) • Bi-weekly – ($36,000 / 26 = $1384.62 every 2 weeks) • Bi-monthly – ($36,000 / 24 = $1500 twice a month) • Weekly – ($36,000 / 52 = $692.30 every week)

REQUIRED DeductionsAmounts subtracted from gross pay (Government) • Federal / State & Local Income Tax • Support multiple “public goods” & “programs” (roads / schools / defense / welfare / etc.) • The largest source of income for the Federal government is from Income taxes (43% of all revenue) • Social Security Tax (FICA) • Federal Insurance Contributions Act • Government supported retirement program • % of Gross Income • Employer matches • Medicare Tax • Government supported health insurance for retirees • % of Gross Income • Employer matches up to certain $ amount

OPTIONAL DeductionsAmounts subtracted from gross pay (Personal Option) • Health Insurance • PPO / HMO / etc. • Retirement Savings (401k / 403b / etc.) • Vested • Life Insurance • Union Dues • Employee Stock Options Plan • Savings Accounts • Various Others (parking / gym / etc.)

Employment Classifications Full-Time • Full access to benefits & better pay Part-Time • Fewer hours – benefits may or may not be offered Temporary • Short-term assignments (leaves / busy periods) • Employment agencies may provide benefits Contract • Specified time period for project completion • Usually no benefits unless stated in contract

Homework • Review Questions - Chapter 8 (pg. 206; 1-13) (Due Wednesday)

TYPES OF TAXES Progressive Taxes (Income Tax): • The more you earn – the higher amount of tax comes out of your pocket (Tax Brackets) Regressive Taxes (SALES TAX): • Smaller share of income is collected as income grows – SALES TAX is regressive – straight % for sales tax Proportional Taxes (PROPERTY TAX): • FLAT TAX – all members of a community pay the same amount regardless of earnings or value

FEDERAL INCOME TAXTHE UNITED STATES TAX SYSTEM • All U.S. citizens and businesses pay taxes to the government which the government uses for a variety of purposes – public education / police / fire / roads / etc.

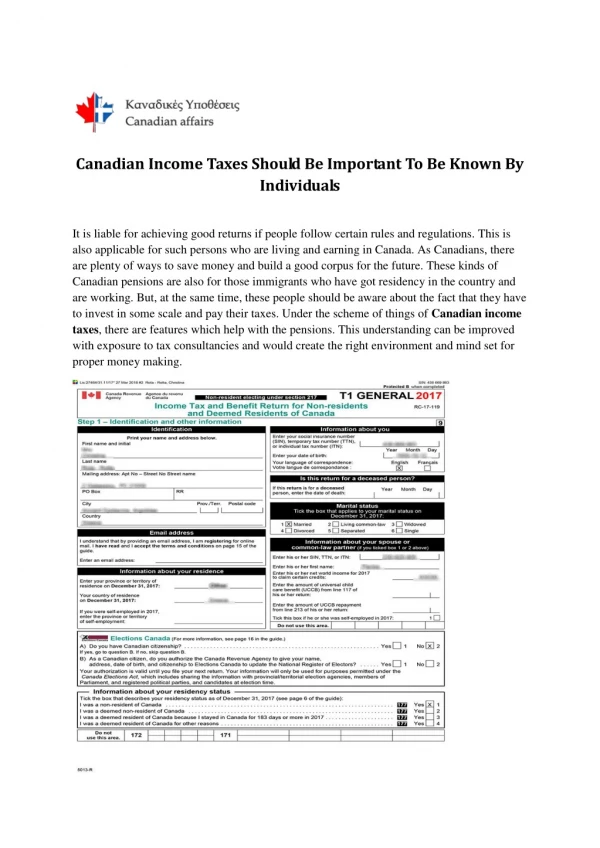

INCOME TAX – DOCUMENTS • Statement of Annual Earnings (Form W-2) • Sent by employer before January 31 • Employee Withholding Sheet (Form W-4) • This will let the employer know how much to take out of you pay for taxes (page 201) • If this form is completed incorrectly you may have too much or too little take out of your paycheck • Withholding too much • This will result in a tax REFUND after filing • Some people may use this to save money – no saving’s interest • Withholding too little • This will result in a tax liability – you will owe more $$ to IRS • Avoid this tax bill by: paying extra $$ / change your allowances

Progressive Taxes INCOME TAX • The ability-to-pay principle - individuals with higher income should pay a higher percentage of their income • Income tax is progressive – the more money earned the higher % is required to pay to the government • Approved and changed by Congress and the President • Collected by the Internal Revenue Service (IRS) • Based on Voluntary Compliance & people paying fair share • Determined by a tax return filled out by April 15 of each year based on the “Tax Formula” GROSS INCOME (Wages / interest / tips / etc.) -ADJUSTMENTS (Retirement plans / alimony / etc.) =ADJUSTED GROSS INCOME -ITEMIZED DEDUCTION or STANDARD DEDUCTION -EXEMPTIONS =TAXABLE INCOME ***Tax Tables will determine how much will be paid

TAX RETURNS • Returns should be completed with the idea of paying your fair share & taking advantage of all laws designed to give tax relief • Every American files a tax return before April 15th of each year to determine if they have paid the correct tax amount based on their total income • You may file online (www.irs.gov) – Turbo-tax Filing Status • Single (not married) • Married filing jointly • Married filing separately • Head of Household (providing a home for dependent people whether married of single & qualified)

WHICH TAX FORM? Form 1040EZ • Single or Married filing jointly • One Exemption for self & spouse if applicable • Income less than $50,000 on Line 6 of form • Income from wages, salaries, tips / Interest income of less than $1500 / Unemployment compensation / Taxable scholarship Form 1040A • Any filing status • All exemptions you qualify for • Income less than $50,000 on Line 25 • Income from same as above Form 1040 • Any filing status • All exemptions you are entitled to • Any amount of Income • All sources income are eligible

Taxable Income • Wages / salaries / tips • Interest income • Dividend income • Unemployment compensation • Social Security benefits (85% in some cases) • Alimony -- maintenance • “Other” income (businesses / royalties / estate income / trust income / pensions / gambling winnings / sale of personal items

Dependents / Exemptions • More dependents claimed the less tax paid (WHO?) • Person living with you receiving more than half his/her living expenses from you • Person must be a relative – child, stepchild, adopted child, etc. • Person must be a U.S. citizen of resident of the U.S. • The person may not file a return and claim himself or herself as an exemption • The person’s income may not exceed the amount of his or her exemption • After age 1 all dependents must have a social security number

Self-Employed Individuals • Required to claim income over $400 annually (Form 1040) • Many businesses must pay taxes quarterly depending on revenue • Schedule C (Profit or Loss Statement) is attached

Tax Planning • Understanding laws and guidelines for filing taxes is important to pay the correct amount each year • http://www.youtube.com/watch?v=IroCYzwWZtU