Download

1 / 58

600 likes | 998 Views

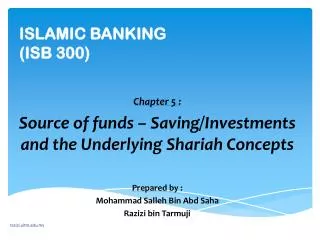

ISLAMIC BANKING (ISB 300). Chapter 5 : Source of funds – Saving/Investments and the Underlying Shariah Concepts Prepared by : Mohammad Salleh Bin Abd Saha Razizi bin Tarmuji. Content presentation. Sources of Funds Shareholder fund Depositors fund Current account Saving account

E N D

ISLAMIC BANKING(ISB 300) Chapter 5 : Source of funds – Saving/Investments and the Underlying Shariah Concepts Prepared by : Mohammad Salleh Bin AbdSaha Razizi bin Tarmuji razizi.uitm.edu.my

Content presentation razizi.uitm.edu.my Sources of Funds • Shareholder fund • Depositors fund • Current account • Saving account • General investment account • Specific investments account

Shareholders fund / equity razizi.uitm.edu.my • Contract used : Musyarakah (joint – venture profit sharing). • Through shares : • Ordinary Shares quoted @ unquoted • Special share (Minister of Finance)

Depositor fund razizi.uitm.edu.my

Pure profit – Sharing Model : razizi.uitm.edu.my • Model was the first to evolve • This model enjoys much support amongst most of islamic economists. • It assigns a significance role to profit sharing (mudarabah) on the both side of balance sheet, the asset and liability side. • Also know as the Two-Tier Mudarabah Model. • Concept based on two level of Mudarabah : • The first tier • The second tier

The first tier :- razizi.uitm.edu.my Between bank and depositor Put their money in the bank’s investment account and share profits with it. Depositors are considered to be provider of the capital (rabb al mal). The bank functions as a working patner or manager of funds (mudarib or amil).

The second tier :- razizi.uitm.edu.my Between the bank and the entrepreneurs. Seek finance from the bank on the condition that profits accruing from their business shall be shared between them and the bank in a mutually agreed propotion. But, the loss shall be borne only by the financier. Bank functions as the provider of capital. The entrepreneur is the manager of funds.

Two-tier contract of Mudarabah razizi.uitm.edu.my

Two Window Model razizi.uitm.edu.my The liability side of the bank’s activities is divided into 2 window : The bank is required to pay the funds held in the current account on demand, it is subjected to a 100% reserve requirement . The islamic precept – that funds of demand deposits are a trust (amanah) that is held by the bank on behalf of the depositors. The banks neither have a right to use these funds to make profit nor it should be used for the purpose of money creation through fractional reserve system.

Cont TWM… razizi.uitm.edu.my Funds held in the investment accounts shall not be subjected to any reserve requirement. It is argued by the economists who have advocated this model that investment accounts of islamic banks are not similar to time deposits of conventional banks, which are used for credit creation.

Profit Sharing – Cost Plus Model razizi.uitm.edu.my A profit sharing (mudarabah) on the liability side of the balance sheet and cost-plus technique of financing (murabahah) on the asset side. Other islamic ally permissible technique of finance such as mudarabah, musyarakah, ijarah, etc may also be used on the assets side.

Customers Deposits in Current Accounts razizi.uitm.edu.my Definition : An account into which customer can deposit money and effect payments by the drawing of cheques. The bank accepts its customer’s deposit and undertake to honor any demand (invariably in the form of cheque) made by customer, provided there is available funds in the account.

Currents Accounts based on Al-Wadiah razizi.uitm.edu.my Muamalat Contract : Al-WadiahYadDhamanah (a combination of al-wadiah (custody) and al-dhamanah (guarantee). A trust arrangement and involves the depositing (movable) or monetary deposits with another person, for safe-keeping. The depository acts as a trustee or guarantor, and guarantees repayment of the deposits on demand. Wadiah does not provide the depositors with the right to receive a share of the profits.

The pillars of Al – Wadiah Contract razizi.uitm.edu.my • Al – Muwaddi’ • Depositor, Owner of the property • Al – Wadi’ • Depositee, Custodian of the property • Al-Wadi'ah • Property for safe keeping • Sighah • Offer (Ijab) • Acceptance (Qabul)

Condition of Al - Wadiah razizi.uitm.edu.my

Type of wadiah razizi.uitm.edu.my • Wadi’ahYadd al-Amanah • Safe custody based on trust • Wadi’ahYadd al-Dhamanah • Guaranteed safe custody

WadiahYadAmanah razizi.uitm.edu.my • Generally, wadi’ah is based on amanah (trust) • It is charitable and divinely rewarded. • Important features of wadi’ahyadd al-amanah: • The custodian should keep the deposits as if he is keeping and taking care of his own property. • The custodian should not responsible for any damage of the property so far it has not resulted from his negligence • The custodian is not entitled to any profits gained from the contract. Any benefits accrued from the deposit belong to the owner. • The custodian should not utilize or take benefit of the deposit. • The custodian should not transfer the deposit in the hands of others without permission of the depositor. • The custodian should not take the deposit in journey unless permission is given. • The custodian should return the deposit back to the owner upon request.

WadiahYaddDamanah razizi.uitm.edu.my • This type of Wadi'ah is a combination of safekeeping (Wadi'ah) and guarantee (dhaman). • The Wadi'ah is based on guarantee whereby the custodian guarantees the refund of the property kept with him and ensures to refund the item upon request. • This type of wadia’ah facilitates wider application in the Islamic banking system. • Important features of wadi’ahyadd al-dhamanah: • The custodian is entitled to use the deposited property for trading or any purposes. • The custodian has a right to any income derived from the utilization of the deposited item and liable for any damages or loss • The custodian owns the profit and under his discretion to give some portion of it as a gift (hibah) to the depositor. The gift cannot be in the form of a pre-agreed agreement. • The custodian must return the deposited property to the owner at any time upon the request of the depositor.

AL-WADI'AH: ACT OF TRUST BECOME ACT OF GUARANTEE razizi.uitm.edu.my • Besides the cases of ignorance, contract of Wadi'ah could be transformed from trust (amanah) into guarantee (dhamanah) in the following cases if the depositee: • Ignores the protection and safe keeping of the deposited property • Deposits the property with somebody else, or not somebody who normally takes care of the depositee’s property. • Benefits from the usage of the deposited property • Travels with the deposited property. • Refuses to return the deposited property to the depositor or withholds it even though he/she is capable of returning it. • Mixes the deposited property with other properties, which could not be recognized and distinguished from each other. • Commits certain conducts which are against the predetermined condition of the depositor.

Customer’s deposits in Current Accounts (al-wadiahyaddhamanah) razizi.uitm.edu.my Islamic banks mobilises its customer’ deposits in current accounts on the contract of al-wadiahyaddhamanah (guaranteed custody)

Details or modes of operation razizi.uitm.edu.my

Cont…. Current Accounts razizi.uitm.edu.my Basic Features and the Nature of Agreement between Banks and their Customers that forms the basis of Current Account : • The banks accepts deposits from its customers looking for safe custody of their funds and absolute convenience in their use in the form of current accounts on the principle of al-wadiahyaddhamanah. • The banks requests permission from such customers to make use their funds so long as these funds remain with the bank. • The customer may withdraw a part or the whole of their balances at any time they so desire, and the bank guarantee the refund of such balances.

Cont…. Current Accounts razizi.uitm.edu.my All the profits generated by the bank from use of such funds belongs to the bank. The bank may, at their absolute discretion give reward to accounts maintained by Federal and State. Government and Statutory Authorities provided they maintain a minimum daily balance of not less than RM 25,000. The bank provides its customers with cheque books and other usual services connected with current accounts. Any losses generated from the investment will be borne by the bank.

Characteristics and Salient Features razizi.uitm.edu.my Current accounts mostly govern what is commonly known as call deposits or demand deposits. These accounts are opened by both individuals and business companies. These accounts may be opened in local or foreign currency if the bank is allowed to operate in the foreign exchange market. The banks guarantees full return of these deposits on demand and the depositors are not paid any share of profit or a return in any form.

Cont…. Characteristics and Salient Features razizi.uitm.edu.my The depositors are not subjected to any conditions regarding to deposits or withdrawals. Any amount may be deposited into account any time and may be withdrawn any time. Some banks may insist to maintain a minimum balance in the account to keep it operational. The banks usually provide checks writing facility to account holders.

Dominant Expressions of the Idea of Loans that Underline Current Accounts in the Islamic Banks : razizi.uitm.edu.my • To treat demand deposits as an Amanah (Trust) / Wadiah : • Among islamic banks which apply the principle of wadiah are banks in Bangladesh, jordan and Malaysia. • In Malaysia, however instead of wadiah, the principle is called wadiahyaddhamanah or guarantees custody.

Cont…. Current Accounts razizi.uitm.edu.my • To treat demand deposits as Qardh Hassan (an interest free loan) : • Among islamic banks which apply the principle of qardhhassan are banks in Iran, Dubai islamic bank of the United arab Emirates and the Kuwait Finance House of Kuwait.

Differences between wadiah account from conventional savings account razizi.uitm.edu.my

Current Accounts Based on Al-Mudharabah razizi.uitm.edu.my Definiton of al – Mudharabah : • Literally : Profit or increase • Technically : can be defining as a joint-venture profit sharing contract whereby one party is the provider of capital while the other is the entrepreneur (Ahmad,2006)

Characteristics of Mudharabah razizi.uitm.edu.my The profit will be shared between parties whom involved in the contract according to the terms of their agreement. The losses will be borne by the capital provider who is the financier of the project. The entrepreneur suffers of their fruitless effort.

Categories of Mudharabah razizi.uitm.edu.my

Al-Mudharabah Al-Mutlaqah(unrestricted mandate) razizi.uitm.edu.my Under unrestricted investment fund, entrepreneur (bank) has got the authority by the capital provider (depositor) to invest the funds in any manner which they think appropriate. Entrepreneur (bank) is free to invest on how, where and for what purposes the funds should be invested. They (depositor) will be no restriction to entrepreneur.

Al-Mudharabah Al-Muqayyadah(restricted mandate) razizi.uitm.edu.my The entrepreneur is restricted in his activity in carrying out the mudaharabah project in term of business, method, time period or place.

Pillars of Mudharabah razizi.uitm.edu.my Sahibul Mal : owner of capital, fund provider Mudharib : entrepreneur Ra’sul Mal : capital Al-Amar or Mashru’ : business ventures or project Ribh : predetermined share of profit Sighah : offer and acceptance

Condition for pillars of mudharabah razizi.uitm.edu.my Owner of capital Entrepreneur Capital Project Profit or loss Contract (offer and acceptance) Sighah (ijab and qabul)

Termination of Mudharabah razizi.uitm.edu.my The contract dissolved : • With the completion of the venture • Or the expiry of the specific time period • Or the death of either rab-al-mal or the mudharib • Or the serving of notice by either of the two partners of his intention to dissolve the mudharabah.

Al-mudharabah in Current Account razizi.uitm.edu.my • Contract made between : • Depositor (provider of capital) ---------- Bank (entrepreneur) • The amount deposited for a stipulated period by the depositor will be used by the bank for investment purposes according to the al-mudharabah principle. • The bank becomes wholly responsible and liable in the management and investment the deposits in halal business ventures. • Profits gained will be divided and distributed accordingly, based on margins agreed upon earlier.

Customers deposits in Saving Account razizi.uitm.edu.my Muamalat contract : Al – WadiahYadDhamanah • Mobilizes customers’ deposits under the cintract of al-wadiahyaddhamanah its modification on the payment of profit at the absolute discretion of the bank. • This is a trust arrangement and involves the depositing (movable) or monetary deposits with another person, for safe-keeping. • The depository acts as a trustee or guarantor, and guarantees repayment of the deposits on demand. • Wadiah does not provide the depositors with the right to receive a share of the profit.

Details or modes of operation razizi.uitm.edu.my

Basic Features And Nature Of Agreement razizi.uitm.edu.my The bank accepts deposits from its customers looking for save custody of their funds and a degree of convenience in their use together with the posibility of some profits in the form of savings accounts on the principle Al-WadiahYadDhamanah. Al-WadiahYadDhamanah is a trust arrangement and involves the depositings of goods (movable) or monetory deposits with another person, for safe-keeping. As this is trust, the depositary acts as a trustee or guarantor, and guarantees repayment or the deposits on demand. Wadiah does not provide the depositor with the right to receive a share of the profits.

razizi.uitm.edu.my The bank request permission from such customers to make use of their funds so long as these funds remain with the bank. The customers may withdraw a part or the whole of their balances at any time they so desire, and the bank guarantees the refund of such balances. All the profits generated by the bank from the use of such funds belong the bank. However, in contrast with current accounts, the bank may at its absolute discretion rewards the customers by returning a portion of the profits generated from the use of their funds from time to time. The bank provides its customers with savings passbook and other usual services connected with savings accounts. The bank also provides the ATM services for these accounts.

Salient Features/ Characteristics razizi.uitm.edu.my A savings account is a type of deposit account. It characterized by a passbook. Savings account are primarily intended for small savers. These savers formed a stable deposit base for the bank. The 3 shariah principles used by islamic banks for savings account are: Qard Hassan (used by banks in Iran), Wadiah (used by bank in Malaysia, Kuwait Finance House of Kuwait and Faisal Islamic Bank of Bahrain) and Mudharabah (used by Dubai Islamic Bank and Islami Bank Bangladesh).

razizi.uitm.edu.my The banks accepts deposits from its customers looking for safe custody of their funds and a degree of convenience in their use together with the posibility of some profits in the form of savings accounts on the principle of al-WadiahYadDhamanah.

Discretionary Rewards of Saving Account: razizi.uitm.edu.my Under the principle of al-Wadiah, the bank is not obligated in any way to give returns on depositors. However, the banks at its absolute discretion, may reward its customer a certain amount of return as deemed fit. Calculation of profit is a follows: Cumulative daily balance for the month x Rate x 1/12 No. of days in the month

Customers deposits in General Investment Account razizi.uitm.edu.my Muamalat Contract: al-Mudharabah (trustee profit- sharing). This account open to all its customers. The bank acts as ‘entrepreneur’ and the customers as the ‘ provider of capital’. Both agree on show to distribute profits (if any) and in the event of loss, the customer bears all the loss.

Details or modes of operation razizi.uitm.edu.my

Characteristics of an Islamic General Investment Accounts razizi.uitm.edu.my The banks accepts deposits from its customers looking for investment accounts on the principle of al-Mudharabah. The deposit will have to be for a specified period. In basic Syariah relationship, the banks acts in the case as the entrepreneur and the customers as the will provider of capital and both will agree among others on how to distribute the profits if any, generated by the bank from the investments of the funds.