Download

1 / 10

100 likes | 204 Views

The Housing Meltdown, Subprime Mortgages And Securitization. Robert Van Order University of Aberdeen and University of Michigan. Subprime Loans. Some ambiguity, but mostly it’s borrowers with bad credit history—Loans are higher cost Now by “FICO” score and related credit history

E N D

The Housing Meltdown, Subprime Mortgages And Securitization Robert Van Order University of Aberdeen and University of Michigan Chapter 23

Subprime Loans Some ambiguity, but mostly it’s borrowers with bad credit history—Loans are higher cost Now by “FICO” score and related credit history But other things like documentation and down payment matter. Alt-A: High enough FICO but low documentation Quantifying credit history was a big deal in securitizing high risk loans. Chapter 23

Subprime Share Should we be surprised in a market expanding that fast that quality deteriorated? Chapter 23

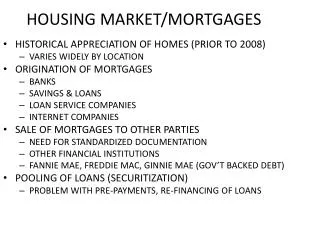

– Recession Subprime ARM Defaults Are Very Different from Prime and Subprime FRM: Why are they worse? Loans 90 days or more delinquent or in foreclosure (percent of number) Subprime ARM Subprime FRM FHA & VA Prime Conventional Chapter 23 Source: Mortgage Bankers Association (Quarterly data not seasonally adjusted;1998Q1-2007Q3)

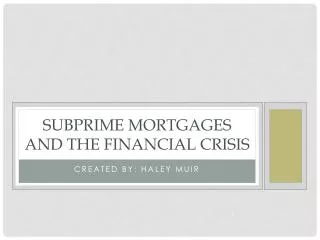

Subprime Performance Has Worsened by Origination Year Cumulative REO as a Percentage of Original Balance 2003 2006 2005 2004 Age in Months Source: Loan Performance, a subsidiary of First American Real Estate Solutions Note: the last twelve points on each origination year cohort contain fewer loans progressively as loans issued at earlier dates always age faster. Chapter 23

Subprime Underwriting: On the surface the loans look like they haven’t changed much. Source: LoanPerformance TrueStandings Securities. Data through June 2007. First Liens Only; by dollar amount. Chapter 23

Relative Default ProbabilitiesNote the “Nonlinearity” as you move NortheastMistakes investment more risky there, more sensitive to mistakes. Chapter 23

SECURITIZATIONAgency Costs and Senior/Subordinated Structures Serous asymmetries of information make it hard on investors Senior/Sub structures are the most popular way of managing this. They allow most of the credit risk to remain with the originator and/or specialists and get institutional investors interested in the senior part. In Principle this is a good way of dealing with agency problems (moral hazard, asymmetric information. The trick is to prioritize the cash flows so that there is a queue and originators or specialists take the bulk of the credit risk’ This means that a pool of B type securities can have most of it funded with AAA paper. That there were AAA pieces is consistent with the loans in the pool being junk bonds. The “Cheapest to Deliver” problem. How much subordination is enough?

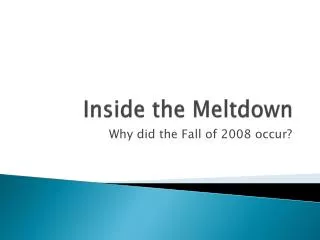

A TYPICAL STRUCTURE: What happens to the loans Loan 1 Loan 2 Loan 3 Loan 4 $1 Billion Total Loans ….. Trust (SPV) $850m AAA Rated $1 Billion Subprime Structured Deal $100m, BB Rated, $50m, NR, Chapter 23 9

Jumbo Rates Have Gone Way Relative to Other RatesThis is why the stimulus package has FF expansion. Think California <> Chapter 23