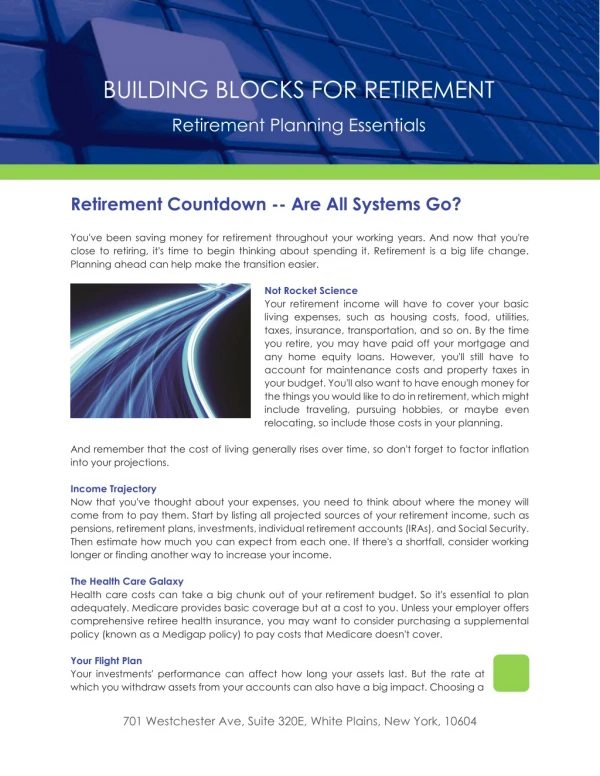

Download

1 / 26

260 likes | 344 Views

US Retirement Systems Project. 21 October 1998. Ben Fischer, Faculty Advisor. Introduction. Welcome Group Member Introduction Panel Member Introduction Project Description Discussion of Actuarial Assumptions Discussion of Pensions Where Do We Go From Here?. Jim Archbold

E N D

US Retirement Systems Project 21 October 1998 Ben Fischer, Faculty Advisor

Introduction • Welcome • Group Member Introduction • Panel Member Introduction • Project Description • Discussion of Actuarial Assumptions • Discussion of Pensions • Where Do We Go From Here?

Jim Archbold Carnegie Mellon University, Biology Group Project Manager Rebecca Bosch University of Michigan, Psychology Glenn Dubin University of Miami, Broadcasting/ Political Science Yuan Gao Shanghai University, Accounting Melissa Gongaware Carnegie Mellon University, Psychology Serge King Howard University, Political Science Zhenqqing Li Nankai University, Business Administration/Economics Matthew Maletestinic Carnegie Mellon University, Industrial Management María De León University of Wisconsin-Madison, Literature Group Members

Panel Members • Please introduce your: • Name and Organization

Project Description • U.S. Retirement System • Data Gathering • Actuarial Reports • Assumptions • Pensions • Policy Proposals

Economic Assumptions of the OASDI • Annual Interest Rate • Gross Domestic Product (GDP) • Consumer Price Index (CPI) • Average Wage • Real Wage Differential • Level of Unemployment • Labor Force Participation

Interest Rate • Average Annual Interest Rate • Each Annual Report Makes Projections 75 years into the future • There is variation between the predicted rate and the actual rate. • Should Americans panic and make “rash” policy changes based on these predictions. Economic Assumptions

Interest Rate Assumptions Economic Assumptions

Gross Domestic Product • The GDP is the sum of all goods and services produced in the United States, by both foreign and domestic organizations • The GDP is a tremendous measure of economic strength Economic Assumptions

GDP Assumption Economic Assumptions

CPI and Real Wage Differential • The CPI is the “bundle” of goods that has come to be used as an indicator of inflation • The average real wage is the average wage of all earnings taxable for social security purposes for all covered workers indexed for inflation • Real Wage - CPI = Real Wage Differential • The Real Wage Differential is indicative of the standard of living Economic Assumptions

CPI and Real Wage Differential • The CPI is important as an index of inflation and represents the cost of living • As the CPI (and inflation) rises, the real wage differential is negative. As the CPI is steady or decreases, the real wage differential is positive • When the real wages are higher than the CPI, net income to the trust fund increases Economic Assumptions

Unemployment rate Unemployed Persons Retired Employees The unemployment rate represents the proportion of the civilian labor force that is unemployed. All persons who had no employment during the reference week, were available for work, except for temporary illness, and had made specific efforts to find employment sometime during the 4-week period ending with the reference week At work part time for non-economic reasons due to retirement or Social Security limits on earnings Average Annual Unemployment Rate Economic Assumptions

Average Annual Unemployment Rate Economic Assumptions

Average Annual Percentage Increase in LFP Note: Labor force is the total for the United States (including military personnel) and reflects the average of the monthly numbers of persons in the labor force each year Economic Assumptions

In 1993, the Labor Force Participation Rate was off by 1.5% (ages 60-64) Economic Assumptions

In 1985, Labor Force Participation was off by 1.5% (ages 60-64) Economic Assumptions

In 1995, the actual labor force participation was much higher than anticipated. Economic Assumptions

Pensions: Private and Public • ERISA • Defined Benefit v. Defined Contribution • Level of Savings-Private • Level of Savings-Public

Private Pension Plans • Private pensions currently cover less than half of the American workforce • Contributions to private plans have been declining for a number of years • In 1989, plan terminations increased 37% and new plan creations decreased 67% • In 1994, there was a decrease in private pension plan contributions of approximately $2 million from 1993 • The main reason for this trend is the complexity of pension regulations • Tax Reform Act of 1986 • Pension qualification rules enacted in 1989 Sources: Kelley, Christopher T., UNCERTAINTY IN THE GOLDEN YEARS: THE GROWING DEMANDS UPON THE AMERICAN RETIREMENT SECURITY SYSTEM, 2 Elder L.J. 225; Private Pension Plan Bulletin, Abstract of 1994 Form 5500 Annual Reports, U.S. Dept. of Labor.

Employment Retirement Income Security Act (ERISA) • ERISA governs the creation and maintenance of employer-provided pensions • A qualified ERISA plan is entitled to preferential tax treatment • Benefits • - Employees are allowed to defer taxation of a portion of their income • - Interest accrued on the funds is tax-deferred until withdrawal or retirement • - The employer avoids payroll taxes on the amounts contributed • Shortcomings • - Not available to everyone • - Many Americans overestimate how much their pension plans will provide Sources: 29 U.S.C. §§ 1001-1461 (1988) and 26 U.S.C. § 401(a) (1988). “Merrill Lynch Survey Finds Baby Boomers Not Saving for Retirement”, BNA PENSIONS & BENEFITS DAILY, July 11, 1991.

Public Pension Funds • Federal Regulations • State Regulations • - Tax sanctions are not an effective means of regulation • - Federal tax regulations harm the plan participant rather than the sponsor • Public pension fund trustees must: • - Act with strict fiduciary loyalty to participants and beneficiaries • - Administer the funds prudently • Conflicts of interest arise in: • - Personal interest in a transaction involving fund assets • - Divergent interests of the various beneficiaries • - Duty of the Trustee to the beneficiaries and to other interests Source: Paisley, Kathleen. “PUBLIC PENSION FUNDS”, 4 Yale Law & Policy Review 188.

Private v. Public Pensions • Public Sector employees are more likely to receive defined benefit pension plans than are their private sector counterparts. • Private Sector employees are more likely to receive Social Security. • Defined contribution plans are becoming increasingly prevalent among private sector employees. • Beyond coverage, defined benefit pension plan provisions differ widely between public and private sector employees, making comparisons difficult. Source: Wiatrowski, William J. “On the Disparity Between Private and Public Pensions.” Monthly Labor Review. April, 1994. P8.

Summary • Is Social Security broken? • Are the assumptions reliable enough to base major policy changes upon them? • Improving upon the US Retirement System (ie. Social Security, Pensions, Medicare, Private Savings) can be done “rationally”, without the panic that current projections create.

Sampling of Policy Alternatives • Raise earnings cap for Social Security recipients • Raise the level of taxable earnings • Raise the age limit for people to receive Social Security benefits • Invest trust fund surplus in stocks/bonds/funds • Create private investment accounts for Social Security recipients • Give incentives to employers to keep older workers employed • Eliminate benefits for those with more than a certain amount of income regardless of age • Bolster private and public pension funds with trust fund surplus or with entire trust fund

Questions and Answers • Our three identified areas of future analysis: • Labor Force Participation • Private & Public Pensions • Policy Alternatives • Where does your expertise fit into our areas of future analysis?