Download

1 / 7

70 likes | 137 Views

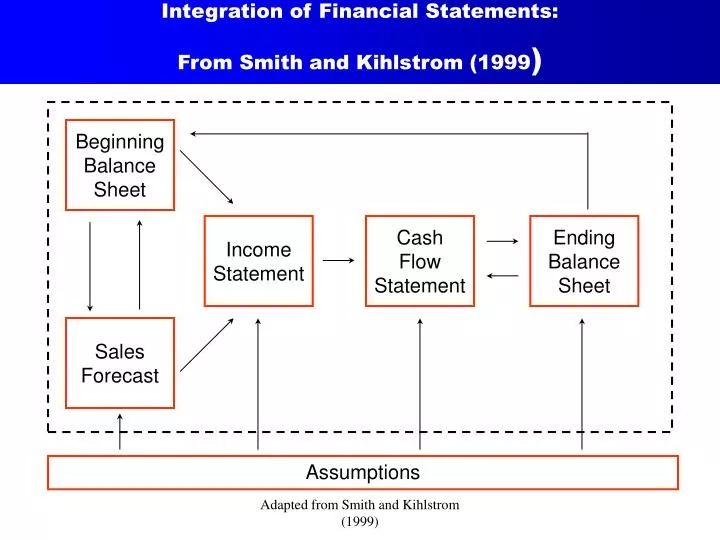

Integration of Financial Statements: From Smith and Kihlstrom (1999 ). Beginning Balance Sheet. Income Statement. Cash Flow Statement. Ending Balance Sheet. Sales Forecast. Assumptions. Four key questions to be answered in a sales forecast.

E N D

Integration of Financial Statements: From Smith and Kihlstrom (1999) Beginning Balance Sheet Income Statement Cash Flow Statement Ending Balance Sheet Sales Forecast Assumptions Adapted from Smith and Kihlstrom (1999)

Four key questions to be answered in a sales forecast • 1) When will the venture begin to generate revenues? • 2) Once revenues are being generated, how rapidly will they grow? • 3) Over what span of time (3 years, 5 years, 10 years, etc.) should • the forecast be made? • 4) What is an appropriate forecasting interval (weekly, monthly, annually, etc.)?

General rules of financial forecasting Part 1 • Build and support a schedule of assumptions • Begin with a forecast of sales • If the sales growth is expected to track inflation, consider forecasting • sales in real terms • When using historical data to forecast, consider a weighting scheme • which focuses on the firm’s most recent experiences • For new ventures, choose several “yardstick” firms and compare to aid in • developing underlying assumptions regarding expected performance • Integrate the pro forma balance sheet and income statement variables • through formulas

General rules of financial forecasting Part 2 • Consider time span. To assess financial need, project until the firm • expects follow up financing. To determine venture value, extrapolate • to the point of harvest • Determine the planning horizon of the venture to establish • forecasting intervals • Test the model’s rationality by tracing line items across financial statements • Apply sample scenarios and compare outcomes to estimations • Try a basic sensitivity analysis to ensure the model yields reasonable • results when magnitudes and growth rates of key variables change

New company assumptions Part I • 1) Development will require 18 months, during which no sales will be made • 2) Initial sales of $10,000 in the 19th month • 3) Sales will grow 8% per month in real terms for three years and at the inflation rate • thereafter • 4) Cash operating expenses during the development period of $15,000 per month, • plus inflation • 5) Inflation at 3 percent per year • 6) A $200,000 production facility will come on line at the end of month 18. The • facility is to be leased by the company for the first 5 years of operations with • monthly payments of $3,000 • 7) Gross profit of 60% of sales revenue on materials costs with trade discounts • 8) Selling expenses of 15% of sales. • 9) Administrative expenses of $2,000 per month beginning in month 19, growing at the • inflation rate, plus 15 percent of sales (Included in development period operating • expense total)

New company assumptions Part II • 10) Entrepreneur’s salary of $3,000 per month through the first full year of sales • (included in initial operating expenses), increasing thereafter by $500 per month • 11) Corporate tax rate of 45%. No loss carry forward • 12) All sales are for credit. The average collection period is 45 days. No discount • for prompt payment • 13) The inventory turnover rate is 5 times per year, measured against ending inventory • 14) The company desires to maintain the greater of 30 days’ sales in cash or $10,000 • 15) All materials are purchased on credit, with terms of 2/10 net 30. The company • anticipates paying in time to receive the discount. The payables period is 10 days • 16) The entrepreneur will borrow any funds necessary at a rate of 1% per month • 17) Initial investment by the entrepreneur of $200,000. Additional financing by • borrowing on a line of credit

New company sales forecast • (Forecast generated monthly, selected months shown)