Download

1 / 20

200 likes | 312 Views

Review of Virginia Market Conditions and Foreclosure Trends. What’s Ahead for Housing? A Symposium on Federal Housing Policy Change June 14, 2013. W here we are in the market recovery. H ome sales continue to rise. April/May sales were strong following a slowing in the 1 st Qtr.

E N D

Review of VirginiaMarket Conditions and Foreclosure Trends What’s Ahead for Housing? A Symposium on Federal Housing Policy Change June 14, 2013

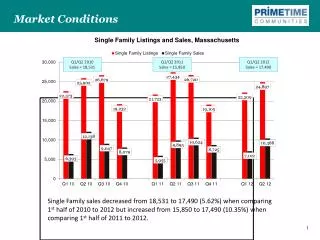

Home sales continue to rise. April/May sales were strong following a slowing in the 1st Qtr. Source: Virginia Association of Realtors (VAR)

The increase in home sales has been somewhat stronger downstate than in the Northern Tier. Source: Virginia Association of Realtors (VAR)

Nonetheless, NoVA’s extremely tight inventoryis pushing up prices more than in other regions. Source: Federal Housing Finance Agency (FHFA)

Rising prices are alleviating negative equity,but it remains aconstraint on for-sale inventories. Source: CoreLogic, a real estate data and analytics company

Investor sales remain high in the Northern Tier,but are much lower than elsewhere in the nation. Sources: MRIS (regional data), National Association of Realtors (U.S. data)

Tight inventory and difficulty in accessing creditare keepingfirst-time buyers on the sidelines. Source: National Association of Realtors (NAR)

New problem loans rates are declining, but are only half-way back to their long-term average. Source: Mortgage Bankers Association (MBA)

Likewise, long-term serious delinquency rates are only half way to their long-term average. Source: Mortgage Bankers Association (MBA)

The decline in serious delinquencies continuestoclosely track improvement in unemployment. Sources: Mortgage Bankers Association (MBA) and Virginia Employment Commission (VEC)

Subprime and ARM loans make up most of the 45% drop in foreclosures from the 2009 peak. Source: Mortgage Bankers Association (MBA)

Nonetheless, subprime and ARM loansremain a disproportionate share of foreclosures. Source: Mortgage Bankers Association (MBA)

The Northern Tier’s improved loan performance in not yet being seen in downstate markets. Source: Federal Reserve Bank of Richmond/Lender Processing Services (LPS) Applied Analytics

Northern VA’s number and share of problem loans has fallen, while Hampton Roads’ has risen. Source: Federal Reserve Bank of Richmond/Lender Processing Services (LPS) Applied Analytics

Distressed sales in Hampton Roads remain high, and continue to constrain increases in prices. Sources: National Association of Realtors (U.S. data), Tom Lawler, Economist, Calculated Risk Blog /MRIS (regional data)

Short sales are playing a bigger role inGreater Washington than they are nationwide. Source: National Association of Realtors (U.S. data), Tom Lawler, Economist, Calculated Risk Blog /MRIS (regional data)

Conclusions • Price rises are being driven by abnormal factors: • Low mortgage rates: Ongoing Federal Reserve bond purchases are keeping rates at historic lows. • Constrained inventories: Negative equity and fewer distressed sales are constraining listings of existing homes. • Despite market recovery, key undertows remain: • Lagging Fundamentals: Traditional housing and lending fundamentals — income, employment and household debt — continue to be weak. • Reluctant Buyers: Increases in traditional buyers, as well as sellers, are needed to support a sustained recovery.

Conclusions • The housing recovery still relies on federal stimulus. • Low mortgage rates remain critical to the restoration of positive owner equity and the mitigation of troubled loans. • However, the Federal Reserve cannot maintain current levels of mortgage bond purchases indefinitely. • The recovery will remain fragile until higher home prices can be sustained by economic fundamentals — i.e., rising incomes and more normal sales volumes and mortgage interest rates.