Download

1 / 6

0 likes | 1 Views

Youu2019ve been house-hunting in Toronto neighbourhoods like Leslieville, The Annex, or Scarborough, you found a place you absolutely loveu2014and then, boom: your mortgage pre-approval in Canada comes back denied.

E N D

What to Do if Your Mortgage Pre-Approval Gets Denied You’ve been house-hunting in Toronto neighbourhoods like Leslieville, The Annex, or Scarborough, you found a place you absolutely love—and then, boom: your mortgage pre-approval in Canada comes back denied. It’s disheartening. You might feel like you hit a wall. But trust me: this isn’t the end of your home-buying journey. With the right plan and support, you can come back stronger. And with Think Homewise by your side, you don’t have to go at it alone. Why Did My Pre-Approval Get Denied? Before moving forward, let’s understandwhylenders sometimes say “no.” In Toronto’s high-cost housing market, lenders are extra cautious. Some common reasons include: Credit issues: Low credit score, past delinquencies, or unresolved collections. High debt-to-income (DTI) ratio: If your monthly debts (credit cards, auto loans, etc.) plus the proposed mortgage amount exceed what lenders are comfortable with. Unsteady income or employment history: Perhaps you've recently changed jobs, or your income comes from contract work or side gigs that don’t show up consistently.

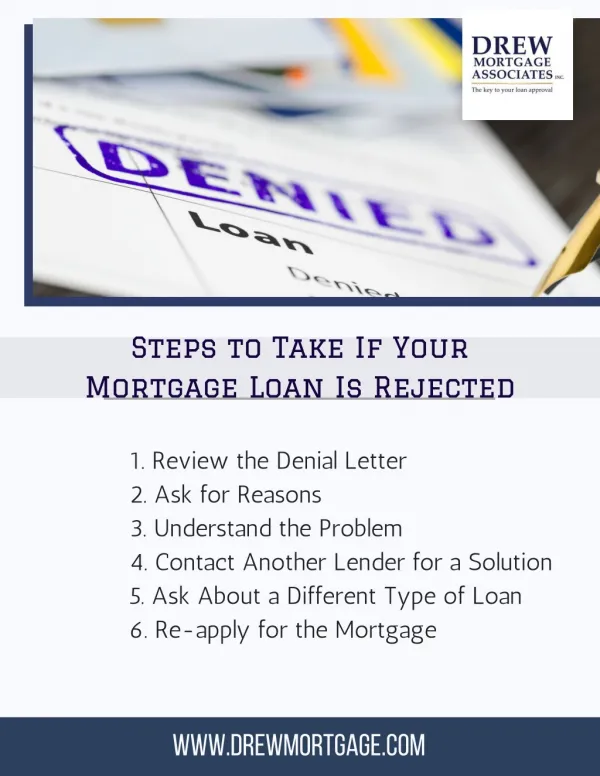

Incomplete or incorrect documentation: Missing pay stubs, not enough proof of residence, or errors in the application. Recent large financial changes: Big purchases, new lines of credit, or high credit utilization. Sometimes the denial letter from the lender will clearly state the reason; other times, it may be a mix of several small concerns. The good news? These are fixable. Step 1: Read the Denial Letter Closely When you receive that denial, don’t just put it aside and forget about it. Read it carefully. The lender will usually cite what concerns they had. That’s your roadmap for what to improve. Maybe it’s “credit score below XYZ,” or “DTI too high.” Maybe they couldn’t verify some income. With Think Homewise, you can also ask your Homewise Advisor to go through the letter with you, help you decode the jargon, and figure out exactly what to fix. Reach out to hello@thinkhomewise.com or give them a call at 1 (866) 846-9473—they’re ready to help you map a clear path forward. If you want a fresh chance at getting pre-approved, apply online now with Think Homewise and let them help you find out what needs adjusting. Step 2: Strengthen Your Credit Profile Your credit score is often the hill you’ll climb first. In Toronto and across Ontario, lenders look to Equifax or TransUnion history, and they check your score, credit usage, and payment history. To build your credit: Pay down or eliminate any high credit-card balances. Don’t open multiple new credit lines right before reapplying. Make sure all past payments are on time. If something’s off, contact the creditor and see if a settlement or payment plan is possible. Pull your credit reports and double-check for errors (maybe an old collection that shouldn't be there). Dispute any inaccuracies. Using Think Homewise, you can tap into resources that help you understand what’s affecting your credit, together with your personal advisor, who can suggest concrete steps. Want credit-improvement tips tailored to your situation? Talk with a Homewise advisor today.

Step 3: Lower Your Debt-to-Income Ratio In Toronto, with high rents, commute costs, and everything else, keeping your DTI reasonable can be tricky. But lowering your DTI can make a big difference: Try to pay off smaller debts (credit cards, small loans) first. Avoid taking on new debt (financing furniture, a car, etc.) until after you’re pre-approved. If possible, increase your gross income—maybe through side work, bonuses, or overtime— and make sure to document it well. Having a steady income helps. Think Homewise works with 30+ banks and lenders, which means they see different lender thresholds; sometimes, a small improvement in DTI (e.g., paying down one credit card) will move you into a bracket where more lenders might say yes. Compare your options with Think Homewise — apply now and see where you stand across lenders. Step 4: Stabilize Employment & Income Sources Lenders want to see stability. If you’ve switched jobs recently or if your income fluctuates wildly, that may trigger a denial. Here’s what you can do: Stay in a role for at least a year, if possible. If changing jobs, choose ones similar in field or pay, rather than ones with huge income swings. If you have variable income (commissions, freelance, etc.), be sure to keep good records— tax returns, client contracts, etc. Avoid big gaps in employment, or if you have them, be ready to explain them with documents. Think Homewise’s advisors can help you package that income documentation so lenders see the full picture. Getting ready to reapply? Let Homewise help you organize your employment records and figure out which lenders in Toronto will view your income most favourably. Step 5: Boost Your Down Payment & Reduce Other Financial Risks If your down payment is small (or partly borrowed, or unverified), it worries lenders. In a city like Toronto, where house costs are steep, showing you have a solid down payment can make a

significant difference. Also, showing lower ongoing costs (property taxes, condo fees, utilities) helps reduce your risk profile in the eyes of lenders. If possible, save more; maybe dial back on some discretionary spending. Explore assistance programs (especially for first-time homebuyers in Ontario). Use gifts from family if applicable, but document them properly. Think Homewise can help you calculate how much extra down payment might reduce your monthly payment, and they’ll match you with lenders who value stronger down payments. Want to see how increasing your down payment changes your mortgage options? Reach out to Think Homewise now. Step 6: Explore Different Loan Types & Alternative Lenders If your profile doesn’t yet meet the stricter banks’ thresholds, there are other avenues: Government-insured mortgages (like CMHC) or other programs for first-time buyers. Alternative lenders or private lenders (though interest rates may be higher). Co-signers or joint applicants, if feasible. Short-term or variable rate mortgages may have different underwriting criteria. With Think Homewise, you’re not stuck with one bank. Because they work with many lenders, they can find the loan type that matches your risk profile. Explore tailored options by shopping around using Think Homewise’s platform — fill out an application online in just 5 minutes. Step 7: Reapply — Better Than Before Once you’ve addressed the reasons for your first denial, it’s time to try again—better prepared. Before submitting: Double-check all documents. Ask your Homewise advisor to do a mock review with you. Approach lenders who may have more flexible requirements.

With Think Homewise, you have the benefit of human guidance and digital tools: their online platform helps you compare lender options and pick the one most aligned with your improved financial profile. Reapply with confidence — start your pre-approval journey with Think Homewise. How to Get Pre-Approved for a Mortgage Getting pre-approved for a mortgage is the first step toward buying a home. Here’s how: 1.Check your credit score–make sure it’s accurate and in good shape. 2.Gather documents– pay stubs, bank statements, tax returns, and info on debts. 3.Know your budget– consider monthly payments, taxes, and insurance. 4.Compare lenders– banks, credit unions, and mortgage brokers may offer different rates. 5.Apply– submit your paperwork for review. 6.Get your pre-approval letter–this shows sellers you’re ready and qualified. FAQs Q1. How long after a denied mortgage pre-approval should I wait to reapply? A: It depends on what caused the denial. If it was due to high credit card debt, once you’ve paid that down meaningfully, then perhaps after 6–12 months of steady income, if due to employment stability. With Think Homewise, you can talk to an advisor who will help you assess your timeline based on your specific situation in Toronto. Q2. Will applying again hurt my credit score? A: A denial from pre-approval often comes from a “soft”credit check, which doesn’t impact your score. However, submitting full mortgage applications to multiple lenders may involve “hard” credit checks, which can show up. That’s why it helps to use a comparison platform, like Think Homewise, to narrow down your best options before doing hard pulls. Q3. What documents will I need when I reapply with an improved profile? A: Expect the usual: recent pay stubs, T4s or Notice of Assessment, proof of down payment, credit report, bank statements, and proof of identity. If you’ve improved your credit or income, bring documentation of payments, contracts, or side income. Think Homewise will walk you through

exactly which docs each lender will require, so you don’t end up missing something that causes another denial. Real-Life Example: A Torontonian’s Comeback Shanaz M. from East York dreamed of a Leslieville condo—but her first mortgage application was denied. With guidance from Think Homewise, the best mortgage broker in Toronto, she fixed credit errors, paid down debt, and built her savings. A year later, she got pre-approved at a better rate and is now happily living near Queen Street. Final Thoughts Getting a mortgage pre-approval denial in Toronto can feel like a huge setback—but in most cases, it’s not permanent. It’s a warning, not a stop sign. You have options. With small changes— credit fixes, lowering debt, proving stable income, improving down payment—you can shift the odds in your favour. If you’re ready to regroup, refocus, and make your case stronger, Think Homewise is ready to help you every step of the way. Whether it's getting your documentation in order, understanding what lenders in Ontario will accept, or comparing your mortgage options, they’ve got your back. Don’t let denial close the door on your dream. Apply with Think Homewise, get a personalized review today, and let’s unlock your path to homeownership in Toronto.