Download

1 / 36

360 likes | 755 Views

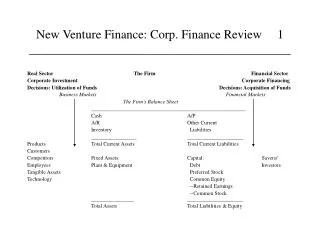

New Venture Finance: Corp. Finance Review 1 __________________________________________. Real Sector The Firm Financial Sector Corporate Investment Corporate Financing Decisions: Utilization of Funds Decisions: Acquisition of Funds

E N D

New Venture Finance: Corp. Finance Review 1__________________________________________ Real Sector The Firm Financial Sector Corporate Investment Corporate Financing Decisions: Utilization of Funds Decisions: Acquisition of Funds Business Markets Financial Markets The Firm's Balance Sheet __________________________________________________________ Cash A/P A/R Other Current Inventory Liabilities _________________ _____________________ Products Total Current Assets Total Current Liabilities Customers Competitors Fixed Assets: Capital: Savers/ Employees Plant & Equipment Debt Investors Tangible Assets Preferred Stock Technology Common Equity --Retained Earnings --Common Stock ________________ _____________________ Total Assets Total Liabilities & Equity

New Venture Finance: Corp. Finance Review 2__________________________________________ • Financing (sources of funds) must equal the investment in assets (use of funds). • Managers make investment decisions that generate earnings so that investors get a return on investment. • Financial Management is defined as the planning for, acquiring, and utilization of funds in a manner that maximizes the firm’s economic efficiency.

New Venture Finance: Corp. Finance Review 3__________________________________________ The Corporate Finance View of the World: Bus. Transactions $$ $$ Securities Commercial Sector -Customers -Products -Technology -Competitors Firm’s Balance Sheet Assets Liab. Capital Financial Sector Savers/Investors: -Individuals -Corporations -Partnerships -Banks Return on Investment Firm’s Income Statement Revenue -Expenses -Taxes Net Income Retained Earnings? Dividends?

New Venture Finance: Corp. Finance Review 4__________________________________________ • The corporation has advantages over the other forms or organization: • Unlimited lives that extend beyond the lives of the founders or original managers. • Simple transferability of ownership: investors and managers are two separate groups, so investors can buy or sell the common stock without disrupting corporate operations. • Limited liability in the corporation: investors can lose only the total amount they invested in the common stock.

New Venture Finance: Corp. Finance Review 5__________________________________________ • The stock market monitors the publicly-traded corporation’s performance: • Stock price changes signal whether managerial decisions are good (stock price goes up) are bad (stock price goes down). • Because of the requirements to disclose information that publicly-traded corporations face, the stock market can monitor these firms better than it can the other forms of organization.

New Venture Finance: Corp. Finance Review 6__________________________________________ • The stock market disciplines the firm by causing the stock price to decline. In response, the firm can: • Change strategies. • The Board of Directors can replace the managers ( this is called internal governance). • The firm can be merged/taken over (this is called the market for corporate control). • Declare bankruptcy.

New Venture Finance: Corp. Finance Review 7__________________________________________ • In the Theory of Finance, the appropriate goal of the firm is to maximize the value of shareholder wealth. • Shareholders commit part of their wealth to the firm when they buy the firm’s common stock. • Equivalent ways of stating this goal are: • To maximize the market value of the firm. • To maximize the stock price of the firm.

New Venture Finance: Corp. Finance Review 8__________________________________________ • An equation that is central to the Theory of Finance is: A Firm’s Stock Price = The Present Value of All Future Dividends DIV1 DIV2 DIV3 DIV∞∞ DIVt = ----------- + ----------- + ------------ + ... + ----------- = Σ ------------- (1 + k)1 (1 + k)2 (1 + k)3 (1 + k)∞ t=1 (1 + k)t

New Venture Finance: Corp. Finance Review 9__________________________________________ • This equation says that value (i.e., the stock price) depends on: • The stream of dividends. • Risk, reflected in the discount rate, k. • The timing of the dividends. • Note that value depends on all future dividends and not only on next quarter's dividends. • Where do dividends come from? • Dividends = (Earnings) • Earnings = (Revenue, Expenses, Interest Exp.,Other) • Revenue = (Business Decisions, Strategy)

New Venture Finance: Corp. Finance Review 10__________________________________________ • Agency Problems and Costs. Investors (principals) provide funds, but managers (agents) formulate and implement strategies and tactics: the problem of separation of ownership and control. • The goal is to maximize shareholder wealth, but investors cannot be sure that managers will act in shareholders’ best interests. Managers might: • Shirk their duties. • Use corporate resources to pay for perquisites. • Shift funds into higher risk projects than the stockholders desire.

New Venture Finance: Corp. Finance Review 11__________________________________________ • Observability, asymmetric information, & moral hazard: • Investors cannot observe everything managers do. • Managers have more information about the firm. • Investors monitor the firm, and the firm incurs monitoring costs. • Investor relations staffs, annual reports, SEC and other regulatory reports consume resources. • If managers’ actions cannot be observed directly, then periodic disclosure must be made: • Disclosure: information sets become more symmetric. • Are bank loan officers' salaries a monitoring cost?

New Venture Finance: Corp. Finance Review 12__________________________________________ • Agency problems can be solved if the interests of managers and investors are aligned, if both managers and investors have the same incentives. • Agency theory suggests if managers are bonded to the firm, managers would behave in the shareholders' best interests. • This entails bonding costs. For example, stock options or stock purchase programs (like at 85% of the market price) transform managers into owner/managers. • But managers are buying into the firm at below-market prices. The bonding cost is the loss of wealth suffered by other shareholders when the stock is sold “cheap.”

New Venture Finance: Corp. Finance Review 13__________________________________________ • These costs cause shareholder wealth to be less than if managers didn't pose a moral hazard. • We live in an imperfect world. • A perfect world of symmetric information no moral hazards is not attainable. • Financial contracting solutions are often used. • For example, bond indenture contracts often contain restrictive covenants that limit the behavior of managers, like no new mortgages on the assets. • Bank loans also contain restrictions, like limitations on paying dividends, the amount of additional borrowing, or a minimum current ratio requirement.

New Venture Finance: Corp. Finance Review 14__________________________________________ • A closer look at financial contracting. Bonds are loan contracts, and common stocks have legal ties to the firm via the firm's charter. • Bonds are fixed income securities that have finite lives: bonds have a fixed maturity date, pay a set amount of interest each period, and borrowings must be repaid. • Stocks are variable income securities that have infinite lives. Dividends are not guaranteed and stock never matures—as long as the firm is alive. Stocks can be repurchased by the firm, but that is different: stock can be retired but it does not mature. Stocks represent an equity, or ownership, interest in the firm.

New Venture Finance: Corp. Finance Review 15__________________________________________ Security Payment Priority _______________________________________________________________________________________________________________________________________ Debt Fixed, periodic interest Priority in bankruptcy Par value at maturity Preference over preferred & common Can force bankruptcy if not paid Preferred Fixed, periodic dividend Paid before common dividends Stock No maturity date Preference over common Div. must be declared Common No fixed dividend Residual position in dividend Stock No maturity date payment and bankruptcy Div. must be declared

New Venture Finance: Corp. Finance Review 16__________________________________________ • The Relationship Between Discount Rates and Value: • Like stock, bond prices also equal the present value of the cash flows that investors expect to receive: • Bond Price = P.V. of interest + P.V. of maturity value • Bond Interest = coupon rate X maturity value • Maturity Value = $1,000.00; called the bond’s principal • Consider a 10% , 1-year bond or a 10%, 5-year bond; both have a maturity value of $1,000. • Currently, bond interest rates are 10%, but rates may vary between 8% and 12% over the next few months. • How do changing interest rates affect bond values? Interest = .10 x $1,000 = $100 per year

New Venture Finance: Corp. Finance Review 17__________________________________________

New Venture Finance: Corp. Finance Review 18__________________________________________ • Define k as the Market Rate of Interest. The example shows that that k and a bond’s price are inversely related: • Bond prices goes up as k goes down. • Bond prices goes down as k goes up. • Note that the bond with the longer maturity (the 5-yr bond) has greater price volatility for the same changes in the interest rate. • The 5-yr bond has a higher price at 8% and a lower price at 12% than the 1-yr bond.

New Venture Finance: Corp. Finance Review 19__________________________________________ • Project evaluation techniques. Developing new products or services are essential if a firm is to continue growing. Capital budgeting involves: • Long-term investment opportunities as projects. • Conducting a cost/benefit analysis for each project. • Accepting projects when benefits exceed the costs. • Picking good projects allows the firm to grow and to increase its stock price. • The preferred technique is called Net Present Value (NPV).

New Venture Finance: Corp. Finance Review 20__________________________________________ • NPV = P.V. of Inflows - P.V. of Outflows n NCFt NPV = ------------------- - Cost of the project t=1 (1 + MCC)t where: NCFt = Net Cash Flow at time t MCC = the Marginal Cost of Capital, a risk-adjusted discount rate

New Venture Finance: Corp. Finance Review 21__________________________________________ • This gives rise to the following set of decision rules that are used in capital budgeting: • IRR is the Internal Rate of Return and is defined as the discount rate that makes NPV = 0.

New Venture Finance: Corp. Finance Review 22__________________________________________ • Who gets the NPV > 0 and how does it achieve the goal of the firm? • Common shareholders, the residual claimants. • Bondholders and preferred shareholders get what they expect, and common shareholders get what is left over. • The larger the residual, the more wealth common shareholders receive (think of the positive NPV that Intel creates with each new generation of microprocessors.) • If managers select all of the projects with NPV > 0, this is the best that shareholders can hope for and the stock price will be maximized. • Negative NPV’s would make the stock price go down.

New Venture Finance: Corp. Finance Review 23__________________________________________ • Informational efficiency: This important concept is the idea that having accurate information is crucial to making good investment decisions. • Financial markets are informationally efficient if security prices fully reflect all information and react immediately to impound new information. • For example, if the financial markets are efficient, then Intel’s stock price reflects all information about Intel. • Any new information about Intel will make its stock price go up or down immediately.

New Venture Finance: Corp. Finance Review 24__________________________________________ • One implication is that it is hard to "beat the market" in an efficient market. • The greatest rewards exist for those who have the best information; there is much competition for information. • The "big players" who have the most resources gain information first and grab the available profits first. • You and I, who are far from Wall Street and who spend little on information, find it difficult to beat the market. • Getting information first, or immediately, is very costly and it is difficult to beat the market and to cover the costs of obtaining information.

New Venture Finance: Corp. Finance Review 25__________________________________________ • Nevertheless, information efficiency is an important concept, and financial markets are pretty efficient in my opinion. • Competitive markets are key: as information becomes available, investors revise their decisions to buy or sell a stock or bond, so there must be markets in which they can actually buy or sell. • Economics and finance profs love markets: supply and demand come together and individuals are free to make buy or sell decisions that are in their best own interests. • As information arrives, it becomes reflected in prices, so price changes signal good news (prices up) or bad news (prices down).

New Venture Finance: Corp. Finance Review 26__________________________________________

New Venture Finance: Corp. Finance Review 27__________________________________________

New Venture Finance: Corp. Finance Review 28__________________________________________ • A basic principle of Finance: more risk should be rewarded with a higher return. • In the Theory of Finance, taking risk is a good thing since it creates new wealth (new products, new technologies, etc.) • Thus, there should be rewards for bearing risk.

New Venture Finance: Corp. Finance Review 29__________________________________________

New Venture Finance: Corp. Finance Review 30__________________________________________ • A life-cycle view of the growth of a technology-driven firm. Corporate Finance textbooks typically concentrate on firms that have gone beyond the start-up stage and are publicly-traded. • Publicly-traded firms have developed products and services that generate earnings from the assets in place. • Start-ups have no assets in place, and maybe are based on no more than a product or service concept. • The value of a publicly-traded firm is based on assets in place, a start-up’s value is based on its growth options.

New Venture Finance: Corp. Finance Review 31__________________________________________

New Venture Finance: Corp. Finance Review 32__________________________________________ • Venture Economics’ Stage Definitions: • Early Stage • Seed. A relatively small amount of capital provided to prove a concept, maybe involving product development but not initial marketing. • Startup. Financing for product development and initial marketing; no product sales, management team assembled, business plan written, market research done. • First Stage. Financing for initial commercial manufacturing and sales.

New Venture Finance: Corp. Finance Review 33__________________________________________ • Expansion • Second Stage. Working capital financing provided; likely to have no profits. • Third Stage. Financing for plant expansion, marketing, and working capital. • Bridge Stage. Financing for firm expected to go public in 6-12 months; often repaid from IPO proceeds. • Management/Leveraged Buyout (MBO/LBO) and Turnaround • later-stage companies: buying out existing firms or financing firms with operational or financial difficulties.

New Venture Finance: Corp. Finance Review 34__________________________________________

New Venture Finance: Corp. Finance Review 35__________________________________________

New Venture Finance: Corp. Finance Review 36__________________________________________