Download

1 / 38

380 likes | 401 Views

This event, hosted by Peter Pontuch of the European Commission in Luxembourg, covered the logic, accounting, and economic perspectives of data consolidation. It emphasized using sector data for economic analysis and understanding macroeconomic imbalance procedures, with a focus on current and desired states. The session concluded with insights on policy responses and the annual MIP cycle for handling imbalances.

E N D

Consolidated sector data and the analysis of macroeconomic imbalances Peter Pontuch European Commission DG Economic and Financial Affairs TF on data consolidation, Luxembourg, April 17-18 2013

Outline • The underlying logic of consolidation • The accounting perspective • The economic perspective • Use of sector data for economic analysis • Macroeconomic Imbalance Procedure • Analytical work • The current and the desired states • Conclusion 2

Outline • The underlying logic of consolidation • The accounting perspective • The economic perspective • Use of sector data for economic analysis • Macroeconomic Imbalance Procedure • Analytical work • The current and the desired states • Conclusion 3

The accounting perspective Consolidated data present the sector as if it were a single entity: only financial assets, liabilities, and transactions with other sectors are reported. • Intra-sector assets, liabilities and flows offset each other, whatever their nature: • Intra-group lending between a company and its resident subsidiaries, • “Inter-company” lending defined here as loans between two independent entities. 4

The accounting perspective: Intra-sector lending • Intra-group lending: • Between the corporate center and its resident subsidiaries, • Between peer companies of the same Group. • Inter-company lending: • Treasury investments (minor at the aggregate level), • Loans to associated companies that are not fully controlled subsidiaries, • Loans to customers or suppliers, esp. in a context of the recent credit tightness (e.g., in the recent period Rolls Royce distributed ~GBP 500m inter-company loans to strategic suppliers due to tight credit). 5

The accounting perspective Group A Company A1 L A A A L L SE SE SE Independent company B Subsidiary A2 (100%) 6

The accounting perspective Group A In consolidated sector data, the treatment of the intra-group loan of 50 (red) would be the same as the treatment of the inter-company loan of 30 (green). Total debt: 450 (non-cons.), 370 (cons.). 100 Company A1 L 200 A A A L L 50 SE SE SE 50 Independent company B 150 Subsidiary A2 (100%) 30 30 7

The economic perspective • Consolidated data reflect the amount of external funds received by the sector. • These funds allowed additional investment spending (corporate sector) or consumption (household sector). • Effects on economic activity: positive in the upturn phase, potentially negative if indebtedness needs to be reduced (deleveraging). • Relevant for measuring the credit boom-type of imbalances (e.g., IE and ES). • Non-consolidateddata also useful: risks coming from the distribution of debt across the sector. • Deleveraging pressures if debt concentrated in some parts of the sector. • Possible contagion effects. • But, it is necessary to distinguish intra-group and inter-company lending. 8

The economic perspective Group A The control of subsidiary A2 makes the intra-group loan relatively benign from an “imbalances” perspective. Little economic difference with the case where A2 was legally a part of A1. The intra-group loan was financed by A1, most likely through a corresponding liability (grey). Even if A2 defaults on its liability, A1 remains liable of the external liability. Non-consolidated data lead to double-counting. 100 Company A1 L 200 A A L 50 SE SE 50 Subsidiary A2 (100%) 9

The economic perspective Group A • A2 has little control over company B: • How the funds are spent (investment project), • Likelihood of repayment. • The loan was financed by A2 (grey). If B defaults: possible contagion on A2. 100 Company A1 L A A A L L SE SE SE Independent company B 150 Subsidiary A2 (100%) 30 Again, there is double-counting in non-consolidated data. But consolidated data do not capture the whole story (if B defaults there is a risk of contagion). 30 10

Outline • The underlying logic of consolidation • The accounting perspective • The economic perspective • Use of sector data for economic analysis • Macroeconomic Imbalance Procedure • Analytical work • The current and the desired states • Conclusion 11

The Macroeconomic Imbalance Procedure Role and Scope • External positions (current accounts, net international investment positions) • Competitiveness developments (REERs, ULCs) • Export performance (export market shares) • Private sector indebtedness (credit, debt) • Public sector indebtedness • Assets markets (housing) • Financial sector developments (as of 2012) External imbalances Internal imbalances 12

Policy response No problem Procedure stops. In-depth reviews Analysis to distinguish between benign and harmful macroeconomic developments and to identify policy options Imbalance exists Commission/Council recommendations under Article 121.2 Severe imbalance Commission/Council recommendation under Article 121.4 MIP: annual cycle November April/May April Alert Mechanism Report Economic reading of early warning scoreboard to identify Member States with potential risks Scoreboard Additional indicators Any other relevant data and analytical work Scoreboard Additional indicators Data use

Relevance for MIP: consolidated or non-consolidated? • Excessive private sector debt implies risks for growth and financial stability and increases the vulnerability to economic shocks. • Consolidated debt determines the amount the sector received from (and needs to ultimately repay to) other sectors. Relevant for effects on economic activity (imbalances in the boom years if excessive investment) and vulnerability to economic shocks (risks of deleveraging in the adjustment phase). • Non-consolidated debt provides information about the total gross indebtedness of the sector, acknowledging that some financing may be intra-sector. Could signal deficiencies in access to finance from the financial sector, and point to financial stability issues (contagion) and issues with distribution of debt and assets in the sector. 14

Relevance for MIP: consolidated or non-consolidated? • Non-consolidated data are available for all MS and less subject to heterogeneity in national reporting and consolidation practices. • However, non-consolidated data have drawbacks: • Contain both intra-group and inter-company loans. The former are not an imbalance, merely reflecting corporate financing, accounting, and tax practices. • We do not know the relative weight of intra-group transactions within intra-sector liabilities of MS. • The intra-group financing practices (and hence their weight) likely differ across MS: comparability issues. 15

MIP Scoreboard: The basics • Screening device to identify potential imbalances requiring an in-depth review. • Selection of 11 indicators with indicative alert thresholds: thresholds mostly based on quantiles of historical data. Headline indicators complemented with a set of "additional indicators". • The Alert Mechanism Report presents an economic reading of indicators, and proposes a list of MS requiring in-depth reviews. The reading considers other relevant information, over a longer time horizon. • Presented on t-1 annual data but the economic reading considers latest data available at any frequency. • May be adjusted: As available data and experience evolve, technical adjustments in the definitions of the variables are possible. 16

Alert Mechanism Report 2012: private indebtedness as a prominent issue The AMR provides an economic reading of the latest Scoreboard for all EU27 MS, considering the indicators' evolution over time, as well as additional indicators. The 2012 AMR discusses private debt in more detail in 16 MS. In 2 cases of high private indebtedness (non-consolidated), the findings were qualified by the effect of inter-company loans on the levels of debt. The AMR selected 14 MS for an In-depth review (private debt issues mentioned to some extent in all 14): Belgium, Bulgaria, Denmark, Spain, France, Italy, Cyprus, Hungary, Malta, Netherlands, Slovenia, Finland, Sweden and the United Kingdom. 19

In-depth reviews 2013 and private debt • On April 10 2013 the Commission published 13 IDRs. • In 11 cases there was a specific focus on private debt (BG, BE, ES, FR, HU, MT, NL, FI, SE, SI, UK), generally based on the headline non-consolidated private debt data. • In 10 cases the analysis was either complemented with consolidated data or qualified by intra-sector lending practices. • Additional country-specific issues were also raised: • Increase in account payable financing (BG), corporate tax optimization practices (BE, SE), special-purpose entities (HU), cross-border lending (SE, FI, UK). 20

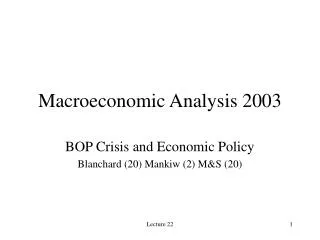

Example: Belgian IDR 2013 • Non-consolidated private debt at 237% of GDP in 2011 (3rd in EU). • Large part due to NFCs: 182.5pp vs. 99pp in the euro area. • Consolidated debt of NFCs only at 89.4pp vs. 81.4pp in the euro area. • The large difference is due to intragroup lending practices (financial centres). • Allowance for Corporate Equity policy introduced in 2006 encourages triangular schemes between group financing entities and subsidiaries. • Assessment: The risks of high corporate indebtedness are attenuated by the underlying factors. The cost of these practices is statistical noise and reduced tax revenues. 21

Example: Belgian IDR 2013 Debt Decomposition, All Sectors, Non-Consolidated Debt Decomposition, All Sectors, Consolidated Source: Commission services. Note: * indicates estimated figure using quarterly data. 22

Analytical work: A study on private deleveraging The Commission recently published the study Indebtedness, Deleveraging Dynamics and Macroeconomic Adjustment (European Economy - Economic Papers 477, April 2013). Four aims: Identification of deleveraging pressures in the private sector; Quantification of these pressures; Refining the message using credit supply and demand conditions; Simulation of the impact of a household deleveraging shock. 23

Identification of deleveraging pressures • Challenge: examine and summarize several alternative indicators of indebtedness. • Approach: Composite indicators based on clustering and PCA methods. • Two dimensions: debt to capacity to repay and debt to assets. For each we use alternative definitions of indebtedness ratios (GDP or GOS/GDI for the former, assets or deflated assets for the latter). • Focus on current levels of debt as well as accumulation over 2000-2008. • The main analysis uses non-consolidated data (availability, consistency with MIP). • Robustness check using consolidated data for NFCs confirms the findings for all MS, except BE (intra-sector lending). 24

Identification of deleveraging pressures for non-financial corporates Non-financial corporates sector deleveraging pressures considering the capacity to repay Non-financial corporates sector deleveraging pressures considering assets 25

Identification of deleveraging pressures for non-financial corporates Composite indicator on deleveraging pressures for EU27 Member States, Non-financial corporates Main finding: Deleveraging pressures in the NFC sector identified for: BE, BG, CY, EL, ES, HU, IE, IT, PT, SI, SE, UK, EE, LV. 26

Outline • The underlying logic of consolidation • The accounting perspective • The economic perspective • Use of sector data for economic analysis • Macroeconomic Imbalance Procedure • Analytical work • The current and the desired states • Conclusion 27

Availability: not there yet! • Currently, annual consolidated data available for all EU27 except UK. Quarterly consolidated data are more problematic. • Back in 2011, the incompleteness of annual (and absence of quarterly) consolidated data was one of the arguments against using them as the headline indicator in the MIP Scoreboard. • They nevertheless serve as additional indicator. • But… • Availability (i.e. being able to get a data point from the ESTAT database) is not everything, since there are reasonable doubts about reliability of these data. 28

Plausibility: what you see and what you get Non-consolidated and consolidated NFC debt (AF3, AF4), % of GDP • Difference between non-consolidated and consolidated NFC debt (AF3 and AF4) is in many cases very small. • In EA27 the difference between NC and C debt ranges from 0 pp to 93 pp. • Some of this heterogeneity is real. • Some is probably due to inconsistent practices, especially in the grey zone and beyond… • Even worse, this throws doubt even on the quality of NC data. Does NC mean the same thing everywhere? Plausible Grey zone Implausible Source: ESTAT 29

Consistency: how bad is it? • What we know is that national consolidation practices differ. • We do not know: • What is the order of magnitude of the discrepancies generated by different practices? • Do we have clusters of MS with comparable consolidation practices? • How consistent were the practices over time? Are historical data series reliable? 30

Country specificities: noise or patterns? • Even with consistent consolidation practices across all MS, some country-specific differences will continue to affect the comparability of C/NC figures: • Depth of corporate groups and intra-group financing; • Cross-border financing of foreign subsidiaries; • Financial engineering practices (e.g., SPEs and tax optimization). • A strong need to know more about these issues. 31

Problems with the current state • Due to the issues discussed, our current analysis of private balance sheets relies more heavily on non-consolidated data. • Consolidated data are used as a qualifier, if they are available and if they "look plausible". • This is not optimal, as both C and NC (and the gap) are relevant for the analysis of macroeconomic imbalances. • The quality of data that we use is not clear. • The plausibility criterion is insufficient. • Can we trust at least the NC data? 32

The ideal state • Transparent and consistent consolidation rules applied homogeneously across EU27. • Both current and historical data. • Even in that case one needs additional information about: • The extent of intra-group lending which is a noise in NC data (for our purposes), • Multinational HQs and their foreign subsidiary lending, • Effects of SPEs. • At least occasional insights on these three topics would be extremely helpful. 33

Conclusions • Our current analysis uses primarily non-consolidated data, complemented by consolidated data when available. • Consistence and quality of the consolidated figures is not completely clear. • Both consolidated and non-consolidated data would be useful for the analysis of macroeconomic imbalances. • Ideally: a set of common transparent and consistent consolidation rules applied in all EU27. • Both current and historical data. • Additional insights into intra-group lending, foreign subsidiary lending, SPEs would be also very useful. 34

Macroeconomic Imbalance Procedure: context • MIP introduced as part of the Six-Pack in late 2011: • Turbulent economic circumstances–sovereign crises and poor growth • High uncertainty/stress in financial markets • Significant risks of negative spillovers, especially in the euro area • Large stocks of imbalances from the pre-crisis period • Significant but still incomplete adjustment • Incomplete institutional framework 37