Download

1 / 4

40 likes | 53 Views

"What If Credit of F.Y. 20-21 Is Still Not Reflecting In GSTR 2A Due To Which ITC Was Not Availed?<br>As everyone is well aware that as per Section 16(4) of the CGST Act:<br>u201cA registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the due date of furnishing..."<br>Read more at https://taxguru.in/goods-and-service-tax/itc-f-y-20-21-reflecting-gstr-2a.html

E N D

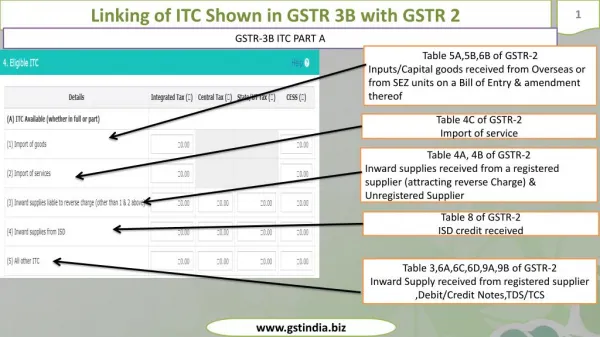

What If ITC of F.Y. 20-21 Is Still Not Reflecting In GSTR 2A taxguru.in/goods-and-service-tax/itc-f-y-20-21-reflecting-gstr-2a.html What If Credit of F.Y. 20-21 Is Still Not Reflecting In GSTR 2A Due To Which ITC Was NotAvailed? As everyone is well aware that as per Section 16(4) of the CGSTAct: “A registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the due date of furnishing ofthe return under section 39 for the month of September following the end of financial year to which such invoice or debit note pertains or furnishing of the relevant annualreturn, whichever isearlier.” Hence, if there is any credit that is still pending to be taken for F.Y. 20-21, then the same needs to be taken before the due date of furnishing of the return for the month of September 2021 under Section 39 of the CGSTAct. Now as per Rule 36(4) of the CGSTRules: “Input tax creditto be availed by a registered person in respect of invoices or debit notes, the details of which have not been furnished by the suppliers under sub-section(1) of section 37, in FORM GSTR-1 or using the invoice furnishing facility shall not exceed 5 per cent of the eligible credit available in respect of invoices or debit notes the details of which have been furnished by the suppliers under sub-section (1) of section 37 in FORM GSTR-1 or using the invoice furnishingfacility”

Now, if a taxpayer has taken eligible credit in his books of accounts and due to the faultof the supplier the same is not appearing in the GSTR 2A of the taxpayer even till the due date of filing of the return for the month of September then what is the recourse available to the taxpayer in such a scenario? Will the taxpayer be made to suffer for no fault ofhis? Watch Video At: https://youtu.be/oEev04FeDoE In this regard I would like to bring to light Rule 37(4) of the CGST Ruleswhich statesas under: “(4) The time limit specified in sub-section (4) of section 16 shall not apply to a claimfor reavailing of any credit, in accordance with the provisions of the Act or the provisionsof this Chapter, that had been reversedearlier.” So, in my opinion if we avail the credit in the GST return as per the books of accounts if the same is still not appearing in GSTR 2A and reverse it in the same month then there will not be any consequence with regards to interest and as mentioned in Rule 37(4),the time limit mentioned in Section 16(4) for re-availing the credit will notapply. Further reliance can also be placed on Circular No. 990/14/2014- Central excise-8dated 19.11.2014 wherein it was stated that, “ The purpose of the amendmentmade by Notification No. 21/2014-CE (NT) dated 11.07.2014is to ensure that after theissue of a document under sub-rule (1) of Rule 9, credit is taken for the first time withinsix months of the issue of the document. Once this condition is met, the limitation has no further application. It is, therefore, clarified that in each of the three situations described above pertaining to Rule 4(7), Rule 3(5B) or Rule 4(5) (a) of CCR, 2004, the limitation of six months would apply when the credit is taken for the first time on an eligibledocument. It would not apply for taking re-credit of amount reversed, after meeting the conditions prescribed in theserules”

Hence, going by the above provisions it can be said that with regards to re-availment of credit there is no time limit and this route can be taken by the taxpayers to avoidblockage of input tax credit taken in a genuine manner. However, this may also be subjectto litigation and the hence suitable clarifications in this regard should beissued. Tags: goods and services tax, GST, input taxcredit Kindly Refer to Privacy Policy & Complete Terms of Use andDisclaimer. AuthorBio Name: VISHAKA GOYAL Qualification: CA in Practice Company: GOYAL RATHI ANDASSOCIATES Location: SURAT, Gujarat,India Member Since: 07 Oct 2021 | Total Posts:1 View Full Profile Join Taxguru’s Network for Latest updates on Income Tax, GST, Company Law, Corporate Laws and other related subjects. Join Taxguru Group onTelegram TELEGRAM GROUPLINK

More Under Goods and ServicesTax «PreviousArticle Next Article» 12Comments Leave aComment Your email address will not be published. Required fields are marked*