Download

1 / 11

110 likes | 135 Views

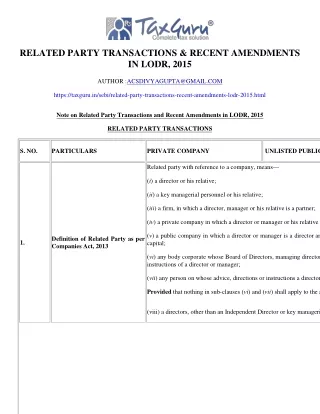

"Note on Related Party Transactions and Recent Amendments in LODR, 2015 RELATED PARTY TRANSACTIONS S. NO. PARTICULARS PRIVATE COMPANY UNLISTED PUBLIC COMPANY L"<br>TaxGuru is a platform that provides Updates On Amendments in Income Tax, Wealth Tax, Company Law, Service Tax, RBI, Custom Duty, Corporate Lawu00a0, Goods and Service Tax etc.<br>To know more visit https://taxguru.in/sebi/related-party-transactions-recent-amendments-lodr-2015.html

E N D

RELATED PARTY TRANSACTIONS & RECENT AMENDMENTS IN LODR, 2015 AUTHOR :ACSDIVYAGUPTA@GMAIL.COM https://taxguru.in/sebi/related-party-transactions-recent-amendments-lodr-2015.html Note on Related Party Transactions and Recent Amendments in LODR, 2015 RELATED PARTY TRANSACTIONS S. NO. PARTICULARS PRIVATE COMPANY UNLISTED PUBLIC COMPANY LISTED COMPANY Related party with reference to a company, means— (i) a director or his relative; (ii) a key managerial personnel or his relative; (iii) a firm, in which a director, manager or his relative is a partner; (iv) a private company in which a director or manager or his relative is a member or director; (v) a public company in which a director or manager is a director and holds along with his relatives, more than two per cent of its paid-up share capital; Definition of Related Party as per Companies Act, 2013 1. (vi) any body corporate whose Board of Directors, managing director or manager is accustomed to act in accordance with the advice, directions or instructions of a director or manager; (vii) any person on whose advice, directions or instructions a director or manager is accustomed to act: Provided that nothing in sub-clauses (vi) and (vii) shall apply to the advice, directions or instructions given in a professional capacity; (viii) a directors, other than an Independent Director or key managerial personnel of the Holding Company or his relative.

(ix) any body corporate which is— (A) a holding, subsidiary or an associate company of such company; (B) a subsidiary of a holding company to which it is also a subsidiary; or (C) an investing company or the venturer of the company;”; N.A. Explanation.—For the purpose of this clause, “the investing company or the venturer of a company” means a body corporate whose investment in the company would result in the company becoming an associate company of the body corporate.] (i) Related party as per Companies Act, 2013 (ii) Related Parties as defined under Applicable Accounting Standards – IND AS 24. *Definition of Related Party- has been widened to include the following: (a) Any person or entity forming a part of the promoter group of the Company; or Definition of Related Party as per LODR, 2015 2. N.A. (b) Any person or any entity, holding 20% or more equity shares of the Company and w.e.f. 1st April 2023, 10% or more equity shares of the Company, at any time, during the immediate preceding Financial Year. *Inserted by SEBI (LODR)(Sixth Amendment) Regulations, 2021, w.e.f 01.04.22

Relative’ with reference to any person, means anyone who is related to another, if— (1). they are members of a Hindu Undivided Family (2). they are husband and wife (3). Father : Provided that the term “Father” includes step-father (4). Mother : Provided that the term “Mother” includes step-mother (5). Son : Provided that the term “Son” includes step-son 3. Definition of Relative (6). Son’s wife (7). Daughter (8). Daughter’s husband (9). Brother : Provided that the term “Brother” includes step-brother (10). Sister : Provided that the term “Sister” includes step-sister Related Party Transactions as prescribed under Section 188(1) of Companies Act, 2013: (a) sale, purchase or supply of any goods or materials; (b) selling or otherwise disposing of, or buying, property of any kind; Related Party Transactions (c) leasing of property of any kind; 4. as per Companies Act, 2013 (d) availing or rendering of any services; (e) appointment of any agent for purchase or sale of goods, materials, services or property; (f) such related party’s appointment to any office or place of profit in the company, its subsidiary company or associate company; and (g) underwriting the subscription of any securities or derivatives thereof, of the company.

*Related party transaction means a transaction involving a transfer of resources, services or obligations between: (a) the Company and its related parties; (b) the Company and Related Parties of subsidiaries; (c) Transactions between Subsidiaries and Related Parties of the Company; (d) Transactions between Subsidiaries and Related Parties of subsidiaries; and (e) W.e.f. 1st April 2023, it shall also include the Company or its subsidiaries on one hand, and any other person or entity on the other hand, the purpose and effect of which is to benefit a related party of the Company or its subsidiaries. regardless of whether a price is charged and a “transaction” with a related party shall be construed to include a single transaction or a group of transactions in a contract: Related Party Transactions as per LODR, 2015: 5. Exemption from purview of RPT- Not applicable in case of Private and Unlisted Public Companies (a) Issue of Equity Shares/ other securities convertible into equity shares, on preferential basis. (b) Following Corporate actions which are uniformly applicable/ offered to all Shareholders: (i) Payment of Dividend (ii) Sub-division /consolidation of securities (iii) Issuance of securities by way of Rights/Bonus Issue, (iv) Buy-back of securities. (c) Acceptance of fixed deposits by banks/Non-Banking Finance Companies at applicable/offered to all shareholders /public, subject to disclosure of the same along with the disclosure of related party transactions every six months to the stock exchange(s), in the format as specified by SEBI. the terms uniformly *Inserted by SEBI (LODR)(Sixth Amendment) Regulations, 2021, w.e.f 01.04.22 REVIEW MECHANISM/APPROVAL/RATIFICATION

All transactions of the company with related parties and subsequent modifications shall require approval of Audit Committee. Exemption: Audit Committee Approval as per Companies Act, 2013 6. The approval shall not be required for transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval.

*(a) RPTs and subsequent material modifications therein, shall require prior approval of the Audit Committee of the Company. (b) Audit Committee to define Material Modifications in Related Party Transactions and disclose it as a part of Policy on Materiality of Related Party Transactions and on Dealing with Related Party Transactions. (c) Only those members of Audit Committee who are Independent Directors shall approve such RPTs and subsequent material modifications therein. (d) RPTs in which the Company is not a party but Subsidiary is a party, shall require prior approval of the Audit Committee of the Company, if the value of such transaction(s) during a financial year exceeds: (i) W.e.f. 1st April 2022, 10% of the annual consolidated turnover as per the last audited financial statements of the Company; (ii) W.e.f. 1st April 2023, 10% of the annual standalone turnover as per the last audited financial statements of the subsidiary. Exemption: Audit Committee Prior Approval as per LODR, 2015 7. N.A. Prior approval shall not be applicable in the following cases: (a) *RPT to which listed subsidiary is a party but the Company in not a party, if Regulation 23 and Regulation 15(2) are applicable to listed subsidiary. For RPT of unlisted subsidiaries of the listed subsidiaries, the prior approval of the audit committee of the listed subsidiary shall suffice. (b) transactions entered into between two government companies; (c) transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval. *(c) transactions entered into between two wholly- owned subsidiaries of the listed holding company, whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval. * Inserted by SEBI (LODR)(Sixth Amendment) Regulations, 2021, w.e.f 01.04.22

Audit Committee may make omnibus approval for related party transactions proposed to be entered into by the company subject to the following conditions, namely (1) The Audit Committee shall, after obtaining approval of the Board of Directors, specify the criteria for making the omnibus approval (2) The Audit Committee shall consider the following factors while specifying the criteria for making omnibus approval, namely: – (a) repetitiveness of the transactions (in past or in future); (b) justification for the need of omnibus approval. (3) The Audit Committee shall satisfy itself on the need for omnibus approval for transactions of repetitive nature and that such approval is in the interest of the company. (4) The omnibus approval shall contain or indicate the following: – (a) name of the related parties; Omnibus Committee as per Companies Act, 2013 Approval of Audit (b) nature and duration of the transaction; 8. (c) maximum amount of transaction that can be entered into; (d) the indicative base price or current contracted price and the formula for variation in the price, if any; and (e) any other information relevant or important for the Audit Committee to take a decision on the proposed transaction: Provided that where the need for related party transaction cannot be foreseen and aforesaid details are not available, audit committee may make omnibus approval for such transactions subject to their value not exceeding rupees one crore per transaction. (5) Omnibus approval shall be valid for a period not exceeding one financial year and shall require fresh approval after the expiry of such financial year. (6) Omnibus approval shall not be made for transactions in respect of selling or disposing of the undertaking of the company. Exemption: The approval shall not be required for transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval.

Audit committee may grant omnibus approval for related party transactions proposed to be entered into by the listed entity subject to the following conditions, namely- (1) the audit committee shall lay down the criteria for granting the omnibus approval in line with the policy on related party transactions of the listed entity and such approval shall be applicable in respect of transactions which are repetitive in nature; (2) the audit committee shall satisfy itself regarding the need for such omnibus approval and that such approval is in the interest of the listed entity; (3) the omnibus approval shall specify: the name(s) of the related party, nature of transaction, period of transaction, maximum amount of transactions that shall be entered into, the indicative base price / current contracted price and the formula for variation in the price if any; and such other conditions as the audit committee may deem fit: Omnibus Committee as per LODR, 2015 Approval of Audit 9. N.A. Provided that where the need for related party transaction cannot be foreseen and aforesaid details are not available, audit committee may grant omnibus approval for such transactions subject to their value not exceeding rupees one crore per transaction. (4) the audit committee shall review, atleast on a quarterly basis, the details of related party transactions entered into by the listed entity pursuant to each of the omnibus approvals given. (5) Such omnibus approvals shall be valid for a period not exceeding one year and shall require fresh approvals after the expiry of one year: Exemption: The same as in the case of Audit Committee Approval as stated above.

All Related Party Transactions: (a) which are in Ordinary Course of Business and not at arm’s length basis; (b) which are not in Ordinary Course of Business and not at arm’s length basis; and (c) all Material Transactions shall also be approved by the Board of Directors at a meeting or through a Resolution passed by Circulation in the case of urgent requirements, in the interest of the Company subject to ratification at their next following Board Meeting. 10. Board Approval Where any director is interested in any contract or arrangement with a related party, such director shall not be present at the meeting during discussions on the subject matter of the resolution relating to such contract or arrangement. Exemption: Approval shall not be required for: 1. transactions entered into by the company in its ordinary course of business and on an arm’s length basis. 2. transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval. All Material Related Party Transactions shall be approved by the Members by the way of an Ordinary Resolution. Exemption: Approval shall not be required for: Shareholders Approval as per Companies Act, 2013 11. 3. transactions entered into by the company in its ordinary course of business and on an arm’s length basis. 4. transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval.

The contracts or arrangements related to- (i) sale, purchase or supply of any goods or material, directly or through appointment of agent, amounting to ten percent or more of the turnover of the company. (ii) selling or otherwise disposing of or buying property of any kind, directly or through appointment of agent, amounting to ten percent or more of net worth of the company. (iii) leasing of property of any kind amounting to ten percent or more of the turnover of the company. (iv) availing or rendering of any services, directly or through appointment of agent, amounting to ten percent or more of the turnover of the company. Material Transactions as per Companies Act, 2013 Related Party 12. Explanation.- It is hereby clarified that the limits specified in sub-clause (i) to (iv) shall apply for transaction or transactions to be entered into either individually or taken together with the previous transactions during a financial year. (v) for appointment to any office or place of profit in the company, its subsidiary company or associate company at a monthly remuneration exceeding two and a half lakh rupees. (vi) is for remuneration for underwriting the subscription of any securities or derivatives thereof, of the company exceeding one percent of the net worth. Explanation.- (1) The turnover or net worth referred above shall be computed on the basis of the audited financial statement of the preceding financial year. All material related party transactions and subsequent material modifications shall require prior approval of the shareholders through resolution and no related party shall vote to approve such resolutions whether the entity is a related party to the particular transaction or not. Shareholders Prior Approval as per LODR, 2015 13. N.A. Exemption: The same as in the case of Audit Committee Approval as stated above.

*A transaction with a Related Party shall be considered material if: (1) the transaction(s) entered individually or together with previous transactions during a financial year, exceeding Rs.1000 crore Consolidated Turnover of the Company as per the last audited financial statements, whichever is lower. or 10% of Annual Material Transactions as per LODR, 2015 Related Party (2) transaction involving payments made to a related party with respect to brand usage or royalty, if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceed five percent of the annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity. 14. N.A. *Inserted by SEBI (LODR)(Sixth Amendment) Regulations, 2021, w.e.f 01.04.22