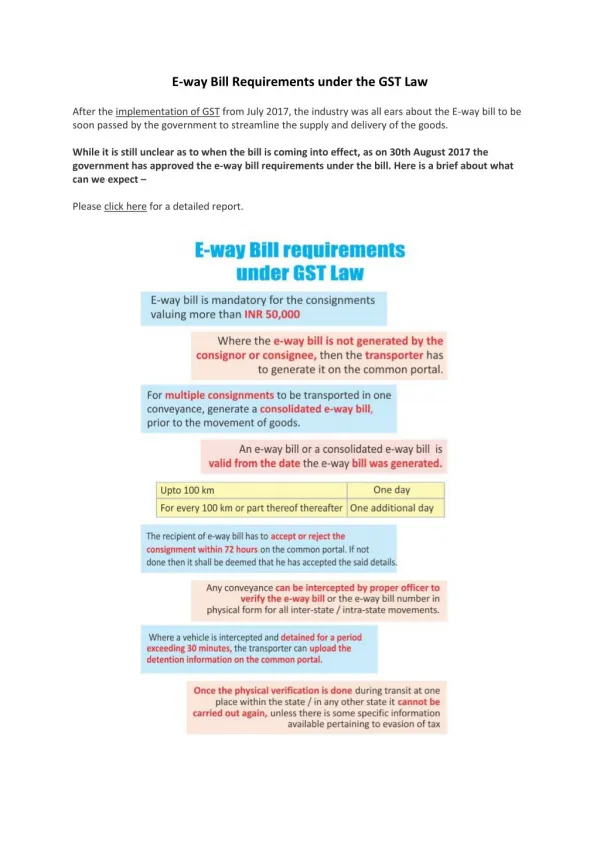

Download

1 / 6

60 likes | 71 Views

"There is full code of law for Reverse Charge under GST. There is definition clause for reverse charge, goods or services are specified on which reverse charge b"<br>TaxGuru is a platform that provides Updates On Amendments in Income Tax, Wealth Tax, Company Law, Service Tax, RBI, Custom Duty, Corporate Lawu00a0, Goods and Service Tax etc.<br>To know more visit https://taxguru.in/goods-and-service-tax/full-code-law-reverse-charge-mechanism-gst.html

E N D

FULL CODE OF LAW FOR REVERSECHARGEMECHANISM UNDERGST AUTHOR :PARVEEN KUMAR MAHAJAN https://taxguru.in/goods-and-service-tax/full-code-law-reverse-charge-mechanism-gst.html There is full code of law for Reverse Charge under GST. There is definition clause for reverse charge, goods or services are specified on which reverse charge be applicable, supplier and recipient notified for the purpose of reverse charge, time of supply provisions available for reverse charge, input tax definition is also there for reverse charge etc… I shall try to discuss all provisions relating to the Reverse Charge in thisarticle. What is ReverseCharge? Section 2(98) CGST Act – “reverse charge” means the liability to pay tax by the recipient of supply of goods or services or both instead of the supplier of such goods or services or both under sub-section (3) or sub-section (4) of section 9, or under sub-section (3) or sub-section (4) of section 5 of the Integrated Goods and Services Tax Act. Thus, tax liability on supply of goods or services or both specified under sections 9(3) CGST, 9(4) CGST, 5(3) IGST and 5(4) IGST shall be paid by the Recipient. The notifications for the purpose of Reverse Charge are issued under theseprovisions. Difference between the provisions stated under sub-section 3 of section 9 and sub-section 4 of section 9 of theCGST.

The person either registered unregisteredperson Supplier of the Goods orServices or Only UnregisteredPerson Any Recipient who receives specified goodsorservices.IftheRecipientisnot registeredthenheshallhavetoregisterOnlyNotifiedRegisteredPerson compulsory according to section 24(iii) CGST. Recipient Parent Notifications specifying Goods or Services, suppliers andrecipients

For which notification wasissued S.No. Notification Goods orServices Notification No.4/2017-Central Tax (Rate)For Goods Sub-Section CGST Sub-Section CGST Sub-Section CGST Sub-Section IGST 3 ofSec of Sec of Sec 3 ofSec 1 – Dated28-06-2017 Notification No.13/2017-Central Tax (Rate)ForServices 2 – Dated28-06-2017 Notification No. 07/2019- Central TaxForServices 3 (Rate) – Dated29-03-2019 Notification No.4/2017-Integrated TaxForGoods 4 (Rate) –28-06-2017 Notification No.10/2017-Integrated TaxForServices Sub-Section 3 of Sec IGST 5 (Rate) –28-06-2017 • Whether tax paid on the basis of Reverse Charge is outputtax? • No. Tax paid on the basis of Reverse Charge is not an output tax. It has been cleared by definition stated under section 2 of the CGST. Clause 82 of Section 2 CGST says that “output tax” in relation to a taxable person, means the tax chargeable under this Act on taxable supply of goods or services or both made by him or by his agent but excludes tax payable by him on reverse chargebasis; • Time of Supply for reverse charge supply of goods – Section 12(3)CGST • In case of supplies in respect of which tax is paid or liable to be paid on reverse charge basis, the time of supply shall be the earliest of the following dates,namely:— • the date of the receipt of goods;or

the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier;or • the date immediately following thirty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by thesupplier: • Provided that where it is not possible to determine the time of supply under clause (a) or clause (b) or clause (c), the time of supply shall be the date of entry in the books of account of the recipient ofsupply. • Time of Supply for reverse charge supply of services – Section 13(3)CGST • In case of supplies in respect of which tax is paid or liable to be paid on reverse charge basis, the time of supply shall be the earlier of the following dates,namely:— • the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier;or • the date immediately following sixty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by thesupplier: • Provided that where it is not possible to determine the time of supply under clause (a) or clause (b), the time of supply shall be the date of entry in the books of account of the recipient ofsupply: • Provided further that in case of supply by associated enterprises, where the supplier of service is located outside India, the time of supply shall be the date of entry in the books of account of the recipient of supply or the date of payment, whichever isearlier. • Invoice provisions relating to Supply falling under Reverse ChargeMechanism • The Tax Invoice pertaining to supply of goods or services falling under reverse charge shall either be issued by the supplier himself if he is registered or by the recipient if the such supply is received from the person who is not registered under theGST. • There is mandate to issue the invoice within time as stipulated under the provisions of the GST. Timing to issue the invoice is as understated. • Supply of goods made by Registered Person– The invoice shall be issued before or at the time of, removal of goods where the supply involves movement of goods or delivery of goods or making available thereof to the recipient, in any other case. (Section 31(1)CGST) • Supply of service made by Registered Person– The invoice shall be issued before or after provision of service but within a period of thirty days from the date of the supply of service. (Section 31(2) CGST read with rule 47.) • Supply received from Unregistered Person – Section 31(3)(f) CGST – a registered person who is liable to pay tax under sub-section (3) or sub-section (4) of section 9 shall issue an invoice in respect of goods or services or both received by him from the supplier who is not registered on the date of receipt of goods or services orboth; • Payment Voucher – Payment voucher is mandate to issue if liability to pay tax fall under section 9(3) or 9(4)CGST

Section 31(3)(g) CGST– a registered person who is liable to pay tax under sub-section (3) or sub- section (4) of section 9 shall issue a payment voucher at the time of making payment to thesupplier. Input Tax – For the purpose of Reverse Charge Liability – Section 2(62)CGST According to this section Input Tax includes the tax payable under the provisions relating to reverse charge i.e. 9(3) CGST, 9(4) CGST, 5(3) IGST and 5(4)IGST. Input Tax Credit Provisions under section 16 CGST read with Rule 36 be applicable for availing Input Tax Credit towards supply falling under Reverse ChargeMechanism Such provisions contemplated under section 16(2) are asunder: Tax Invoice inpossession; Goods or Services has beenreceived; Tax Liability has been paidand Return has beenfurnished Relevant provisions enumerated under clause (a) and (b) of sub-rule (1) of Rule 36 require for claiming input tax creditthat an invoice issued by the supplier of goods or services or both in accordance with the provisions of section31; an invoice issued in accordance with the provisions of clause (f) of sub-section (3) of section 31, subject to the payment oftax; Thus, merely Tax Invoice is not required in possession but it (Tax Invoice) must be issued in accordance with the provisions of section 31. If Invoice is not issued within time as stated under section 31 then it shall be treated as invoice was not issued in accordance with the provisions. If it is proved that invoice is not issued in accordance to the provisions of section 31, input tax credit may be denied foravailing Limitation Period to avail Input Tax Credit in the case of Supply falling under Reverse Charge Mechanism – Section 16(4)CGST The present provisions say that a registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the thirtieth day of November (before amendment – 20th October) following the end of financial year to which such invoice or debit note pertains or furnishing of the relevant annual return, whichever isearlier. For example, the registered person shall not be entitled to avail input tax credit if he failed to avail input tax credit towards reverse charge liability pertaining to the 2020-21 till 20th October2021. Conclusion– The term Reverse Charge Mechanism under the GST Law is being governed by followingprovisions. 1. Definition – Section 2(68)CGST

Goods or Services on which RCM be applied – Specified in Notifications issued under Section 9(3) and Section 9(4) CGST and Section 5(3) and Section 5(4)IGST Recipients and Suppliers for the purpose of reverse charge – See Notifications prescribed under relevant sections pertaining to reversecharge. Time of Supply for Supply of Goods – Section 12(3)CGST Time of Supply for Supply of Services – Section 13(3)CGST Invoice Provisions – Section 31 read with rule47 Input Tax in the case of Reverse Charge – Section 2(62)CGST Input Tax Credit Provisions – Section 16(2) CGST read with rule36 Limitation Period for availing Input Tax Credit – Section 16(4)CGST Interest, Penalty and Recovery – Provisions relating to interest, penalty and recovery shall apply to tax liability on account of reverse charge as if it is applied to liability towards regularsupply. Thus, it can be said there is full code of law under the GST for Reverse ChargeMechanism. To reach to me for any suggestions, rectifications, amendments and/or further clarifications in regard of this article my email address ispkmgstupdate@gmail.com. (PARVEEN KUMARMAHAJAN) Advocate