Download

1 / 12

120 likes | 135 Views

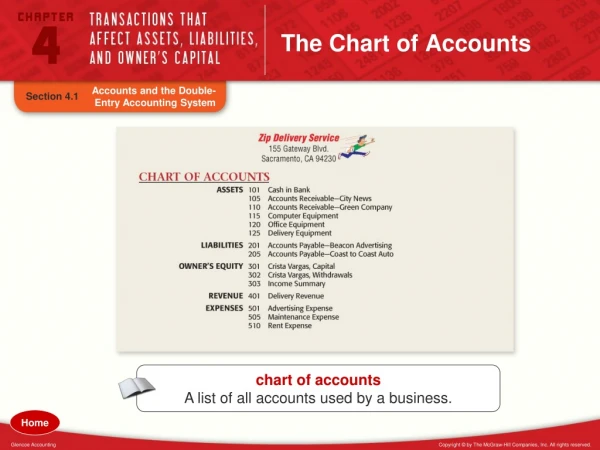

EXHIBIT A UNIFORM CHART OF ACCOUNTS GENERAL

E N D

EXHIBIT A UNIFORM CHART OF ACCOUNTS GENERAL INTRODUCTION: Use of this Uniform Chart of Accounts is mandatory for all Lodges as stated in Sections 4.330 and 13.040 of the Statutes. It is designed to allow flexibility in the number of different accounts each Lodge will use and is adaptable for use in a computerized system. Each Lodge will use the approved Chart of Accounts and distribute the listing to all concerned for use in classifying assets, liabilities, receipts and expenditures for entry into the accounting system. Use the minimum number of accounts that will satisfy the following requirements: Local Accounts and subaccounts can be added for unique activities of a Lodge. Accounts …

1-119. Restricted Funds: Defined by Grand Lodge Statutes Sections 1.165 & 16.011. • Funds or other property donated to, raised by, or allocated by a Lodge or related entity to be expended during a specified time or for a designated purpose, or both. Restricted Funds may be “temporary” if the restriction(s) will or could expire over a defined period of time, if the entity holding them is permitted to change or remove the restriction(s), or if the asset could be fully distributed for the defined purpose, or “permanent” if the purpose and time are designated or otherwise considered to be perpetual or the principal is to be held intact. • Use of restricted funds by a Lodge shall be governed by the following provisions: • A Lodge which holds Restricted Funds because of donor designation shall not expend, borrow from, or borrow against any such property for a purpose or during a period other than that designated without authorization of the donor, or pursuant to an order from a court of competent jurisdiction. • A Lodge which holds permanent Restricted Funds because of Lodge designation shall not expend, borrow from, or borrow against any such property for a purpose or during a period other than that designated without the written authorization of the State Sponsor, and two-third (2/3rds) approval by the Members present at a regular Lodge meeting following a minimum ten (10) day notice to all Members. Any such expenditure shall also be in compliance with all State and Federal Laws. • c. Lodges who receive unrestricted donor grants may choose to place these funds in the Restricted Funds ….

9-102. An Audit:An audit is defined as a formal or official examination and verification of accounts. It results in a final report by a Certified Public Accountant (CPA) setting forth his opinion. An audit requires more work and is more costly than a review or compilation. An audit is appropriate for any Lodge, but more so for larger Lodges that have a complex organization or extensive assets. An Audit may be required and/or waived for any Lodge as determined by the State Grand Lodge Sponsor.

9-103. A Review:A review is an engagement performed by a Certified Public Accountant (CPA) which is less expensive than an audit examination. The CPAdetermines whether material modifications exist that do not present financial information in conformity with generally accepted accounting principles. He makes this determination after conducting inquiries of Lodge personnel and performing an analytical review of procedures. A review is appropriate for all but the larger Lodges. A review may be required and/or waived for any Lodge as determined by the State Grand Lodge Sponsor.

9-104. A Compilation: A compilation merely presents, in the form of financial statements, information that is the representation of Lodge management. A compilation is only to be prepared when the Lodge’s Gross Revenues are $500,000 or lower, when the Qualified Independent Accountant determines that an audit or review is not economically practical because of inadequacies in Lodge records and procedures or similar circumstances, or when it is the first report being prepared for a Lodge. The Lodge Auditing and Accounting Committee must, by January 31st, request permission to prepare its Annual Financial Report using a Compilation, for the Lodge fiscal year ending the following March 31st. The application must first be filed with the State Grand Lodge Sponsor and can be obtained from the Lodge’s Grand Lodge Auditing & Accounting Area Committee Member or included as “Exhibit I” in this manual. If approved, the Sponsor will forward on to the Area Committee Member. The Lodge Auditing and Accounting Committee must inform the Lodge that the report is based solely on information provided by the Lodge and will not include an opinion or any other form of assurance that the financial information is verified as completely accurate. A compilation must have the approval of Grand Lodge Sponsor before it can be prepared.

9-105. In-House Annual Financial Report Preparation:Under Section 13.040(j), a Lodge must request permission to prepare its Annual Financial Report using an in-house Qualified Accountant.The Lodge Auditing and Accounting Committee must, by January 31st, request permission to prepare an “In-House” Annual Financial Report, for the Lodge fiscal year ending the following March 31st. The application must first be filed with the State Grand Lodge Sponsor and can be obtained from the Lodge’s Grand Lodge Auditing & Accounting Area Committee Member or included as “Exhibit J” in this manual. If approved the Sponsor will forward on to the Area Committee Member. After a Lodge has annually requested 3 In-House preparations of the Annual Financial Report, then in the fourth year the report must be prepared by a licensed independent accountant.

Exhibit K 45. Qualified Accountant = an individual with any of the following: 1) Bachelor’s Degree in accounting 2) Master’s degrees in accounting 3) Public Accountant / Licensed Public Accountant 4) Certified Internal Auditor 5) A person holding a Certificate in Management Accounting 6) An Enrolled Agent

Potential New Financial Reporting System • Lodges will use their current accounting software • Will be used to produce required reporting to State Sponsor, SDGER, Grand Lodge Area A&A Committeeman, District Auditor, etc. • Cost – 1st Year (initial setup) $360 per lodge. 2nd year and on $120 per year per lodge. • Potential to replace the AFR and associated costs. • Proof of Concept - Phase 1 • Starting now and running through June 30th • 10 lodges to enter data monthly

Volunteers Needed • Initial Data • Lodge Name, Number and District • Current Lodge Chart of Accounts Number and Description (Mapping to the standardized Elks Chart of Accounts if they currently do not comply) • Current Year Lodge Budget detailed by Chart of Account Number and month (annual if month is not available) • Prior Year and Current Year Actual by Chart of Account number by month. • Monthly Data through June 2019 • Up or Down recommendation to Grand Lodge