Download

1 / 24

240 likes | 408 Views

Life Cycle Cost Analysis. Virginia Concrete Conference March 6-7, 2014. Luis Rodriguez, P.E. Federal Highway Administration. Presentation Outline. Life Cycle Cost Analysis Definition LCCA Five Steps Process Current Issues Resources / Reference. Life-Cycle Cost Analysis Definition.

E N D

Life Cycle Cost Analysis Virginia Concrete Conference March 6-7, 2014 Luis Rodriguez, P.E. Federal Highway Administration

Presentation Outline • Life Cycle Cost Analysis Definition • LCCA Five Steps Process • Current Issues • Resources / Reference

Life-Cycle Cost Analysis Definition • A process for evaluating the total economic worth of a usable project segment by analyzing initial costs and discounted future costs, such as maintenance, user, reconstruction, rehabilitation, restoring, and resurfacing costs, over the life of the project segment. Source: Transportation Equity Act for the 21st Century

LCCA Overview Ananalytical tool to provide a cost comparison between two or morecompeting design alternatives producing equivalent benefits forthe projectbeing analyzed.

The LCCA Process • Step 1: Establish alternatives • Step 2: Determine timing of required activities • Step 3: Estimate agency and user costs • Step 4: Compute life-cycle costs • Step 5: Analyze the results

Step 1: Establish Alternatives • Activities to ensure performance • Initial construction or rehabilitation activity • Future rehabilitation and preservation activities

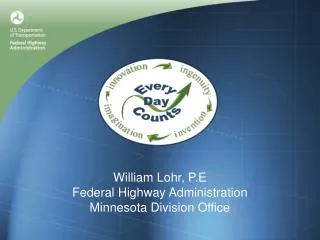

Time Initial Activity Activity One Activity Two Step 2: Determine Activity Timing Serviceability Terminal Serviceability Index Service Life Analysis Period Long enough to capture differences between alternatives When will the future preservation and countermeasure costs be incurred?

Step 3: Estimate Agency and User Costs • Include cost elements that are different between alternatives • Exclude cost elements that are the same between alternatives • Agency overhead costs • Real estate acquisitions • Normal operations user costs

Step 3:Estimate Agency and User Costs • Approach fundamentals • Compare demand and capacity under normal operations and work zone conditions • Determine how traffic is impacted • Convert traffic impacts into costs

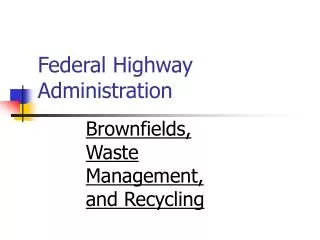

Cash Flow Diagram Initial Activity Rehab 1 $ Preservation Activities Agency Costs Salvage or Remaining Value Time Initial Activity Work Zone Rehab 1 Work Zone Preservation Work Zones $ User Costs Time

Step 4: Calculate NPV of Life-cycle Costs N 1 Σ Net Present Value = of Costs (Costk)x (1 + d)nk k = 0 Present Value Factor Costk= cost of activity N = length of analysis period d = discount rate nk = year of expenditure

Step 5: Analyze the Results • How do agency costs compare? • How do user costs compare? • Can trade-offs be made?

Current Issues • MAP 21 and LCCA • GAO Report: LCCA – Pavement Selection • LCCA and Alternative Bidding

MAP-21 to asset management? Each State is required to develop a risk-based asset management plan for the National Highway System (NHS) to improve or preserve the condition of the assets and the performance of the system. (23 U.S.C. 119(e)(1), MAP-21 § 1106)

Highway Asset Management Plan Plan Contents • pavement and bridge inventory and conditions on the NHS • objectives and measures • performance gap identification • lifecycle cost and risk management analysis • a financial plan • investment strategies

GAO and Next Steps • Define Program Characteristics • Obtain Data • Verify what was used was correct • Document the Estimate • Present Estimate for approval • Update the Estimate

FHWA Program Performance Management Alternate Bidding • What is the FHWA position on alternate bidding for pavement type selection? FHWA considers alternate pavement type bidding a suitable approach for determining pavement type when engineering and economic analysis does not indicate a clear choice between different pavement designs.

Consideration of Challenges LCCA Consistency Flexibility

LCCA Resources LCCA Case Study User Manual LCCA Primer LCCA Technical Bulletin http://www.fhwa.dot.gov/infrastructure/asstmgmt/lcca.htm

RealCost LCCA Software • Microsoft Excel based application – existing user expertise and user customizable • User interface – separates inputs from analysis methodology • Offers both Deterministic and Probabilistic Analysis • Available free of charge, regular enhancements and technical assistance from FHWA

Reference • FHWA LCCA Internet Site: http://www.fhwa.dot.gov/infrastructure/asstmgmt/lcca.cfm • GAO Report : LCCA-Pavement Selection http://www.gao.gov/products/GAO-13-544 • FHWA TA on Use of Alternative Bidding for Pavement Type Selection: http://www.fhwa.dot.gov/pavement/t504039.cfm

Luis Rodriguez, P.E. Federal Highway Administration luis.rodriguez@dot.gov 404-562-3681 http://www.fhwa.dot.gov/resourcecenter/ Thank You