Download

1 / 36

360 likes | 1.04k Views

Chapter 3 Preparation of Financial Statements. By the end of this chapter, you should be able to: understand the structure and content of published financial statements; explain the nature of the items within published financial statements;

E N D

By the end of this chapter, you should be able to: • understand the structure and content of published financial statements; • explain the nature of the items within published financial statements; • prepare the main primary statements that are required in published financial statements; • comment critically on the information included in published financial statements.

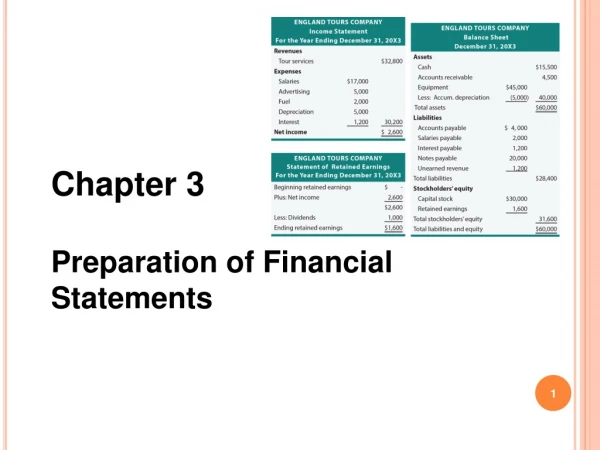

Components of Financial Statements (a) The Balance sheet Assets Liabilities, and Equity (b) The Income Statement Revenue (income) Expenses

Preparing an income statement The steps are: • Prepare the trial balance • Identify year-end adjustments • Calculate year-end adjustments • Prepare an internal income statement.

Identify and calculate year-end adjustments • At year-end there will be some transactions that affect both the current year, and the coming year. These need to be adjusted so that the amounts applied to the current year’s activities are correct. • Expenses accrued – expenses have been incurred, but have not been paid eg. Wages accrued • Prepaid expenses – expense is paid before it is incurred eg. Prepaid rent • Depreciation – the annual expense is normally calculated and applied at the end of each year • Accruals and prepayments are usually apportioned evenly over the period (pro rata basis)

IAS 1 allows a company to choose between two formats for detailing income and expenses. Format 1:Vertical with costs analysed according to function, cost of sales, distribution costs, administration expenses and other expenses;

IAS 1 allows a company to choose between two formats for detailing income and expenses. Format 2 Vertical with costs analysed according to nature, raw materials, employee benefits expenses, operating expenses and depreciation, after operating profit the rest is the same as format 1.

Note: Many companies use format 1, if they do then the details disclosed by format 2 must be provided in the Notes to the Financial Statements

Classification of operating expenses and other income by function format 1 Cost of sales • Direct materials; direct labour; other external charges that comprise production costs from external sources. • Overheads: variable and fixed production overheads. • Depreciation and amortisation: depreciation of non-current assets used in production and impairment expense; • Adjustments: capitalisation of own work as a non-current asset.

Classification of operating expenses and other income by function Distribution costs Costs incurred after production of finished goods and up to and including transfer of the goods to the customer. • Warehousing costs such as rent, rates and wages • Promotion costs such as advertising • Selling costs such as sales staff salaries and commissions and cost of rent, etc. on showrooms • Transport costs, such as gross wages and pension contributions of transport staff, vehicle costs such as running costs, maintenance and depreciation.

Classification of operating expenses and other income by function Administrative expenses Costs of running the business that have not been classified as either cost of sales or distribution costs. • Administration salaries • Property costs, rent and rates • Bad debts • Professional fees, audit fees, directors’ fees.

Classification of operating expenses and other income by function Other operating income or expense Derived from ordinary activities of the business that have not been included. • Income from intangible assets such as royalties • Income from employees such as from canteen, repayments to use intangible assets like licences.

Statement of comprehensive income Figure 3.4 Statement of comprehensive income Figure 3.4 Statement of c

Statement of comprehensive income (Continued) Other comprehensive income Gains and losses previously recognised directly in equity and presented in the statement of changes in equity. Unrealised gains/losses that cannot be claimed as part of net profit from operations For example: From the revaluation of non-current assets and from other items relating to Financial Instruments and Employee Benefits.

Statement of comprehensive income (Continued) Figure 3.4 Statement of comprehensive income (Continued)

Information disclosed by way of note Accounting policies Details on the accounting policies applied – such as using historical cost, basis of inventory valuation, depreciation method etc, and details of certain items that have been charged in arriving at Operating Profit. • Showing the makeup of individual liabilities and assets • Sensitive items such as auditors’ remuneration • Subject to judgement - depreciation • Exceptional items – unusually high/low, or occur infrequently.

Current tax Current tax is: • An estimated figure • Treated as an expense in the Statement of Income • A current liability in the Balance Sheet • The actual tax expense for a year might be higher or lower than the company’s estimate which leads to under- or over-provisions being made. • Deferred tax • Tax may be deferred when the percentage allowed by the tax authorities for depreciation differs from the rate charged as depreciation by the company • We look at accounting for tax next week

The statement of financial position(Balance Sheet) IAS 1 specifies which items are to be included on the face of the balance sheet, for example • Property, plant and equipment • Inventories • Trade and other payables. It does not prescribe the order and presentation that is to be followed Generally, it is appropriate to split items into current (less than 12 months) and non-current (more than 12 months) lives.

Notes to Balance Sheet • Giving greater detail of the make-up of items that appear in the statement of financial position • Setting out accounting policies, and methods used to value assets • Providing additional information to assist predicting future cash flows • Giving information of interest to other stakeholders.

The accounting rules for asset valuation • Property, plant and equipment Either historical cost or market value depending upon accounting policy chosen from IAS 16 • Financial assets Certain classes of financial asset are required to be recognised at fair value • Inventory It is included at the lower of cost and net realisable value. 4. Provision is an amount retained from profit. • provides for a loss or liability that are likely to be incurred but the amount is uncertain. • is shown in statement of financial position after creditors are deducted from assets, e.g. Bad debt provision.

Statement of changes in equity The statement of changes in equity will show the following items: Total comprehensive income and expense for the period, showing separately the total amounts attributable to equity holders of the parent and to non controlling interests For each component of equity, the effects of changes in accounting policies and corrections of errors recognised in accordance with IAS 8 The amounts of transactions with equity holders in their capacity as equity holders, showing contributions by and distributions to equity holders separately.(dividends)

Statement of changes in equity Transactions with equity holders in their capacity as equity holders Other comprehensive income After-tax profit from ordinary activities Figure 3.7 Statement of changes in equity for the year ended 31 December 20X1

Other items appearing in a statement of changes in equity Other items may include: • Prior period adjustments • Share issues • Transfers from revaluation reserve.

Illustration Figure 3.8 Statement of changes in equity for year ended 31 October 20X1

Reserve • is a realised or unrealised gain which either has legally or at the company’s discretion, not been distributed as dividends, i.e. • is retained in the business, e.g. retained profits, share premium, revaluation reserve etc. • is shown in the statement of financial position after share capital.

Has prescribing the formats meant that identical transactions are reported identically? No because Differences still arise on • How inventory is valued • The choice of depreciation policy • Management attitudes • The capability of the accounting system.

% difference in gross profit Figure 3.13 Effect of physical inventory flow assumptions on the percentage gross profit

What does an investor need in addition to the financial statements to make decisions? • More quantitative information in the accounts (discussed in Chapter 4) including: • Segmental analysis • The impact of changes on the operation, for example a breakdown of turnover, costs and profits for both new and discontinued operations • The existence of related parties. • More qualitative narrative information, including: • Mandatory disclosures • Chairman’s report • Management Commentary • Directors’ report • Best practice disclosures: Operating and Financial Review • Business Review in the Directors’ report.

Mandatory disclosures • The write-down of assets to realisable value or recoverable amount • The restructuring of activities of the enterprise, and the reversal of provisions for restructuring • Disposals of items of property, plant and equipment • Disposals of long-term investments.

Other Reports • Chairman’s report • Management commentary • Directors’ report • Operating & Financial Review (OFR)* • Key Performance Indicators* • Business review – social, environmental, sustainability • * Usually included in these other reports

What is meant by a fair view?IAS 1 requirements • Select and apply accounting policies in accordance with IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors • Present information, including accounting policies, in a manner that provides relevant, reliable, comparable and understandable information • Provide additional disclosures when compliance with the specific requirements in IFRSs is not enough.

True and fair view – legal opinion • Accurate within acceptable limits • Differences over acceptable limits • Room for differences over method to adopt • Cost effectiveness • Sufficient in quantity and quality to satisfy reasonable expectations. • Complying with the accounting standards is not enough – must also consider whether the standard(s) is/are appropriate in the particular situation.

End of Chapter Review Questions Numbers 1, 2, and 4-7 are relevant for this course

References Elliott, Barry, Elliott Jamie, Financial Accounting and Reporting 18th Edition chapter 3 Elliott, Barry, Financial Accounting and Reporting 15th Edition chapter 2