Download

1 / 4

0 likes | 4 Views

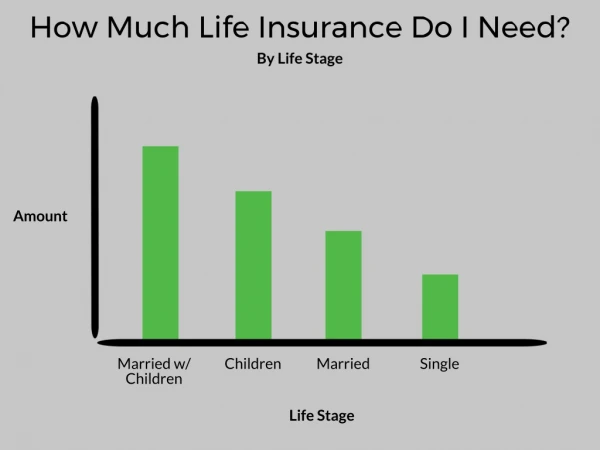

Wondering how much umbrella coverage do I need? Umbrella insurance offers extra liability protection beyond home and auto policies, safeguarding your assets from costly lawsuits. This guide helps you assess your net worth, risk exposure, and current coverage limits to determine the right amountu2014typically $1M to $5M or more. Learn how lifestyle factors, future earnings, and affordable premiums influence your decision, and get practical tips to choose the right coverage for true peace of mind.

E N D