Download

1 / 6

0 likes | 3 Views

f you have served in the military or are a surviving spouse, you may have a great home loan benefit.<br><br>This benefit is called the VA loan, and many people do not fully understand it. But what exactly is it, and why do so many veterans use it to buy a home?<br><br>Letu2019s understand everything about VA Loans.

E N D

VA Loans Explained: Eligibility and Benefits If you have served in the military or are a surviving spouse, you may have a great home loan benefit. This benefit is called the VA loan, and many people do not fully understand it. But what exactly is it, and why do so many veterans use it to buy a home? Let’s understand everything about VA Loans. What is a VA Loan? A VA loan is a home loan from a special program by the U.S. Department of Veterans Affairs. It helps veterans, active-duty service members, and eligible surviving spouses buy a home. They can often do this with no down payment, no private mortgage insurance, and low interest rates. It’s different from other loans because the government promises to repay part of the loan if the borrower can’t. That’s why lenders are more flexible with VA loans. It’s one of the biggest military housing benefits available today.

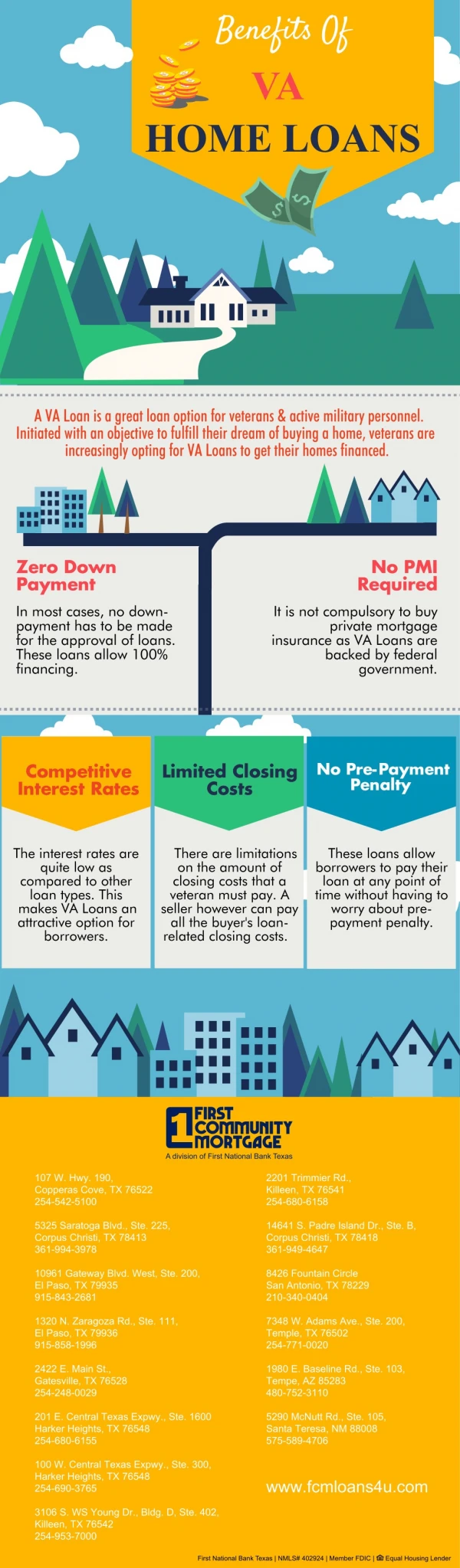

Who is Eligible for a VA Loan? Let’s find out if you qualify. You can apply for a VA loan if you are: ● An active-duty service member (90 continuous days of service) ● A veteran who served during wartime or peacetime ● A National Guard or Reserve member (with at least 6 years of service or called to active duty) ● A surviving spouse of a service member who died in the line of duty What you need: ● A Certificate of Eligibility (COE) ● Proof of service (like your DD-214 form) This is called VA loan eligibility, and it’s the first step to getting started! Top Benefits of a VA Loan Here’s why so many veterans choose VA loans: 1. Zero Down Payment: You don’t need to save up for a down payment. This is a big relief! 2. No PMI: Other loans charge private mortgage insurance, but VA loans don’t. 3. Lower Interest Rates: VA loans usually offer lower rates than regular loans. 4. Flexible Credit Rules: Even if your credit isn’t perfect, you can still qualify. 5. Limited Closing Costs: The VA limits what you can be charged. 6. Funding Fee: There is a one-time VA funding fee, but many people are exempt. With these VA loan benefits, you get to save thousands of dollars and still get a good home loan. VA Loan Process – Step-by-Step Guide Here’s how to get your VA home loan: 1. Check Your Eligibility First things first—make sure you qualify for a VA loan. VA loans are mainly for: ● Veterans who served enough active duty ● Active-duty service members ● Members of the National Guard or Reserves

● Surviving spouses of service members Each group has different service requirements. You can check the exact rules on the VA’s website or ask a lender to help. If you’ve served honorably, there’s a good chance you’re eligible. 2. Get Your Certificate of Eligibility (COE) This is your official proof that you're allowed to get a VA loan. It shows the lender you meet the service requirements. You can get your COE: ● Online through the VA’s website ● Through your lender (they can request it for you) ● Or by mailing in a form You only need to get your COE once—after that, it stays on file. 3. Find a VA-Approved Lender Not every lender can issue VA loans. Look for one that’s VA-approved—this means they understand the VA loan process and can guide you smoothly. Good lenders will help: ● Explain your loan options ● Estimate how much you can borrow ● Make sure you're ready for the next steps Choose someone you trust and who communicates clearly. 4. Get Pre-Approved Getting pre-approved means the lender looks at your credit score, income, and other financial details to see how much you can afford. Why it helps: ● It shows sellers you’re serious ● You’ll know your budget

● It speeds things up when you’re ready to make an offer Tip: Don’t confuse this with pre-qualification. Pre-approval is stronger and more official. 5. Find Your Dream Home Now the fun part—house hunting! Work with a real estate agent who understands VA loans. They’ll help you find homes that: ● Meet VA property standards ● Fit your price range ● Match your lifestyle Once you find the right one, you’ll make an offer. If accepted, your lender moves forward with the loan. 6. VA Appraisal + Underwriting Before the loan is approved, two big steps happen: VA Appraisal The VA sends someone to check the home’s value and condition. This is to make sure: ● The price is fair ● The home is safe, sound, and move-in ready Underwriting The lender reviews everything—your finances, the appraisal, and loan documents. They check: ● You can afford the loan ● The home meets all VA guidelines If all looks good, you get the green light to close!

7. Close the Loan and Move In At closing, you sign all the final paperwork. Your lender sends the money to pay for the home, and the keys are yours! You may pay some closing costs, but they’re usually lower with VA loans. Now you can move in and enjoy your new home—thanks to your service and the VA loan benefit. It’s easy when you have a VA loan specialist to guide you. VA Loan vs. Conventional Loan vs. FHA Loan Let’s compare these three: Feature VA Loan Conventional Loan FHA Loan Down Payment $0 3%-20% 3.5% PMI Required? No Yes (if < 20% down Yes Credit Score Flexibility More Flexible Strict Medium Government Backed? Yes (VA) No Yes (FHA) Is a VA loan better than a conventional loan? In most cases, yes! Especially for veterans who want to save money. Common Myths About VA Loans Let’s bust some myths: ● You can only use it once – Not true! You can use it many times. ● VA loans are slow – Nope! They can close just as fast as regular loans. ● Only first-time buyers can use it – Wrong again. VA loans are for all eligible veterans. These VA loan requirements are much simpler than most people think. Tips to Maximize VA Loan Benefits 1. Compare Lenders: Different lenders offer different rates. 2. Know Your Funding Fee: Some may not have to pay it at all! 3. Ask About Reuse: You can use your VA loan more than once. 4. Use All Your Benefits: Lower monthly payments = more savings!

Looking for expert help? Try VA Loan Assistance to make the most of your benefits. Conclusion VA loans are one of the best tools for veterans and active military members who want to buy a home. They make it easier to afford a house by removing the need for a down payment, PMI, or perfect credit. If you think you might be eligible, now is the time to take action. Ready to discover your VA loan benefits? Get Pre-Approved VA Loan today and move one step closer to homeownership!