Download

1 / 6

0 likes | 5 Views

If you're planning to buy a home, an FHA loan could be a great option. Designed to assist individualsu2014particularly first-time buyers and those with past credit challengesu2014FHA loans make homeownership more accessible.

E N D

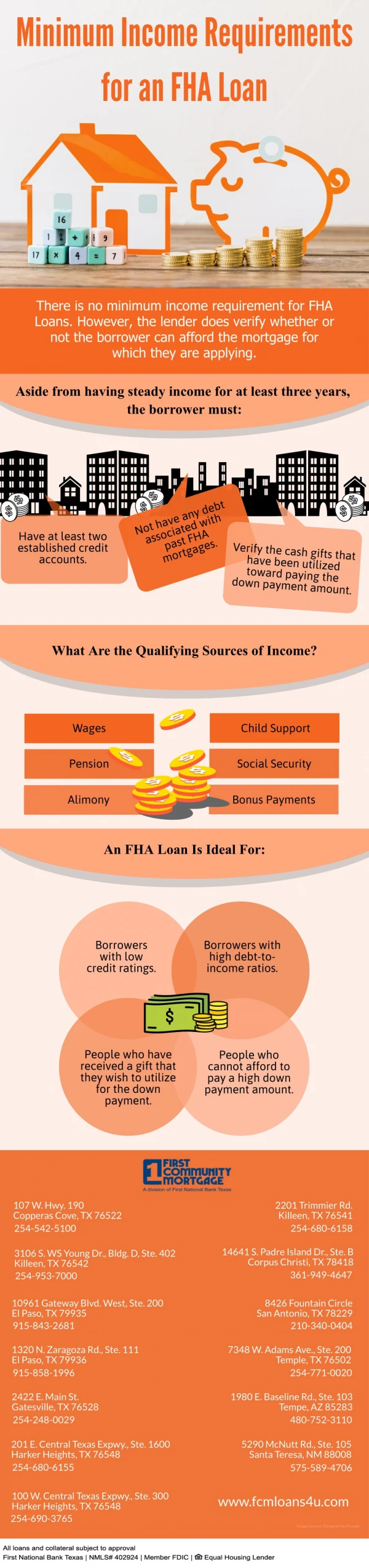

FHA Loan Requirements 2025: Qualifying Guidelines If you're planning to buy a home, an FHA loan could be a great option. Designed to assist individuals—particularly first-time buyers and those with past credit challenges—FHA loans make homeownership more accessible. Compared to conventional mortgages, FHA loans have fewer restrictions, allowing individuals with lower credit scores or smaller down payments to qualify more easily. Below we cover the requirements, loan limits, and how you can use an FHA mortgage to become a homeowner. Understanding FHA Loan Requirements FHA loans are backed by the Federal Housing Administration (FHA), making the loans more attainable for borrowers. But the FHA doesn't make these loans; you must apply through an FHA-approved lender. Since various lenders may have slightly varying requirements, it’s good to be aware of the general eligibility criteria for an FHA home loan. Credit Score Requirements Your credit score is a significant element in your eligibility. Lenders use this score to ascertain your risk level and repayment ability. Generally speaking, the better your credit score, the higher the chances of approval.

FHA loan credit score requirements include: ● 500 to 579: Requires a 10% down payment. ● 580+: Eligible for a 3.5% down payment. Down Payment Requirements A down payment is required to secure a mortgage loan. The FHA mortgage program allows for down payments as low as 3.5%, depending on creditworthiness. Various sources can be used for a down payment, including: Personal Savings: Funds from your bank account. Down Payment Assistance (DPA) Programs: Some state and local programs offer zero-interest loans or grants that don’t require repayment. Gift Funds: Monetary gifts from family or close associates that don’t need to be repaid. Retirement Account Withdrawals: Borrowers can use up to $10,000 from an IRA for a first-time home purchase. Government and Non-Profit Grants: Additional assistance programs may be available for eligible borrowers. Debt-to-Income (DTI) Ratio Limits Your DTI ratio is the percentage of your gross monthly income that you spend paying debts. A lower DTI indicates financial stability and higher repayment ability. FHA loan guidelines generally require: ● Maximum DTI of 43%: Higher DTIs may be considered if compensating factors, such as higher income, exist. Example DTI Calculation: ● Gross Monthly Income: $5,000 ● Monthly Debt Payments: $3,000 ● DTI Ratio: 60% ($3,000 ÷ $5,000)

Employment and Income Requirements To qualify for an FHA loan, a person must have stable employment and a stable income. Lenders typically require at least two years of continuous employment. Commonly accepted forms of income verification include: ● Recent Bank Statements ● Pay Stubs from the Last 30 Days ● W-2 Forms ● Two Years of Federal Tax Returns Mortgage Insurance Premium (MIP) Requirements FHA loans have Mortgage Insurance Premiums (MIP) to guarantee lenders. MIP increases the cost of borrowing but allows more lenient credit and down payment requirements. MIP consists of: Upfront MIP: Paid at closing; can be financed into the loan amount. Annual or Monthly MIP: Included in monthly mortgage payments. Regardless of credit score, all FHA borrowers must pay MIP. A higher MIP may apply if the down payment is less than 5%. FHA Loan Property Requirements In order to qualify for an FHA loan, a home must meet Department of Housing and Urban Development (HUD) standards for safety, durability, and livability. Eligible property types include: ● Single-family homes ● Multi-unit properties ● Townhouses ● Condominiums ● Some manufactured homes Additionally, the home must pass an FHA appraisal to ensure compliance with building codes.

FHA Loan Limits 2025 FHA loans also feature maximum mortgage limits, which vary by location. The limits for a single-unit property in 2025 range from $524,225 to $1,209,750, based on the county's cost of living. How to Qualify for an FHA Loan Qualifying for an FHA loan involves several steps, similar to applying for other home loans. Below is the step-by-step process: Step 1: Determine if an FHA Loan is Right for You ● Assess your credit score and financial history. ● Evaluate your down payment savings and income. Step 2: Compare FHA-Approved Lenders ● Review lender requirements, DTI limits, and fees. ● Use the HUD lender list search tool to find FHA-approved lenders. Step 3: Gather Required Documents ● Proof of residence (utility bills or rental agreements) ● Social Security Number ● Government-issued ID (driver’s license or passport) ● Employment history verification (past two years) ● Proof of income (pay stubs, tax returns, bank statements) Step 4: Get Pre-Approved ● Pre-approval helps determine loan rates and affordability. ● It strengthens your position as a serious buyer. Step 5: Apply for an FHA Loan ● Complete a formal loan application through your chosen lender. ● Provide additional documentation if required. Pros and Cons of FHA Loans Like any mortgage, FHA loans come with advantages and drawbacks. Pros: ● Lower Down Payment Requirements: As low as 3.5%. ● Easier Credit Score Qualification: More lenient compared to conventional loans. ● Government-Backed Security for Lenders: Increases loan accessibility.

● Ideal for First-Time Buyers: Helps individuals with limited savings. ● Pathway to Homeownership: Provides opportunities to those with past financial challenges. Cons: ● Mandatory Mortgage Insurance (MIP): Adds to monthly and upfront costs. ● Loan Limits: Restrictions on borrowing amounts. ● Property Requirements: Must meet FHA standards. ● Higher Down Payment for Lower Credit Scores: Requires 10% down for scores between 500-579. Frequently Asked Questions (FAQ) 1. What is the minimum credit score for an FHA loan? Your credit score is the most important FHA loan requirement. You must have a credit score of 500–579 (with 10% down) or 580+ (with 3.5% down). 2. Can mortgage insurance be removed from an FHA loan? You might be able to cancel the mortgage insurance that comes with taking an FHA loan. To find out how, call your loan servicer. If your remaining loan balance is less than 78% of the original principal, you should be able to drop MIP. 3. How long does FHA loan approval take? Approval times vary but typically take between 3 to 6 weeks, depending on lender processing and documentation requirements. 4. What types of properties qualify for FHA loans? If the property meets current safety and livability standards, you can use an FHA loan on your primary residence. Single-family dwellings, multi-family dwellings, some mobile homes, and condominiums are usually qualifying properties. Final Thoughts Home buyers who have minimal credit and a small down payment can benefit from the advantages FHA loans offer. These loans assist numerous prospective buyers because of the liberal credentialing and guarantee backing by the government, which makes homeownership a reality for just about anyone. Make sure you shop around ahead of time to get the best FHA loan terms and that you are aware of all of the rules ahead of time before applying.

Meta Title (under 60 characters): FHA Loan Requirements 2025 | Eligibility Guide Meta Description (under 160 characters): Discover the latest FHA loan requirements for 2025. Learn how to qualify, credit score, down payment, and income criteria in this quick guide. SEO-Friendly URL Structure: /fha-loan-requirements