Download

1 / 12

130 likes | 218 Views

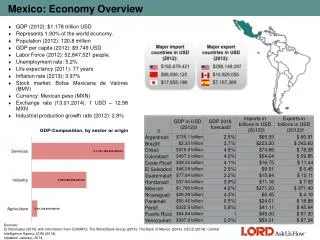

2005 Mexico Economy Outlook. www.cide.edu/analisiseconomico. www.cide.edu/analisiseconomico. ECONOMÃA. Economy Growth.

E N D

2005 Mexico Economy Outlook www.cide.edu/analisiseconomico

www.cide.edu/analisiseconomico ECONOMÍA Economy Growth Last year, Mexico registered his better economy growth in four years, leaving behind the recession that began in the year 2001. The economy grew 4.4% supported in the strong growth of his service sector up 4.6%, and a turn around of the industrial sector up 3.9%; after three years of negative growth. The US sustained recovery, especially on his manufacturing sector, was the main cause of the recovery in Mexican industrial sector; from the demand side economy was sustained by a strong growth on private consumption, investment and real exports.

www.cide.edu/analisiseconomico ECONOMÍA Economy Growth We expect the economy to decelerate slightly this year to a 4% growth based on strong momentum of consumption and investment demand, but restrained by negative net exports growth. We calculate this year private consumption to add 2.95% and fixed investment 1.3% to GDP growth. Industrial sector is expected to grow 3.8% and services 4%. At year-end as the economy accumulates two years of growth, the output gap will close. For next year, we forecast GDP growth to fall to 3.7%, similar to our estimation of Mexico GDP potential growth.

www.cide.edu/analisiseconomico ECONOMÍA

www.cide.edu/analisiseconomico ECONOMÍA

www.cide.edu/analisiseconomico ECONOMÍA CPI Inflation Despite a positive output gap CPI inflation accelerated last year to 5.2%, from 4% registered on 2003, significantly above central bank target of 3% ± 1%. Core inflation was 3.8% vs. 3.7% in the year 2003. Inflation was pushed higher by: 1) greater than expected agricultural prices, 2) Increasing business cost triggered by high international price of commodities, and 3) Higher government controlled prices of energy. As the output gap narrowed, businesses have gradually translated cost pressures to consumers. We expect CPI inflation rate to fall to 3.9% this year while core inflation remains unchanged at 3.8%. The inflation outlook will be favored by: a) a fall in agricultural prices that has already taken place on 1Q, b) Government intentions to keep public sector prices in line with the central bank target, and 3) a restricted monetary policy already adopted to moderate business cost translation to consumers and wages negotiations. We estimate CPI and core inflation rates at 3.8% and 3.6% next year.

www.cide.edu/analisiseconomico ECONOMÍA

www.cide.edu/analisiseconomico ECONOMÍA Monetary Conditions Since 1Q04 the central bank began its ongoing cycle of monetary restrictions, policy that has coordinated since June04 with the Fed own cycle of monetary restrictions in the US. Banxico has increased his “corto” in twelve occasions; the last one was on March 23. As a result of this, monetary conditions have turned quite restrictive as real USDMXN has fallen, expected real interest rates hiked and domestic-yield curve flattened. Until now, due to the lag with which monetary restrictions affects aggregate demand, the restricted monetary policy has had a negligible effect on economy growth; but beginning on 2H05 they will weight in the economy growth deceleration. We consider the actual stance of monetary policy restricted enough, and expect Banxico to look on 2H05 for an opportunity to decouple his monetary policy from the FED, so monetary conditions will loosen as short-term interest rates stabilize and USDMXN rebounds. We expect USDMXN to close this year at 11.82 vs. his 1Q close of 11.17.

www.cide.edu/analisiseconomico ECONOMÍA

www.cide.edu/analisiseconomico ECONOMÍA

www.cide.edu/analisiseconomico ECONOMÍA

www.cide.edu/analisiseconomico ECONOMÍA