Download

1 / 42

430 likes | 563 Views

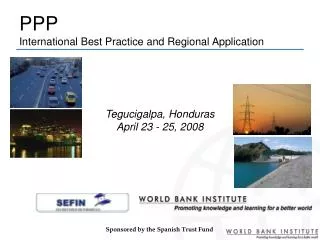

PPP International Best Practice and Regional Application. Tegucigalpa, Honduras April 23 - 25, 2008. Sponsored by the Spanish Trust Fund. Case Study Session 5.2. Water & Sanitation. David Stiggers, Independent PPP Specialist. Session 5.2. Day 2 – Session 6 Readiness of Government.

E N D

PPP International Best Practice and Regional Application Tegucigalpa, Honduras April 23 - 25, 2008 Sponsored by the Spanish Trust Fund

Case Study Session 5.2 Water & Sanitation David Stiggers, Independent PPP Specialist

Session 5.2 Day 2 – Session 6 Readiness of Government Day 1: Session 1.1 Overview of PPP Private Sector View Day 1:Session 1.2 Challenges: Latin America Upstream Policy Readiness of Government Capacity Building For PPP Day 1- Session 5 Case Study: Water & Sanitation Day 1:Session 1.3 Considering Private Participation PPP Approach Day 2:Session 5 Case Studies: (1)Highways (2)Water & Sanitation (3) Ports Day 1:Session 2.1 Planning the Process Day 1:Session 3 Case Study: Transmission Day 2 :Session 4.2 Selecting an Operator Day 1:Session 2.3 Involving Stakeholders Day 2 :Session 4.1 Standards, Tariffs, Subsidy, Financials Day 1:Session 2.2 Regulation & Institutions

Case Study: Armenia • Review Existing Management of the Water Sector in Armenia • Look at existing PPP models in Armenia, and their Performance • Consider an existing Management Contract (ending 2009) – with the regional company AWSC - and what to do after the current contract ends.

Armenia • Population 3.1 Million: • 38% Rural : 62% urban • Abundant Water Resource: 98% Groundwater • Infrastructure in poor condition:$1billion to bring back to good condition • Poor Water & Sanitation Services • 87% Urban connected but only 7 hours/day • 32% Rural connected but only 2% in good condition • 540 villages not served by any water provider

Armenia • THE PROBLEM • Poor quality of water and poor water and sanitation services • Limited Access to drinking water • Deterioration in Public Health • The socially vulnerable groups are the most affected • Population 3.1 Million: • 38% Rural : 62% urban • Abundant Water Resource: 98% Groundwater • Infrastructure in poor condition:$1billion to bring back to good condition • Poor Water & Sanitation Services • 87% Urban connected but only 7 hours/day • 32% Rural connected but only 2% in good condition • 540 villages not served by any water provider

Shirak WSC Municipal/State CJSC 149,600 popn. Yerevan Djur (Veolia) Lease 1m. popn. Lori WSC Municipal/State CJSC 118,500 popn. Nor Akunq 540 Municipal/State CJSC Villages 59,440 popn. Review Management Modes Municipal Companies (Veolia) (Veolia) (Veolia) (Veolia) Lease Lease Lease Lease Lease 1m. popn. 1m. popn. 1m. popn. 1m. popn. AWSC Management Management Management Management Management (Saur) (Saur) (Saur) (Saur) (Saur) Contract Contract Contract Contract Contract 620,000 popn 620,000 popn 620,000 popn 620,000 popn 620,000 popn . . . . . . ‘ ‘ ‘ Management Contract ‘ ‘ ‘ Villages • Considered: • Institutional • Regulatory • Contractual

Management Forms: • Lease: • Yerevan Djur( Capital city ) 1m. popn • Management Contract : • AWSC: National Management Contract (Regional towns and villages) 620,000 popn • 3 Municipal Companies • Shirak (149,600); Lori (118,500); Nor Akunq (59,440) • 540 Village associations

Analysing Key Areas of Responsibility “We looked at three key areas of responsibility for utility management, and then the tasks for each area…………..” MANAGEMENT OPERATIONS & MAINTENANCE INVESTMENT & FINANCE • Direct staff • Set human resource Policy • Establish or improve business processes • Manage inventory • Maintain assets • Commercial responsibilities (e.g. billing & collection) • Issue demand and capacity forecasts • Arrange finance • Prepare technical designs • Construct assets

Responsibilitiesin the main PPP models “……and here we can see which Responsibilities are dealt with under each of the three typical PPP models” Concession & Divestiture Affermage & Lease Management Contract MANAGEMENT OPERATIONS & MAINTENANCE INVESTMENT & FINANCE • Manage inventory • Maintain assets • Commercial responsibilities (e.g. billing & collection) • Issue demand and capacity forecasts • Arrange finance • Prepare technical designs • Construct assets • Direct staff • Set human resource Policy • Establish or improve business processes

Concession Risks & Responsibilities:Armenia Full Ownership (e.g. State or Private) All Risks – with Asset liability Investment Risk Lease Collection Risk Management Contract Operating Risk Management & Operations Commercial: Revenues / Profit Investment & Finance Asset Liability Key PPP Arrangement Risks

Concession not viable for AWSC • For the foreseeable future AWSC will not have sufficient income to meet capital costs and depreciation, as well as operating costs. • International water operators do not currently have the desire/ability to make the necessary investments and finance the Concession model. • We can look at some other PPP form that will allow improvement of AWSC towards Concession in the long term, if investment is still an issue at that time and operators view of concession risks improves. “Concession is not viable under current circumstances”

Some of the ‘players’ • SWCS: The state nominated company who manages sector policy, PPP contracts and some asset ownership • PRCS: the State Regulator: Controls Tariff • The Private Operators: Veolia, Saur • The 3 Municipal Companies • Independent auditor: Technical and Financial audits

Private Operator Veolia “The Bidder” Contractual Payments Management & Resources Use of Facilities Private Service Provider Yerevan Djur cjsc “The Lessee” SWCS “The Lessor” State Lease Fee Independent Auditors Service Tariff Regulator PSRC Customers Lease Contract: Yerevan

Lease: Yerevan • Originally a 5 year Management Contract • Positive experience with the MC (data collection, general improvements) • Since 1 year ago (after bid) a Lease, carried out by Private Operator (Veolia) • Contract terms well established (Model for AWSC) • Regulation clearly defined e.g. tariff reviews • Performance improving as plan • Management of a Comprehensive Capital Works Plan (Govt. Finance)

Private operator SAUR Independent Auditors Payments Management SWCS Service Provider AWSC AWSC Board Tariffs Services Regulator PSRC Customers Management Contract: AWSC

Management Contract: AWSC (1) • AWSC is a State company, managed by SAUR under a 4 year Management Contract (MC) won in open tender. • Good planned results, with improvements designed to lead to next PPP arrangement • Operator responsible for managing all operations, financial matters & personnel • Base Fee + Incentive payment against 4 Performance Indicators

Management Contract: AWSC (2) • SAUR bring management expertise through expatriate & local managers. • AWSC/Government finance a capital works program. • SAUR manage the construction of new and rehab works that affect their operations. • AWSC bears risk of Tariff levels, collection and service delivery risks. Tariff levels do not affect SAUR’s fees.

SWCS State Shareholder (51%) Regional Shareholders (49%) Consultancy services Nor Akunq Board Water Company Nor Akunq cjsc Tariff Service Regulator PSRC Customers The Municipal Companies

Municipal Companies • Municipal joint stock companies were formed, part owned by the State. • Managers are helped to develop institutional & management improvements with help of external advisers • Some investment and technical assistance provided under KfW funding • Emergency works were a success, but long term operational improvement has yet to be seen.

Look at Performance Established Base Data • Technical Performance • Financial Used existing performance • Yerevan 10 year Lease Contract 2006 - 2016: • AWSC 4 year Management Contract 2004 - 2008: • Regional Companies. Made forward performance projections (AWSC only)

Payment Performance Indicators 18 Performance Indicators are used for Management Purposes, of which 4 are linked to Payment: • Continuity of supply (Average hours/day) • % subscribers metered • Bacteriological drinking water safety (% samples) • Company Working Ratio (Costs/Revenue)

AWSC - Performance Data & Projections 2004 - 2010 (current MC Service Area)1 (in million AMD)

Lease Costs (1) - Operational • Personnel Costs: 40% of cost; 22% reduction in workforce (5.2/1000 connections) in 4 years • Electricity Costs: 30% of cost ; assume 15% reduction in 4 years, but requires capital investment • Other Expenses: Similar to today, but increased throughput achieved under lease • Sewage Plant Operation: Similar to today • Management overheads: Current expatriate staff costs reduced by 15 % under lease

Lease Costs (2) - Financial • Operating Capital: $1m loan made available to Operator at preferential rate (5%) • Operator’s Retained Profit: This will only be determined at bid, but estimate made • Debt/Capital Investment: Planned Investment program determined, but funded by Government • State Lease Fee: Set at level to cover Govt. debt repayments • Depreciation: Taken as national accounting standard

SUBSIDY ?? Cost Recovery and Tariff “To be viable: Tariffs + Subsidies = Total Cost of Service” Depreciation: Cost of replacement Cost of Investment Service Coverage Service Quality INCENTIVES TARIFF INCOME COST OF SERVICE

Total Costs ($) Tariff Rate ($/cubic meter) = Total Billed Consumption (cubic meter) My Simple Tariff Formula!!!

Tariff Level: Starting point • Current Tariffs are seen as being low • They are inadequate to recover costs • Tariffs have to be within affordability limits (approx 3% of average household income) • A ‘politically accepted. initial tariff is seen to be around 100 – 110 AMD/m3 • Tariff can be increased as service improves Note: $1 US = 309 Armenian Dram

AWSC Tariff Scenarios Adding the 3 Towns increases Basic Tariff by approx 6%

Good experience from Yerevan model Likely Bidder interest MC well prepared Data availability Operational Improvement Financial improvement No subsidy Reasonable Tariff Actual Tariff increase can be phased It takes time to implement a PPP bid, so immediate start needed on preparation Should Lease be negotiated with the existing Operator or out to Open Tender? What to do about Depreciation? Establish the Lease?

Brings economies of scale (size similar to Yerevan) Smooths Tariffs Size more attractive to manage, and more interest in larger urban element Private Operator expected to make immediate efficiencies Data not so reliable Asset ownership issues need resolving Additional management and reform costs to integrate 3 Towns Break even Tariff comparable, but Lori & Shirak have to increase a lot from existing Should we include 3 Towns?

Suggestions for Lease Contract • Detailed contract comments were proposed to be incorporated on using Yerevan contract as a model: • Tidy up customer contracts/municipal concessions/supply & service contract relationships • Special initial emphasis and funding for water balance issues to be included in Operator’s obligations (e.g. small works issues, customer cadastre, UFW reduction plan) • Regularize ways of dealing with the poor and disadvantaged customers (e.g. sort out voucher or other arrangement) • Resolve nonpayment issues related to Operator’s powers and sanctions. • Independent Auditor; • Penalties; • Ownership & Licence Issues; • Role of PMU; • Excess profits • Employment conditions: • Training; • Lease Payments; • Change of Scope; • Economic Equilibrium; • Extension of Contract: • Management of Capital Works; • Hand Back Provisions

Recommendations • Follow on MC with a Lease • Decide timing: • On balance, if ready to fast track, go straight to Lease: • One time Tariff change • Keeps up momentum • Can make other changes at the same time • Address issue of competition (e.g. is single operator for the major party of the country acceptable) • Assume follow Yerevan contractual lease model, refining for the new arrangement. • Consider benefits of inclusion of 3 Regional Companies in AWSC lease arrangement

Case Study Session 5.2 THANK YOU! Water & Sanitation David Stiggers, Independent PPP Specialist

Contacts For comments or further details contact: Junglim Hahm jhahm@worldbank.org Richard Cabello rcabello@ifc.org Sabino Escobedo sescobedo@tagfinancialadvisors.com David Stiggers davidstiggers@comcast.net

Case Study Session 5.2 THANK YOU! Water & Sanitation David Stiggers, Independent PPP Specialist