Download

1 / 13

130 likes | 243 Views

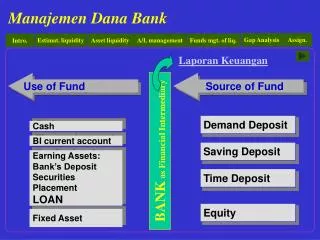

Review of Loans Fund. CIPFA Scottish Treasury Management Forum Workshop 24 February 2012 Hazel Black. Background to Review. LASAAC undertook a review of the loans fund over the period 2010 and 2011 The review group included members of the CIPFA Treasury Management Forum

E N D

Review of Loans Fund CIPFA Scottish Treasury Management Forum Workshop 24 February 2012 Hazel Black

Background to Review • LASAAC undertook a review of the loans fund over the period 2010 and 2011 • The review group included members of the CIPFA Treasury Management Forum • Review was in 2 stages. The first stage led to a recommendation for further work on specific technical issues • Review included a questionnaire. • Two reports were issued • 1 March 2010 • 13 June 2011

LASAAC Review of Loans Fund • LASAAC Report - 1March 2010 • Technical issues identified • Loans Fund Pool Rate • Calculation of Annuity Repayment Schedules • Finance Leases • Investments and Investment income • Interest on Revenue Balances • Policy issues identified • Treatment of capital receipts and grants • Asset transfer between funds • Repayment periods

LASAAC Review of Loans Fund • LASAAC Report – 13 June 2011 • Focussed on the technical issues identified in the March report • Calculation of Annuity Repayment Schedules • Interest on Revenue Balances • Loans Fund Pool Rate

Annuity Scheduling • Initial Conclusions • The legislation permitting the annuity approach is impractical to apply • There is no clear direction as to the interest rate that should be applied in calculating an annuity based repayment schedule. • The requirement for the loans fund to recover interest costs in the year incurred does not seem to be covered by legislation. • It would be useful to clarify when an advance is made as the first repayment is due within 12 months of an advance.

Annuity Scheduling • Recommendations • To recognise that the initial annuity calculation is for the future principal element of the repayment and that future interest charges will vary. The principal element remains fixed for the duration of the loan. • The interest rate should be the pool rate calculated at the end of the financial year. • An advance is considered to be made at the end of the financial year. • All interest costs must be recovered in the same financial year [a conflict was noted re capitalisation of interest].

Interest on Revenue Balances (IORB) • Initial Conclusions • Whilst consistency of practice was desirable the costs and burden of achieving this should be considered. • Recognition that information and systems in place differ significantly across Scotland. • Guidance should be limited to specifying the objective, key principles and considerations for calculation to act as a guide • A non-mandatory model could be provided to set out an acceptable approach

Interest on Revenue Balances (IORB) • Recommendations – Guiding principles • Objective of IORB: to fairly recompense client funds for use of their cash and to fairly charge client funds which use cash for working capital • Identification of client balances: reasonable approximation • IORB rate: appropriate LIBOR rate for relevant period length. May be varied to achieve Objective. • Frequency: weekly or monthly is acceptable. • Interest, transfers and other costs should be allocated in year if possible • Should exclude in year capital expenditure • Loans fund should incur charges/credit and expenses

Loans Fund Pool Rate (LFPR) • Initial Conclusions • Consistency of LFPR is desirable and the guidance does not currently achieve this. • Changes to the LFPR calculation will have an impact on the statutory uses and applications of the LFPR so consultation is indicated. • Changes to the LFPR calculation will affect the LFPR’s use as a comparator. However its use is unlikely to be appropriate in most situations and the issues identified in its use should be included in guidance.

Loans Fund Pool Rate (LFPR) • Recommendations – • Loans Fund expenses, Loans Fund revenue interest (IORB), interest on Loans Fund investments, premiums and discounts are all consolidated into the calculation of the LFPR • Interest and expenses are included in the LFPR on a statutory basis only • Guidance should include limitations on use of LFPR as a comparator • Consultation

LASAAC Review of Loans Fund • LASAAC members considered the report and recommendations and concluded; • that the whole accounting environment had moved on from the situation that existed when the original legislation (1973) was developed and that the Loans Fund policy framework needed to be brought up to date. Once this had been achieved the accounting issues could be considered. • It was agreed that the policy review should be undertaken by the Capital Finance Working Group

Capital Finance Working Group (CFWG) • The CWFG agreed to undertake the policy review. • This review will consider the policy objectives of a loans fund. To include: • the statutory role of the loans fund. • the role of the loans fund as the mechanism for the fair apportionment of debt costs and investment income • The detailed technical work is to be considered by a sub-group of the CFWG. • Detailed work on the review will be undertaken in the coming months

Capital Finance Working Group (CFWG) • The sub group members have been identified and include representatives of the CIPFA Treasury Management Forum as well as accountants • A first meeting has been held to discuss the work to be undertaken • Detailed work on the review will be undertaken in the coming months