Download

1 / 35

350 likes | 460 Views

Information Technology and Corporate Profitability: A Focus on Operating Efficiency. Stephan Kudyba, Donald Vitaliano Information Resources Management Journal , Jan-Mar 2003, 16, 1 Reporter: Yu-Wen Hsiao. Abstract. Involves an empirical analysis , incorporating firm-level investment in IT

E N D

Information Technology and Corporate Profitability: A Focus on Operating Efficiency Stephan Kudyba, Donald Vitaliano Information Resources Management Journal, Jan-Mar 2003, 16, 1 Reporter: Yu-Wen Hsiao

Abstract • Involves an empirical analysis, incorporating firm-level investment in IT • The financial statement information provides an accurate measure of operating revenue (over the period from1995-1997) • Result: IT can enhance firm level profitability • Existing IT: • Advanced computer processing • The proliferation of PCs to the consumer and business environment • The development of the internet • Advanced software applications • New IT: provided infrastructure for advanced information network • Facilitate the flow of value added information • Enable corporate enterprises to more easily operate in the new global economy • All kinds of goods and service are provided that more effectively meet consumer preferences and cost-effective

Introduction • Investment in Information technology is ever-increasing • Enhance operating efficiency and increase productivity and profitability • This paper: whether increased investment in information technology enhances corporate profitability • Using empirical analysis incorporating firm-level investment in IT capital in a profitability function (between 1995-1997) • Provide noteworthy improvement: • Advanced computer processing • Internet as a commercial vehicle • State-of-the-art software applications

Continued focus on operating efficiency 1970s: minimizing input costs by the manufacturing • Costs of materials & business service is 40-80% • The main production decisions: growth of service inputs (i.e. computer, temporary labor) • Aimed at improving the efficiency with intermediate inputs and primary inputs to reduce wastes ( materials & time) • Just-in-time production, statistical process control, computer design and manufacturing • reduce error rates and cut down substandard, rejected production

Continued focus on operating efficiency 1980s: • high technology firms increase in the growth of material inputs in their production of equipment • Economized the use of materials to gain competitive edges

Continued focus on operating efficiency 1990s: • Increases in worker productivity and business efficiency are important • Companies have invested heavily in computers and other innovations to boost efficiency and reduce costs SG&A costs are cut down gradually

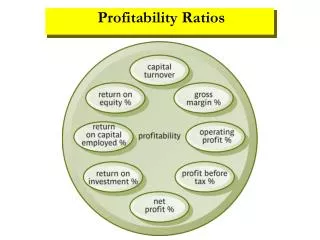

Microeconomic theory & firm profitability • The measure of corporate costs: • Cost of Goods Sold: incurred in the production of goods and services (i.e. materials, labor, manufacturing overhead) • Sell and General Administrative Expenses: costs of selling a product or service • Minimize these costs to increase profitability

Microeconomic theory & firm profitability • Operating income: measure of firm profitability widely • Derive from income statements • (core operation – (CGS+SG&A)) • Advantage: assesses the profitability of a firm’s core foundations

Microeconomic theory & firm profitability • Operating Margin • Operating Margin=operating income/net sales • Higher Operating Margins imply higher efficiency rates lower costs, higher gross margin or combination of the two

Microeconomic theory & firm profitability • Traditional microeconomic theory: • Competitive market firms can’t earn above-normal profits in the long run (enter new competitors) • If market structure is less than perfectly competitive, above-normal profit can be generated beyond the short-term • Barriers: economies of scale, patents and product differentiation • Enable firms to earn excess returns from an extended period

Operating efficiency & IT IT: • Reduce costs by automating capital and labor-intensive activities • Automated teller machines and resulting reduction in tellers and branch locations • IT may enhance profitability by supplying value-added information to DM timely • IS: • facilitate the storage and retrieval of data in to warehouse/marts • Software applications that supply relevant data to end-user

Operating efficiency & IT IT: • Facilitate the use of LANs and WANs • Intranet & extranet • Communication of information between firms, suppliers, distributors and partnering organizations • Augment commerce and brought provider of goods and services closer to the consumer • A survey conducted revealed : • 95% of manufacturers cited benefits from increased in IT • More than 50% exchange accurate information with customers and suppliers

Operating efficiency & IT IT: • 提升公司資料流, 減少Idle 發生, 增加效能 • 不只用於manufactures 還可用於: • Banking and finance, consumer goods, pharmaceuticals • Advanced IT networks provide value-added information to DM (DM可有效率的定義出提升效能策略) • Outsourcing specific function • Creating partnerships • Attaining new production resource • Market share through merger and acquisition

Operating efficiency & IT IT • 使公司程序與表現能更有彈性 • 有效達到產品區別 • 藉由IT可以多國化 • 降低產品的成本(materials and labor) • The background then provides the groundwork for the hypothesis: • H1: IT spending by larger IT intensive firms is positively correlate with above normal profits

Previous research yields conflicting results • Question: whether investment in IT affects firm performance has entailed active debate as productivity studies yielded conflicting results • IT的marginal benefits沒有比marginal costs來的重要 (IT會增加總支出) • IT投資會帶給公司或組織有顯著的contribution (IT的改革產生協力作用)

Previous research yields conflicting results • Empirical studies have shed conflicting results with regards to investment in IT • 分析valve manufacturing firms, 發現投資“IT交流”有正面的影響 • 測驗投資IT如何影響中間的操作變數(i.e. 存貨轉換, 設備使用率) • Result: IT capital對企業選擇策略時,有正面的影響(ex. Market share & ROA) • 測量IT投資的影響藉由ROA & ROE • Result: 對公司利益沒有顯著影響

Previous research yields conflicting results • IT Rate: the ratio of IT stock to number of employees in the firm • IT stock: follows established conventions to incorporate ratios into the profit function • IT Stock 增加的前提假設: • IS labor是公司的支出, 必須要生產資產且要持續在3年以上 • 現行的IS花費, 保持良好的狀況在3年以上

Previous research yields conflicting results • 3個利益測量的測量值: • Return on Assets (ROA) • Return on Equity (ROE) • Total Shareholder Return • 3個可以輔助說明測量值的控制變數 • Debt to Equity • Market Share • Sales Growth

Previous research yields conflicting results • Table1 show no evidence of a significant positive impact of supernormal profitability

A recent empirical analysis • 利用實驗分析可得到以下二者的關係 • Firm rate of investment in IT • Ratio of Gross Operating Margin • Simplistic profit function使用sales growth當控制變數, 並且也包含了Operating Margin在最近期間進行利益測量 • Operating Margin的使用可以精確掌握公司的活動

A recent empirical analysis • 為了驗証H1, 使用了larger IT-intensive firms (from InformationWeek’ 500) • All the data conducted by Computer Intelligence InfoCorp • Rankings: the amount of PCs, LANs, and mainframe computers currently installed & planned purchases • Detailed information reported include: • IS Budget, Total Employees, IT Employees and Revenue • IS Budget: corporate wide capital and operating budget for IS (hardware, software & others)

A recent empirical analysis • Corporate data: financial information (i.e. balance sheets, income statements & cash flow statements) • 用來做二個firm-level的評估: • CGS (cost of Goods Sold) • 在某期間的生產成本與購買之商品 • SG&A (Selling & General Administrative Expense) • 銷售與一般支出

A recent empirical analysis • IT capital: IS的一部份, 涉及PCs & mainframes (hardware) • 1990-1992年佔30%的IS Budget, 1990年佔27%的 IS Budget

A recent empirical analysis • IT capital每年會有0.25的折舊或廢棄率 • Bureau of Economic: 70-90年間的電腦損失率每年是24.3% • (dc-pc) = the rate at which equipment loses value • dc = the depreciation rate • pc = the rate of nominal price change

A recent empirical analysis • IT labor: 主要會受到增加IT employees所影響, 比較切身的關係是薪資的問題

A recent empirical analysis • 有效的IT investment首先要妥善管理operating activities • Operating activities: 結合establishing scale & product differentiation barriers, 將可以在長期之下帶來Operating Margin的增加 • 增加IT Rate可致使operating management與收入相對的增加 • IT network 提供value-added information, 可以減少資源的浪費, 像backlogs in orders, ineffective marketing campaingns, returns due to defects in goods & services, inaccurate pricing strategies…

A recent empirical analysis • R2 terms: 可以說明Gross Operating Margin的變化 • IT Rate & sales growth: generally significant • 1997的樣本數過少, 導致不顯著

A sector analysis • Service-based companies: • 都產生不顯著的結果 • R2反應不顯著

A sector analysis • Manufacturing: • 95 & 97年較有正面的顯著影響 • 個數的不足會顯影結果

A sector analysis • Limitations: • IT投資在公司營運上潛在的lag affect • IT潛在的管理不善 • 要精確的測量IT的值是有其困難度 • Server companies較為不顯著的原因: • IT投資在公司營運上潛在的lag affect

Reasons for recent profit results • The impact investment in IT had on profitability, yielded no conclusive results. • 太著重於競爭者上的花費, IT將沒有明顯的報酬 • 資訊經費縮減, 競爭激烈, 須以降價方式, 致使利益減少 • 政府投入資訊經濟, 增加競爭, 減少利益 • IT投資增加可得到正面的利益 • IT增加的方式 • 準備最好的軟體快速存取, 應用 • 電信改革增加internet • 增加PC的效能建立客戶& 企業環境 • Intranet & Extranet容易取得即時資訊 • Information network即時提供加值資訊給users

Reasons for recent profit results • 有效的資訊: • 減少不確定性 • 提升決策效率 • 提供商品, 服務, 取得好的成本效業方法…

Reasons for recent profit results • 本實驗目的: • 透過利益的測量可減少容錯率 • 公司績效 (ROA & ROE) • 包含許多公司程序的變化, 將會影響分析結果 • Gross Operating Margin • 可以精確掌握公司管理營運活動的能力

Closing remarks • IT改革帶動資訊經濟的發展 • 本文提出90年間一個自然且正常變動的趨勢之例子 • Internet should prove to be a driving force to enhance communication between businesses & their affiliates & with the ultimate consumer • Future research: 測量IT密集 & 公司結構