Navigating Foreign Exchange and Hedging Products: USD/INR Journey and Risk Management

310 likes | 431 Views

This comprehensive analysis explores the journey of USD/INR from 2007 to recent times, highlighting key economic events impacting exchange rates, including the sub-prime crisis and U.S. GDP fluctuations. The paper discusses the significance of hedging in a volatile foreign exchange market, emphasizing forward contracts and options as tools for risk management. Moreover, it details regulatory guidelines governing forward contracts and derivative transactions in India, ensuring corporations understand their exposure and options available for currency and interest rate risk mitigation.

Navigating Foreign Exchange and Hedging Products: USD/INR Journey and Risk Management

E N D

Presentation Transcript

FOREIGN EXCHANGE AND HEDGING PRODUCTS

The US Economy • Came to surface with sub-prime crisis – Double dip recession. • US GDP grew 1.3% in Q2 2011 and is put at 1.7% in 2011 compared to 3% in 2010. • S&P downgraded USA to AA+ from AAA. • US unemployment rate is around 9%. • Initial jobless claims hovering at around 400,000 levels. • Doubts being raised on the status of USD.

The Euro Zone Economy • The Euro zone is governed by the “PIIGS” economies. • Huge public debt. • Greece default risk jumps to 98%. • Downgrade of euro zone economies by rating agencies. • French bank’s rating was downgraded by Moody’s. • IMF lowers global growth forecasts to 4%.

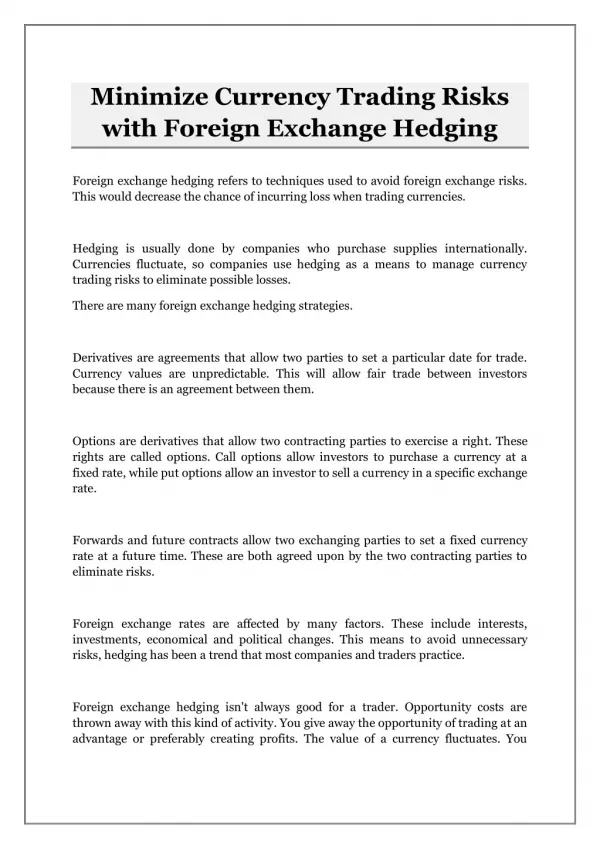

RISK IN FOREX OPERATIONS High volatility is the distinctive feature of foreign exchange market Globalization of Indian economy is increasingly exposing the Indian corporates to greater forex risks. The uncertainty of the moves and lack of clear trend rules the market. HEDGING AND NOT SPECULATING

FORWARD CONTRACT • A Right To Buy Or Sell Foreign Currency At An Agreed Price On A Future Date. • Both A Right And An Obligation

No chance of participating in market volatility Profit/loss crystallized on the date of booking The upside and downside (opportunity profit/loss) theoretically unlimited Forward points are difference between interest rates between the currencies. FORWARD CONTRACTS

Can be booked for period up to one year and beyond. Flexibility of one month option period. Gain or loss depends on prevailing rate. At the time of booking, no money changes hands. Debits/credits are carried in to the Customer’s account only on the settlement date. FORWARD CONTRACT

OPTION • A Contract To Buy Or Sell Foreign Currency At A Agreed Price On A Future Date. • A Right But Not An Obligation • Premium payable upfront. Fixed Maturity.

A call option is an option to buy a certain asset by a certain date for a certain price (the strike price) A put option is an option to sell a certain asset by a certain date for a certain price (the strike price) Options

OPTIONS • SPOT RATE: 52.62 • 1 M FWD: 52.98 Rs .87 • 3 M FWD 53.50 Rs 1.32 • 6 M FWD 54.21 Rs 1.75 • 12 M FWD 55.04 Rs 2.42

SWAPS • Swap Is A Contractual Agreement To Exchange Specified Cash Flows At Future Dates

Mechanism of SWAP ABC Ltd, an Indian corporate borrows US Dollar at 6 mths Libor + 150 bps (0.5 % + 1.50= 2.00 %) to be repaid after 5 years. The company converts the USD into Rupees at present USD/INR rate (49.00). What risks the company is open to? What happens if Libor rate after 1 year goes to 3 % and keeps rising? What happens if the USD/INR rate on repayment date is more than present rate? ABC Ltd can enter into a SWAP deal to hedge uncertainty of future 1) Interest rate or 2) Currency rate or 3) both currency and interest rate.

PRINCIPAL ONLY SWAP (POS) USD Liability USD Cash Flows Bank A Corporate INR Cash Flows @ spot (pays premium %)

INTEREST RATE SWAP (IRS) Floating to Fixed LIBOR Liability Bank Pays Floating Interest Rate 6mL(0.53)+300 Bank Corporate Corp Pays Fixed $ Interest Rate 4.75%

CIRS USD Liability (FCL) Pays Floating Interest Rate (L+300) USD Cash Flows BANK INR Cash Flows @ spot CORPORATE Corp Pays Rs Fixed Interest Rate 8.8% USD loan converted into a INR loan synthetically

Regulatory Requirement Governing Forward Contracts and Derivative Transactions

Guidelines for Forward Contract and Derivative Transactions RBI has classified exposure in two categories Probable Exposure : Average of last three years turnover or last year turnover, whichever is higher. ( For importers the facility stands reduced to 25% of limit). Contracted Exposure : Limits can be sanctioned to the extent of underlying exposure that is available.

Guidelines for Forward Contract and Derivative Transactions Guidelines for Contracted Exposure: • Underlying documents to be submitted while booking contract. Grace period of 15 days provided after which contract be cancelled and no exchange gain to be passed. • Certificate that the exposure is not covered with any AD category 1 bank and if covered in parts, the details thereof. • Quarterly certificate from statutory auditor of customer that contracts outstanding at any point of time during the quarter did not exceed the underlying exposure. • RBI withdraws facility of rebooking once contract is cancelled ( which involves INR as one of currencies).

Guidelines for Forward Contract and Derivative Transactions Guidelines for Probable Exposure: • Limits to be assessed at the beginning of financial year. RBI has allowed a period of three months for submission of audited statement. • Separate limit to be assessed for import and export and advised to customer both in terms of notional and credit exposure limit. These limits to be monitored separately for import and export. • All fwd contracts under this facility on fully deliverable basis. In case of cancellation exchange gain, if any, should not be passed to customer.

Guidelines for Forward Contract and Derivative Transactions Guidelines for Probable Exposure: • Aggregate contracts booked during financial year and outstanding at any point of time should not exceed past performance eligibility , separately for import and export, subject to availability of CEL. • Past performance limits once utilized are not to be reinstated either on cancellation or on maturity of contracts. • Contracts booked under the facility once cancelled are not eligible to be rebooked. Rollover is also not permitted.

Guidelines for Forward Contract and Derivative Transactions Branches to allow customer to use past performance facility after satisfying that following conditions are complied with: • An undertaking may be obtained from customer that supporting documentary evidence will be produced before the maturity of all the contracts booked. • Customers to furnish quarterly declaration, duly certified by Statutory Auditor, stating the amount booked with other AD Category I banks under this facility.

Guidelines for Forward Contract and Derivative Transactions c. Aggregate outstanding contracts in excess of 50% of eligible limit may be permitted on being satisfied about genuine requirement of the customer after examination of following documents: • A certificate from statutory auditor of customer that all guidelines have been adhered to while utilizing facility. • A certificate of import/export of customer during past three years duly certified by statutory auditor in the format prescribed by RBI.

Uncertainty Remains …. India will have to learn to live with volatility in the Global economy. RBI