Download

1 / 25

420 likes | 941 Views

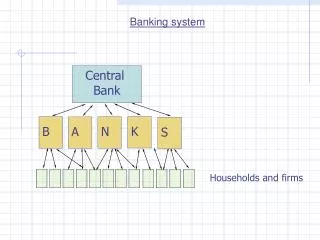

The Chinese Banking system. The Chinese financial system, spring 2014 PV Viswanath Lubin school of business. Learning objectives.

E N D

The Chinese Banking system The Chinese financial system, spring 2014 PV Viswanath Lubin school of business P.V. Viswanath

Learning objectives • Beginnings of the banking system from a mono-bank and its development to a tripartite system of a central bank, a set of development banks and a set of commercial banks, in addition to a private banking sector. • How the four major State-Owned-Banks turned State-Owned-Commercial Banks were equitized and began to trade on stock exchanges, but nevertheless remained state-controlled. • Brief description of the other parts of the banking sector. • Outline of the banking regulatory system consisting of the PBOC, the CBRC and the MoF. • Bad loans and their resolution: NPLs and Asset Management Companies. P.V. Viswanath

Early developments • Prior to 1978, the Chinese banking system was largely government-owned and isolated from the global economy. The banks were subservient to the requirements of China’s central planned economy. The PBOC was the central bank, as well as the only commercial bank, and it was under the control of the Ministry of Finance (MOF). • However, once China moved to a market-based system, centrally planned and directed banking couldn’t work. By the end of 1979, the PBOC became a separate entity, independent of the MOF. • In the 1980s, four state owned specialized banks (SOBs) were established to take care of banking proper, while the PBOC maintained its central banking functions: • the Bank of China (BOC), specializing in transactions relating to foreign trade and investment • The Agricultural Bank of China (ABC), originally established in 1951 by Mao as the rural unit of the PBOC, was reestablished in 1979 to deal with banking business in rural areas. • The China Construction Bank (CCB) handled transactions related to fixed investment especially in manufacturing and • The Industrial and Commercial Bank of China (ICBC) was formed in 1984, out of a PBOC branch, to take over the rest of the commercial transactions of the PBOC. P.V. Viswanath

structure of banking system • In 1993, China’s State Council promulgated a “Decision Regarding Reform of the Financing System.” This was followed in 1995 by the “Law on Commercial Banks.” The four specialized banks now became state-owned commercial banks. • In 1994, three wholly state-owned policy banks were set up to take over the development function, i.e. they follow a non-commercial development agenda, for the most part. • the Agricultural Development Bank (distinct from the ABC) which is supposed to support the development of agriculture and rural areas • China Exim Bank, which provides financial services to promote Chinese exports, particularly of high-tech and new-tech products and facilitates the import of technologically advanced machinery and equipment. • the China Development Bank (CDB), which was responsible for raising funds for large infrastructure projects. However, the CDB has started to be involved in commercial loans (see http://online.wsj.com/news/articles/SB10000872396390443847404577631433239050666). • In addition, there are smaller state-owned banks, such as the Bank of Communications (restructured in 1986), and HuaxiaBank (set up in 1992), which became formal joint-stock commercial banks in 1995. • Starting in 2005, China began transforming the wholly state-owned banks into joint-stock corporations, a process that has been called equitization or corporatization. P.V. Viswanath

State owned banks • The original policy banks, as well as some of the state-owned commercial banks, have now been equitized. Here are some details of the largest equitized banks. Martin, China’s Banking System and Cousin, Table 8.4 P.V. Viswanath

State owned banks • A large proportion of the shares of these banks are held by the PBOC, the MOF or other government entities; hence they are very much under government control. • Tradable shares of the equitized banks are sold on the Shanghai and Shenzhen stock markets (A and B shares) to Chinese investment funds, qualified foreign institutional investors (QFIIs) and private Chinese investors and on the Hong Kong Stock Exchange (H shares)to overseas investors. A and B shares are denominated in renminbi (RMB or 人民币) and Hong Kong shares in HK dollars. Prices of these shares differ because supply and demand differ across markets and arbitrage is not possible. • Each of the equitized banks has a board of directors and senior officers, who are appointed by the central government, but have at times turned out to be quite dynamic and innovative in spite of such government control. P.V. Viswanath

State owned banks • The BOC, CCB, ABC and ICBC together constitute a huge portion of China’s banking and financial system. As of 2010, these banks accounted for over 70% of the $11 trillion in financial assets held in banking system and 43% of China’s total financial assets. (Walter and Howie, p. 27) • Most low income countries have a concentration of assets in the banking system, however in China, the government controls most of these assets; foreign banks hold little more than 2% of total financial assets, while in the international lower-income group of countries, this number was 37% (Walter and Howie, p. 28). • The largest assets for the five large equitized banks were (Table 6 of Martin): • Loans, with corporate loans being three times or more the value of personal loans. The personal loans were predominantly mortgage loans. • Significant investments in securities, including government and corporate bonds. • Required reserves held at the PBOC; as of May 2012, the required reserve ratio was 20% for large banks and 16.5% for smaller banks. • In terms of liabilities, corporate and personal deposits were the largest proportion, at least 75% of all liabilities. To put it in perspective, deposits at JP Morgan Chase as of 2012 end were $1.19tr, compared to liabilities of $2.1tr, or 57%. Other liabilities included federal fund borrowings, commercial paper, long-term debt, accounts payable and trading liabilities. P.V. Viswanath

State owned banks and the state • The state exerts a strong influence on bank lending (“Privatisationin China: Capitalism Confined,” Sept. 3, 2011, The Economist) • Bank directors and senior bank officers are directly appointed by the Communist Party Organization Department (see McGregor, Chapter 3 and Cousin, Table 8.5) • Career Opportunities of senior bank officers depend upon the assessments of the official agencies responsible for their appointment, which makes them beholden to the party. • The Central Government may apply direct pressure on bank officials to provide loans and services to specific projects or investments. • Such pressure can be strong when the government is interested in promoting economic growth, as happened in 2008. • This has led to growth of non-performing loans (NPLs) because there is pressure to lend to SOEs, but not equal pressure on SOEs to repay. P.V. Viswanath

Private commercial banks • Private commercial banks are either Chinese-owned or foreign-owned: • There were twelve Chinese-owned joint-stock commercial banks in 2012, thirty-seven foreign-owned banks, two foreign joint-venture banks and one wholly foreign-owned finance company. (Martin, p. 5) • All large Chinese commercial banks are universal banks; they offer loansand deposit products, are agents for fund and insurance products (important), transfer money, offer trust investments and a wide range of fee-generating products. But their mainstay is deposits and loans (cf. above). • Some Chinese banks have carved out niches: • Mingsheng is a leader in SME lending • Merchants Bank is strong in the area of credit cards. • Bank of Communications (BoComm) and Merchants Bank have acquired smaller city commercial banks and established rural institutions. • BoComm acquired a small insurance company in 2009. • In 2007, ICBC acquired Bank Halim Indonesia, 20% of S Africa’s Standard Bank and 80% of Macau’s Seng Hang bank; in 2009, it acquired ACL Bank of Thailand and, in 2010, a 70% stake in the Bank of East Asia Canada. • CCB has made acquisitions in Hong Kong, Taiwan and Vietnam. • Not all these investments have been successful; some banks lost money in the 2008 crisis (Merchants and Minsheng). P.V. Viswanath

City commercial banks • City Commercial Banks are urban local banks set up originally under the aegis of local governments. Most of them are headquartered in urban centers and their development is linked to their narrow scope and environments. • Many of the CCBs grew by taking over urban credit cooperative banks. • They accounted for 8.2% of total bank assets as of the end of 2010 (Martin, p. 7), compared to 15.6% for the J0int Stock Commercial Banks. • However, they rank just behind the SOCBs in their local markets. • CCBs are prominent in lending to local governments for their large infrastructure projects. This is related to the fact that 75% of the capital of CCBs is owned directly or indirectly by local governments (Cousin, p. 125). The importance of the local government connection is shown by the fact that the profitability of these banks is related to the level of revenues of the local government. Where local governments have abundant revenues, NPLs are lower. • Some CCBs have foreign investors (Cousin, Table 9.2): Bank of Beijing (ING Bank), Bank of Tianjin (ANZ Banking), Bank of Jilin (Hana Bank), Bank of Nanjing (International Finance Corp and BNP Paribas), Bank of Shanghai (HSBC and others), Bank of Chengdu (Hong Leong Group), Urumqi CCB (Habib Bank), Bank of Qingdao (IntesaSanpaolo, Rothschild Group) and others. P.V. Viswanath

Foreign Banks • Foreign banks were allowed into China in 1978. However, until 2006 (when WTO commitments were implemented), restrictive regulations made it difficult for them to make inroads. Foreign banks have a less than 2% share of bank assets in China (Martin, Table 3). • However, in certain sectors, they did better; for example, they had 20% of the market in foreign currency loans (Cousin, p. 133) • HSBC, the Bank of East Asia, Standard Chartered and Citigroup are the major foreign banks. Their branches are mostly concentrated in coastal areas though inland branches are being opened. • In order to enjoy the same regulations as Chinese commercial banks, foreign banks need to register a subsidiary, which requires RMB 1 b. in capital. • Chinese customers are loyal to their banks and banking relationships last, on average, 9 to 12 years; this makes it difficult for foreign banks to make inroads. • Foreign banks complain about non-transparency in regulations and that branch approval is slow. P.V. Viswanath

Rural financial institutions • Rural areas have been served by rural credit cooperatives, the postal savings system, the Agricultural Bank of China and the Agricultural Development Bank of China. • Rural financial institutions makeup about 11.2% of total bank assets (Martin, Table 3). • The importance of RCCs varies from region to region and from sector to sector. In Fujian province, RCCs account for 96% of all agricultural loans (though they only account for 9% of all loans in the province). • Overall, their loan portfolios are heavily geared towards agricultural lending. They benefit from a close relationship to their target market and are often the sole financial institution on these under-banked rural areas. • RCCs were established in the 1980s as part of the ABC framework, but this setup did not work very well – for one, the RCC deposits were siphoned off by the ABC. In the 1990s, the RCCs and the ABC were made independent of each other, which made the RCCs more efficient. • RCC customers include rural farmers, rural enterprises as well as local authorities. However, the loan-deposit ratio is low because RCCs do not want to lend without collateral. Also, loans are short term and not adapted to farmers’ requirements, both in terms of maturities and payment schedules. • Although RCCs are nominally cooperatives, they are controlled by insiders and by local governments. This structure also makes it difficult to obtain foreign investment. • RCCs in general have shown themselves to be not very efficient or profitable. Client needs in rural areas still need to be met properly. P.V. Viswanath

Banking regulatory system • The PBOC implements China’s monetary policy. • The China Banking Regulatory Commission (CBRC) along with the PBOC oversees China’s banking institutions. • The State Administration of Foreign Exchange (SAFE) is responsible for the supervision and monitoring of foreign exchange transactions in China, as well as the management of the governments’ foreign exchange reserves. • The Ministry of Finance (MoF) is responsible for China’s fiscal policies as well as the Central Government’s budget. P.V. Viswanath

major responsibilities of the PBOC • Formulating and implementing monetary policy • Issuing renminbi(人民币) and regulating its circulation • Regulating the inter-bank lending and bond markets • Administering foreign exchange and regulating the inter-bank foreign exchange market • Regulating the gold market • Holding and managing official foreign exchange and gold reserves • Managing the state treasury, including the issuance of treasury bonds and other government securities • Operating the payment and settlement system • Maintaining financial statistics and conducting financial analysis and forecasts • Guiding and organizing anti-money laundering operations; and • Issuing and enforcing relevant orders and regulations. P.V. Viswanath

PBOC and monetary policy • The PBOC uses the following instruments of monetary policy: • Setting reserve requirements for banks and other financial institutions, • Setting the discount rate (interest rate) for intra-bank lending • Controlling the supply of money via the issuance of currency and open market operations • The PBOC also sets benchmark interest rates for RMB-denominated deposits and loans and allocates credit limits to Chinese banks. • The PBOC (in contrast to the US Fed) uses changes in banks’ reserves requirements as its primary method of signaling its desire to tighten or loosen bank lending, and thereby, the money supply. Statutory reserve requirements are around 20% in China (in 2012), whereas in the US, they are only 10% on holdings greater than $89m. • The PBOC also uses changes in benchmark interest rates for deposits and loans in its monetary policy, but with less frequency than reserve requirement changes. P.V. Viswanath

PBOC and monetary policy • As of July 2012, the benchmark interest rate on 1 year loans was 6%, and 6.55% on loans above 5 years. • Benchmark Demand Deposit rates were 0.35%, 1 year deposit rates were 3%, 5-year deposit rates were 4.75%. • Under Chinese law, banks are allowed to offer interest rates within a band above and below the benchmark rates. For example, currently bank lending rates can be no less than 90% of the benchmark rate, with no upward limit. • However, the Chinese inflation rate averaged 5.8% from 1986 until 2013. Of late, it has been much lower. In 2013, it was 2.51%; in 2012, it was 2.41%; in 2011, it was 4.06% and in 2010 it was 4.57%. • Consequently, the real interest rate offered by banks is close to zero, and has often been negative. • Lending rates, though higher than inflation, are still not very high and real lending rates are 3% to 3.5% p.a. Considering that real GDP growth rates are higher than 7%, it is clear that lending rates are below equilibrium; hence there is a lot of demand for loans. However, as explained before, it is mainly the SOEs that are able to borrow at these rates. • In late 2010, Zhou Xiaochuan, Governor of the PBOC, advocated a policy of market-based interest rates; however, this has not yet happened. For one thing, this would put pressure on SOEs, who currently have easy access to money at low rates. P.V. Viswanath

China banking regulatory commission • The CBRC was created in 2003 following the 1997 Asian financial crisis and is responsible for the regulatory oversight of China’s banks, ensuring that they are abiding by the relevant laws and regulations and that the interests of depositors and consumers are protected. Its main functions are: • To authorize the establishment and business scope of banks in China • To formulate and enforce banking regulations • To audit and supervise all banks operating in China • To compile and publish information on China’s banking sector. • To formulate proposals for the resolution of problem deposit-taking institutions in consultation with relevant regulatory authorities. • The current CBRC Chairman is Shang Fulin, who was previously the chairman of the CSRC; he is also a member of the Monetary Policy Committee of the PBOC. P.V. Viswanath

China banking regulatory commission • The CBRC has generally been more cautious about the liberalization of China’s banking sector; it sees excessive deregulation and poor oversight by the US as the principal causes of the global financial crisis. • It’s top priorities are, based on talks given by Shang Fulin in 2012 and 2013: • To promote efficiency in banking institutions • To improve the risk control system • To strengthen external supervision and internal controls • To deepen financial reform by speeding up product and service innovation especially for rural areas and SMEs • To promote economic restructuring • To close down illegal financial activities. • Broadly speaking, the CBRC is in charge of individual financial institutions, whereas the PBOC pays more attention to systemic issues. P.V. Viswanath

Ministry of finance • The Ministry’s current functions are: • To formulate and implement China’s fiscal policies • To prepare and administer the central government’s annual budget • To propose and collect taxes for the central government • To prepare plans for the issuance of treasury bonds and other central government debt • To formulate and implement accounting regulations for businesses operating in China • To collect data • To conduct research on China’s economy and its fiscal situation • Although it does not have as much power as it did, it still holds equity in some banks and other financial institutions, e.g. it holds 50% of the equity in the ABC. • Its approval is necessary for all major changes in banking policy. P.V. Viswanath

Mof/ PBOC rivalry • In the past, the MoFhas been at loggerheads with the PBOC. For example, following the 1997 Asian financial crisis, the PBOC proposed direct infusion of cash to the four major SOBs accompanied by governance reform and improved loan valuation procedures. The MoF suggested a good bank/bad bank strategy whereby newly created Asset Management Companies would acquire NPLs from the ailing banks and try to collect on them. • In 2006, China was worried about the huge unproductive dollar reserves that it was sitting on; meanwhile the dollar was also weakening causing a drop in the value of China’s wealth. The PBOC wanted to invest this wealth directly through its affiliated organization, the State Administration of Foreign Exchange (SAFE). • Ultimately, a new sovereign fund was created in 2007, the China Investment Corporation (CIC), staffed primarily with personnel tied to the Ministry of Finance and the National Development and Reform Commission (NDRC). In addition, the PBOC's holdings of shares of China’s state-owned banks (under Central Huijin, a SAFE subsidiary) were sold to the newly created CIC at below-market prices. P.V. Viswanath

safe • The State Administration of Foreign Exchange (SAFE) was established in 1978 as a carve out of the PBOC; it reports both to the State Council and the PBOC. • Its main function is to manage China’s foreign exchange, including maintaining balance of payments statistics, regulating and monitoring foreign exchange transactions, and managing China’s foreign exchange reserves. • As the regulator of foreign exchange transactions, SAFE must approve the outlay of any forex for overseas investments by Chinese banks and companies. • As the manager of China’s forex reserve, SAFE also acts at times like a bank, providing credit to companies seeking to make overseas investments. • SAFE keeps the details of its investments secret, but generally invests in safe assets, such as US Treasury bonds. • SAFE is also responsible for the regulation of Qualified foreign institutional investors (QFIIs), non-Chinese entities that are allowed to purchase stock, bonds, and other financial assets in China. P.V. Viswanath

Asset management companies • In 1999, the country’s then four major banks, ABC, BOC, CCB and ICBC, were virtually insolvent because of NPLs (from loans made mostly to SOEs). • As part of an effort to rescue the banking sector, the State Council transferred 1.4 tr. 元in NPLs to four newly created asset management companies (AMCs). The NPLs of each bank were transferred to one of the new AMCs at full face value in 1999 and 2000. However, this still left a lot of NPLs on the balance sheets of the four banks and of other Chinese banks. • A second round of NPLs were transferred to the AMCs in 2004 and 2005 totaling about 1.6 tr. 元, this time at a discount to face value. Ultimately, a total of about 3.6 tr. 元 in NPLs was transferred. • The four AMCs were originally owned by the MoF and were supposed to recover as much of the debt as possible by debt collection, debt restructuring, debt-equity swaps, or loan repackaging and resale. • The AMCs were capitalized to the tune of 10 b. 元 in initial capital by the MoF in exchange for AMC bonds. • The AMCs issued an additional 858b. 元 in bonds in 2000 with a coupon yield equal to the one-year deposit rate; these bonds were mostly bought by the four major banks, which effectively put the NPLs back on the banks’ balance sheets. P.V. Viswanath

AMC details Disposal Ratio = Book Value of Assets Disposed of/Total NPLs purchased by the AMC Asset Recovery Ratio = Total (non-cash) Assets Recovered/Book Value of Assets Disposed of Cash Recovery Ratio = Cash Recovered/ Book Value of Assets Disposed of P.V. Viswanath

Asset management companies • The AMCs sold some of the NPLs by bundling bad loans by province, debtor or investor and selling them to foreign and domestic investors, including Bank of America, BNY Mellon, Cargill and Citigroup. • Recovery rates have been low – the cash recovery rate was 20.8%, and the asset recovery rate was 24.2% . Since the easier-to-collect loans were probably dealt with first, the chances of further recovery are slight. • The MOF subsequently allowed the AMCs to engage in a broader range of asset management activities, including purchasing shares in other companies. • Minority interests in the AMCs were also sold to selected domestic investors, including the original policy banks themselves (ABC, CCB and ICBC). • The problem of unresolved NPLs remains a big problem for Chinese banks, since the original management deficiencies that created them continue to exist. • Apparently the Chinese government plans to issue an IPO in Cinda, one of the AMCs (http://www.scmp.com/business/china-business/article/1297653/chinas-insolvent-toxic-waste-dump-cinda-sale). P.V. Viswanath

Themes • The current structure of the banking sector is, to some extent, an outcome of historical events and prior decisions. • The State owns a large part of all the large banks. • The State is directly involved in the appointment of the important managers of large banks and other personnel decisions. • The State interferes in the loan approval process in order to benefit SOEs. • This has resulted in high levels of NPLs, a situation which has still not been resolved. • Borrowing and lending rates are set or controlled by the PBOC, which, compounded by the absence of other investment opportunities, has resulted in financial repression. • Since the major banks are State-owned and are forced to lend to SOEs, they are bankruptcy-remote; this leads to a continuing problem of moral hazard. P.V. Viswanath