TIMBER CAPITAL GAINS

40 likes | 231 Views

TIMBER CAPITAL GAINS. TIMBER CAPITAL GAINS. Rate Changes

TIMBER CAPITAL GAINS

E N D

Presentation Transcript

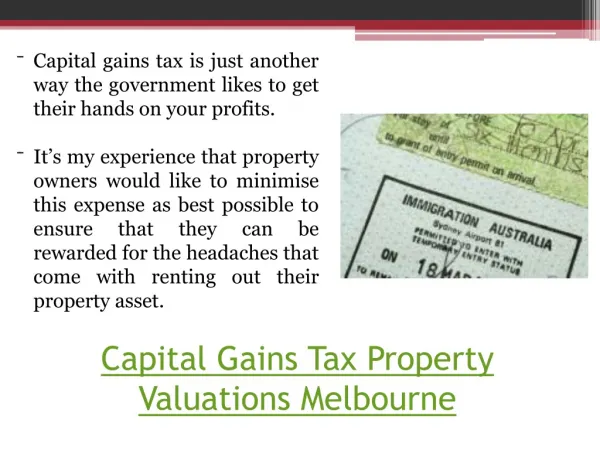

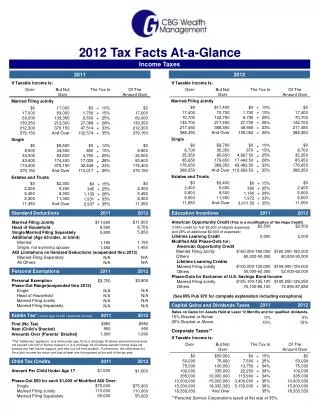

TIMBER CAPITAL GAINS Rate Changes • The 2003 Tax Act temporarily lowered long-term non-corporate capital gains rates applicable to timber sale income from 20 to 15 percent (higher income taxpayers) and from 10 to 5 percent (lower income taxpayers). The changes were to apply through the end of 2008, with the 5 percent rate reduced to zero for 2008-2010. • Recently enacted legislation has extended the 15 and 5 percent rates through 2010. • The corporate long-term capital gain rate remains the same as the applicable corporate ordinary income rate.

TIMBER CAPITAL GAINS IRC Section 631(b) Changes Old Law • Prior to 2005, lump-sum timber sales (sale by timber deed) qualified for capital gain treatment under IRC Section 1221 only if the seller was considered to be an investor, not in the trade or business (dealer) of selling standing timber. • Dealers could qualify for long-term capital gains treatment, however, by disposing of standing timber under IRC Section 631(b) using a contract wherein they retained an economic interest ( i.e., a pay-as-cut contract).

TIMBER CAPITAL GAINS IRC Section 631(b) Changes New Law • Effective January 1, 2005, Section 631(b) was amended to provide that "dealers" can qualify for long-term capital gain treatment via either a lump-sum sale or a retained economic interest disposal. Those sellers subject to Section 631(b), however, irregardless of which method is used, must continue to report the transaction on IRS Form 4797.