Download

1 / 48

480 likes | 751 Views

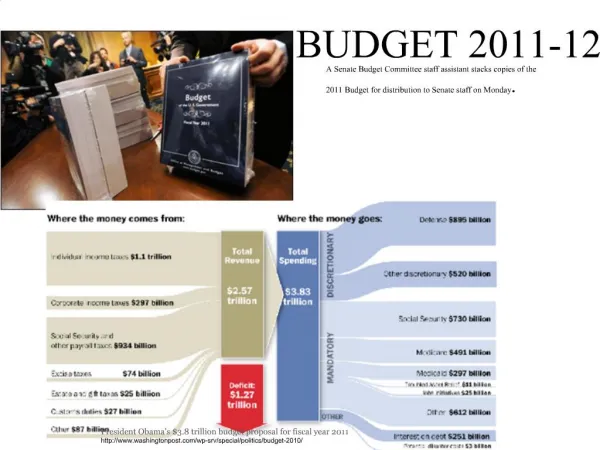

2011-12 Budget Budget Seminar: ‘ Understanding the Budget’. Presented by: Garth Day Scott Kompo-Harms Richard Webb. The State of the Economy. See Budget Paper 1, Statement 1, Table 1 for: real GDP growth and inflation forecasts. Lower real GDP growth estimates Natural disasters

E N D

2011-12 BudgetBudget Seminar: ‘Understanding the Budget’ Presented by: Garth Day Scott Kompo-Harms Richard Webb

The State of the Economy See Budget Paper 1, Statement 1, Table 1 for: real GDP growth and inflation forecasts • Lower real GDP growth estimates • Natural disasters • Patchwork economy • Higher inflation • Food and petrol

Where to look for information? • The Budget Speech • The Budget Overview • The Budget Papers • BP1: Budget Strategy and Outlook • BP2: Budget Measures • BP3: Australia’s Federal Relations • BP4: Agency Resourcing • Portfolio Budget Statements • Main source of information on proposed agency funding and activities

Budget Paper No. 1 • BP1 – Budget Strategy and Outlook • S1: Budget Overview • S2: Economic Outlook • S3: Fiscal Strategy and Outlook • S4: Special Topic • S5: Revenue • S6: Expenses and Net Capital Investment • S7: Assets and Liability Management • S8: Statement of Risks • S9: Budget Financial Statements • S10: Historical Australian Government Data

Budget Papers • BP2: Budget Measures • Policy decisions in the Budget and since MYEFO • Three sections: revenue, expenses and capital • BP3: Australia’s Federal Relations • Payments for specific purposes, general revenue assistance, debt transactions, consolidated non-financial public sector and accountabilities under the Federal Financial Relations Framework. • BP4: Agency Resourcing • Annual appropriations, Special appropriations and Special accounts

Budget Balance Concepts • The headline ‘cash’ budget balance • Total receipts - total payments. • Call on financial markets of government activity • The underlying ‘cash’ budget balance • Removes net cash flow of investments in financial assets (e.g. Telstra sale) and Future Fund earnings • Measure of public saving (surplus), dis-saving (deficit) • The fiscal budget balance • Accrual counterpart to underlying cash balance • Captures long-term effect of current policy decisions

The Budget Aggregates See Budget Paper 1, Statement 1, Table 2 - cash terms: receipts and payments - accrual terms: revenue and expenses

Cash and Accrual Accounting • Gross debt • Total Liabilities • Net debt • Deposits held, government securities, loans and other borrowing minus cash and deposits, advances paid, and investments, loans and placements. Peaked at -3.8% in 2007-08 • i.e. Working capital: current assets minus current liabilities • Net worth • Total assets - total liabilities. Peaked at 6% of GDP in 2007-08 • Net financial worth (used in fiscal strategy) • Financial assets – liabilities. Peaked at -1.5% of GDP in 2007-08 • See BP1 Statement 9: Budget Financial Statement

Structural and Cyclical Factors • The structural component of the budget is driven by policy decisions (termed discretionary fiscal policy). • Budget Paper 2 – Budget Measures: • e.g. CPRS deferral, Flood Levy, MRRT • The cyclical component of the budget is driven by fluctuations in economic activity impacting: • Individuals income tax • Company tax • Indirect tax • Social security & welfare payments

The Fiscal Strategy • The 2008-09 budget formally introduced the Government’s fiscal strategy: • Achieving budget surpluses, on average, over the economic cycle; • Keeping taxation as a share of GDP, on average, below the level for 2007-08; • Taxation receipts less than 23.6% of GDP, on average • Improving the Government’s net financial worth over the medium term. • cyclically-adjusted budget surpluses, accrual basis

The Fiscal Strategy – Part II • Allow cyclical variation in the budget, temporary targeted stimulus (discretionary policy decisions) and New Policy Proposals (NPPs) to be offset. • Allow tax receipts to recover naturally and hold real growth in spending (payments) to 2% p.a. until the budget returns to surplus. • Then, maintain growth in spending at 2% p.a., on average, until surpluses are at least 1 per cent of GDP.

Fiscal Challenges & Opportunities • The 2012-13 surplus is a first step to achieving the Fiscal Strategy, and structural surpluses, on average. • Receipts • If tax receipts average 23.6% of GDP p.a., consistent with the Fiscal Strategy, $150 billion of additional revenue may be generated, more than offsetting accumulated deficits of $129.2 billion • Tax policy: maintain incentives to work and invest • Payments • If real payments grew, on average, by 2 per cent p.a., consistent with the Fiscal Strategy, then an additional $74.6 billion of expenditure may be allocated • Spending policy: well targeted, value for money and social return

Structural Budget Estimates Source: 2009-10 Budget Paper No.1 p4-17, updated by Treasury (2010).

Scott Kompo-Harms • The Budget and macroeconomic policy • Monetary policy (brief description only) • Fiscal policy (main topic of interest) • Instruments • Effects • Economic Forecasting • Background • Process • Risk v uncertainty

The Budget and macroeconomic policy • Two main macroeconomic policy ‘levers’ • Monetary policy – RBA’s inflation targeting regime • Inflation target range: 2-3 per cent per annum • RBA varies their cash rate target in response to actual v target inflation rates • RBA will look through ‘volatility’ – ‘headline’ vs ‘underlying’ inflation • Fiscal policy – changes in government’s budget settings • Main topic of discussion

Monetary policy • In Australia, the RBA has a ‘cash rate target’ • Cash rate is the interest rate charged on overnight loans between financial institutions – this varies with exchange settlement (ES) balances. ES balances are funds held with the RBA to settle obligations daily. The target is announced after each RBA Board meeting. • The next day, the RBA undertakes ‘open market operations’ – purchase and sale of securities such as government bonds – in order to keep the actual cash rate as close as possible to the target. This enables the RBA to have some influence over the levels of ES balances, which thereby affects the interest rate charged for overnight loans between financial institutions

Monetary policy • ‘Conventional’ monetary policy... • Many different interest rates in the economy – lending over varying time periods (term structure) and for different purposes • Cash rate is a very important (short-term) one that affects all others to some degree. • By varying the cash rate, the RBA varies the whole structure of interest rates in the economy – thereby exerting an indirect influence on borrowing and saving. Not an exact science! • There are also so-called ‘unconventional’ monetary policy methods – as this is a seminar on the budget/fiscal policy these need not concern us here.

Fiscal Policy • Government Budget settings – various instruments available • Digression - What is ‘government’? • Total public sector is comprised of: • General Government Sector (GGS) – this is the most commonly discussed sector • Public Non-Financial Corporations (PNFCs) • Public Financial Corporations (PFCs) • GGS + PNFCs sometimes referred to as ‘Non-Financial Public Sector’ or NFPS – Cash flow/operating statements and balance sheets for GGS, PNFCs and NFPS

Fiscal Policy – Instruments • Revenue measures (see BP#1, Statement 5) • Introducing, removing or altering various taxes • ‘Tax expenditures’ – summary only provided in the Budget – Tax Expenditures Statement (released in January of the next year) • Non-tax revenue changes • Various types of taxes • Discretionary (policy changes) vs cyclical (also referred to as ‘automatic stabilisers’) • Some revenue measures are designed with more than just macroeconomic goals in mind –designed to have an impact in some way on behaviour

Fiscal Policy – Instruments • Expenditure measures (see BP#1, Statement 6) • Various types of government expenditure – can be broadly categorised in different ways, depending on the context: • By function – education, health, defence, etc. • Discretionary vs cyclical • Administered vs departmental expenses – Richard Webb will have more to say about this distinction

Fiscal Policy – Instruments • Other measures • Contingent liabilities – e.g. government guarantees of deposits and wholesale funding – Some limited information available in BP#1, Statement 8 – Statement of Risks • Use of the Government Balance sheet - purchase or sale of financial and non-financial assets – Some limited information on the second is available in BP#1, Statement 9 – Budget Financial Statements

Fiscal policy - Effects • Concept of multipliers • Many considerations will impact on the effects of a particular action. Here are but a few: • Time frame under consideration – SR v LR • Exchange rate regime in place- fixed or floating • Openness to trade – exports + imports as % of GDP • Individual national action or synchronised global action • Type of action taken: • Expenditure measures – ‘Productive’ vs ‘unproductive’ government spending vs transfer payments • Revenue measures – Direct vs indirect taxation, differences in treatment across sectors, taxing wages vs capital vs natural resources • Don’t forget automatic stabilisers...

Economic Forecasting – Background • Macroeconomic forecasts form the basis around which the overall Budget is built • Tax revenues/receipts are closely linked to nominal GDP • Some significant expenses/payments are closely linked to real GDP and employment – especially unemployment benefits • Prices, wages, interest rates and exchange rates all affect various spending components • Economists cannot predict the future, but the government needs something upon which to estimate the evolution of budget variables into the future

Economic Forecasting – Background • Some common terminology: • Each budget is done on a financial year basis and contains estimates of economic and fiscal variables for the current year, the budget year, the next year and projections for the next two years • ‘Forward estimates’ period includes the budget year and three years ahead • Two major forecasting rounds – Budget (May) and MYEFO (around November) • Domestic Economy forecasts are presented in detail in BP #1 Statement 2, Economic Outlook

Economic Forecasting - Process Business liaison Release of latest National Accounts data International Economy Division – world outlook Domestic Economy Division – econometric modelling (single equation sectoral and economy-wide), leading indicators, other domestic data/forecasts Quality Assurance – Internal (senior management) and external (Joint Economic Forecasting Group)

Economic Forecasting – Budget cycle • Several documents released over the full Budget cycle • Budget papers #1-4 and Portfolio Budget Statements (May) • Final Budget Outcome (end-September) • MYEFO (November) • Charter of Budget Honesty requires a PEFO to be released prior to elections • Additional Budget documents can be released at the discretion of the Government (e.g. UEFO in Feb 2009; ES in Jul 2010) • Department of Finance and Deregulation also releases monthly budget statements

Economic Forecasting – risk vs uncertainty Forecasters necessarily have to deal with risk and uncertainty – difference between the two is whether the forecaster can identify the underlying probabilities of known possible set of outcomes or not. The former can be quantified whilst the second cannot Dealing with both risk and uncertainty involves the use of ‘sensitivity analysis’ For this reason, budget forecasts are unlikely to come to fruition exactly as predicted REMEMBER – Budget is merely a statement of the Government’s expectations NOT reality!

Economic Forecasting – sensitivity analysis • Sensitivity analysis is the use of alternative assumptions to establish how sensitive the predicted outcomes are to changes in assumptions. Scenarios encompass the budget year and the next year • BP#1 (Statement 3 Appendix A) usually contains two scenarios: • A permanent fall in non-rural commodity prices equivalent to a fall in nominal GDP of 1 per cent • A permanent rise in real GDP of 1 per cent, arising from an equal ongoing rise in both labour productivity and labour force participation • They show impacts on key economic variables and fiscal outcomes – deviation from baseline forecasts • They are ‘partial’ analyses rather than ‘general’, i.e. They do not include ‘feedbacks’, such as exchange rate movements or likely monetary/fiscal policy responses – see next slides

Economic Forecasting – feedbacks and other factors • In scenario 1, we would expect the following: • The exchange rate would fall, dampening the economic and fiscal effects, and • A temporary shock would have a more subdued impact than a permanent fall • In scenario 2, we would expect the following: • As above, a temporary shock would have a more subdued impact than a permanent fall, and • A larger relative contribution to real GDP increases from productivity rather than participation would mean a higher increase in wages and lower gain in employment growth. The reverse would also apply.

Economic Forecasting – sensitivity analysis • A couple of things to note: • Scenarios are broadly symmetric – that is, they apply (roughly) to moves in either direction • However- the effects are not likely to be linear. In other words , in the event of large changes (for example, a 5 per cent fall in nominal GDP – a five-fold increase in the first illustrative scenario), we should not expect that the predicted reactions will also be five times as large, even in the absence of any ‘feedbacks’. • In the event of large shocks, we should not expect the ceteris paribus assumption to hold – all else is rarely equal...

Final comments Cannot emphasise enough – Budget forecasts are not ‘reality’ and economic forecasters are not infallible There is much judgement applied in economic forecasting and policy analysis – assumptions have to be made about the future and these can and frequently do turn out to be wrong Quite often (but not always!) discussion about ‘black holes’ in budgets or ‘flawed’ costings revolves around differences of opinion about assumptions – the important thing is to make sure appropriate analytical techniques and sound logic are applied. It is perfectly valid to apply different judgements Criticisms of ‘inaccuracies’ (which are usually identified only with the benefit of hindsight) are valid only if an unsuitable analytical technique has been applied, logic is flawed or incomplete/incorrect data are used ex ante

Richard Webb • UNDERSTANDING: • PORTFOLIO BUDGET STATEMENTS (PBS)

Department of Resources, Energy and Tourism Budget Statements

Department of Resources, Energy and Tourism Resource Statement – Budget Estimates for 2010-11 as at Budget May 2010

Thank you for your attendance Contact Details: Garth 6277 2464 garth.day@aph.gov.au Scott 6277 2455 scott.kompo-harms@aph.gov.au Richard 6277 2460 richard.webb@aph.gov.au Upcoming Parliamentary Library Publication: The 2011-12 Budget Review Further information: www.budget.gov.au/