Download

1 / 46

480 likes | 879 Views

Profit Pools and Industry Analysis. James Oldroyd Kellogg Graduate School of Management Northwestern University J-oldroyd@northwestern.edu 801-422-7888 650 TNRB. THREAT OF ENTRY HIGH entrants have cost advantages low capital requirements little product differentiation

E N D

Profit Pools and Industry Analysis James Oldroyd Kellogg Graduate School of Management Northwestern University J-oldroyd@northwestern.edu 801-422-7888 650 TNRB

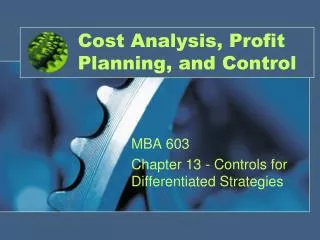

THREAT OF ENTRY • HIGH • entrants have cost advantages • low capital requirements • little product differentiation • deregulation of governmental barriers Example: Airlines • INDUSTRY COMPETITIVENESS • HIGH • many companies • little differentiation • excess capacity • high fixed/variable costs • cyclical demand BUYER POWER MEDIUM/HIGH Buyers extremely price sensitive Good access to information Low switching costs • SUPPLIER POWER • HIGH • strong labor unions • concentrated aircraft makers • THREAT OF SUBSTITUTES • MEDIUM • Autos/train for short distances Source: J. de la Torre

THREAT OF ENTRY • LOW • economies of scale • capital requirements for R&D and clinical trials • product differentiation • control of distribution channels • patent protection Example: Pharmaceuticals • INDUSTRY COMPETITIVENESS • LOW • high concentration • product differentiation • patent protection • steady demand growth • no cyclical fluctuations of demand BUYER POWER LOW Physician as buyer: Not price sensitive No bargaining power. (Changing with managed care.) SUPPLIER POWER LOW THREAT OF SUBSTITUTES LOW No substitutes. (Changing as managed care encourages generics.) Source: J. de la Torre

THE PC INDUSTRY’S PROFIT POOL 40% The value chain for the PC industry includes six key activities; the profitability of the activities varies widely. Manufacturers compete in the largest but least-profitable segment of the chain. 30 20 operating margin 10 0 100% 0 peripherals other components personal computers software microprocessors services Share of Industry Revenue source: Gadiesh and Gilbert, Harvard Business Review, May-June 1998

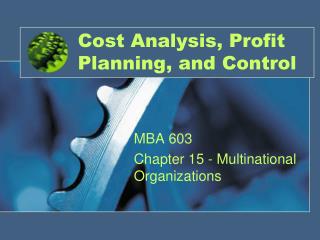

THE U.S. AUTO INDUSTRY’S PROFIT POOL 25% The automotive industry encompasses many value-chain activities. The way that profits and revenues are distributed among these activities varies greatly. The most profitable areas of the car business are not the ones that generate the biggest revenues. 20 15 operating margin 10 5 0 100% auto loans gasoline 0 new car dealers auto insurance service repair leasing used car dealers auto rental warranty auto manufacturing Share of Industry Revenue aftermarket parts source: Gadiesh and Gilbert, Harvard Business Review, May-June 1998

Profit Pools: Company Examples Companies Automakers U-Haul Elevators (OTIS) Iomega Polaroid Core Business Auto manufacturing Truck Rental Elevator Manufacturing Zip Drives Instant Photography Cameras Sources of Highest ROI Leasing, insurance, service. Packing materials, storage Service Zip Disks; Storage Film

The Challenges of Expanding Product or Service Offerings Why don’t firms simply offer the entire value chain to customers? What is a pool? How big is a pool?

Focus Product Leadership Faster Closer Customer Intimacy Operational Excellence Better Source: Adapted from Treacy and Wiersema, The Discipline of Market Leaders. Perseus Books. 1995

Product Leadership Customer Intimacy Operational Excellence The Claimed Focus

Product Leadership Faster Closer Customer Intimacy Operational Excellence Better The Reality 197 Operating Companies ? Source: Adapted from Treacy and Wiersema, The Discipline of Market Leaders. Perseus Books. 1995

Challenges – Overcoming Firm Legacy Polaroid 1948 First instant camera 1981 Formation of electronic group 1989 Polaroid capable of 1.9 m pixels vs. competitors 480k 1990 Research investments cut, lab sold to MIT, focus on marketing 1992 Prototype of digital camera ready 1996 Digital camera announced (already 40 competitors) 1998 Photo play category introduced $10 billion invested over 10 years Two new technologies: Stock falls from over $40 to .03 in 4 years Onxy monochrome digital images printed from mobile handheld devices Opal Color prints in 1 second vs. 40 seconds of current technology 1999 2000 2001 2002

Trade Off’s High Ability to Coordinate Activities Accountability Low Independent Integrated

The Added Cost of Coordination Newspaper-Broadcast-Interactive Sales Force Media Net Sales Force Makes a Sale Makes a Sale Tribune is double counting commissions Resulting in Twice the Sales Cost

Willingness to Pay Value Captured by Customer Price Value Captured by Firm Cost Value Captured by Supplier Supplier opportunity cost Problem of Aligning Perception The Customer’s Idea … 2+2=3 Your Idea… 2+2+5 Willingness to Pay Value Captured by Customer Price Value Captured by Firm Cost Value Captured by Supplier Supplier opportunity cost

Problem of Managerial Skills Broad understanding of the overarching business solution and the ability to perform consultative selling Moving From In- Depth to Breadth A B C D E In depth Knowledge about the specific product/ services

Advertising Agencies 23 Broadcast Stations Broadcast TMN Print Interactive Interactive Events Events Miss Match Alignment Challenges 11 Newspapers 2 Cable Channels

Channel Challenges Barrier 3 million independent sales representatives The Market J.C. Penney and other retail outlets

Channel Continued… Direct Approach via Ford.com and other online sites Barrier The Channel The Market The Corporation Ford Corporation Purchased Dealerships to give it direct customer access Source: 2001 Annual Report In 2002 “Ford is selling its Company-owned dealerships”

Channel Continued… The Market Brokers • Online access to account information • Account activity & balances • Portfolio holdings • Online access to Merrill Lynch research • Ability to e-mail with financial consultant • Online bill payment capabilities • Access to Merrill Lynch analytical tools • Ability to execute trades ml.com Merrill Lynch sought to involve brokers in the online process to minimize dissatisfaction Source: ml.com

Channel Continued… The Market The Travel Agent The Airlines The Solution Frequent Flier Programs

Economic Challenges It takes a substantial investment to: • identify the market • And Interpret the Market • Adapt to the Market

Product Dilemma What is the point of another flavor of toothpaste, another feature crammed into Microsoft Word, or another gizmo on the dash of a Ford minivan? We knew products had reached maturity when we introduced several new products and did not get the bump in market share we were used to getting Tom Kelly, GM of IDEO,as quoted in Business Week, 2001 Corporate Executive, 2002

Radical Innovation Profits over time Product Features 100% 80% 60% Focus Price 40% Product Service 20% Value Added Industry trend 0% Growth Consolidation Maturity Decline Product Parity Forces Firms into the Bottom Half of the Circle

Maturing Markets Strong High Profitability Position in the Supply Chain Typical Path Maturity Weak Low Extensive Limited Ability to Generate Value Enhancing Ideas

The Drive for Solutions • Product Parity New Delivery Vehicles Internet and aggregators Customer Needs are Changing

Dimensions of Value Top Line Value Product Differentiation Service Value Price Willingness to Pay Value Captured by Customer Bottom Line Value Price Value Captured by Firm Cost Value Captured by Supplier Supplier Opportunity Costs

THREE DISTINCT STRATEGIES TO BEAT THE COMMODITY TRAP Significant What you do Scope Extension 1 3 2 Limited Product Service Company focus Who you are

Cemex SEVERAL COMPANIES HAVE MADE THIS TRANSITION SUCCESSFULLY Significant GEMS Tribune Starbucks What you do Scope Extension 1 3 2 Cisco Limited Product Service Company focus Who you are

Taking the Turn ALTHOUGH VALUE CAN BE GENERATED BY MOVING TOWARDS SOLUTIONS OR CUSTOMERS A COMPLETE TURN ESSENTIAL TO SUSTAIN STRONG POSITION Significant GEMS Tribune Cemex Starbucks What you do Scope Extension 1 3 2 Cisco Limited Product Service Company focus Who you are

GEMS CHANGING SCOPE AND THEN COMPANY FOCUS Introduction Market leader in diagnostic imaging with over 40% market share Grew in the 90s through acquisitions Scope extension ideas Slowly moving pure equipment sales to financial and consulting services Education of customers (TIP TV) Quality and Productivity programs Changing company focus Use of Field Engineers not only as technical experts but onsite customer relationship developers Change organization focus to allow dedicated resource focusing on customer service Significant Scope Extension Limited Product Service Company focus "Becoming better than the best through a boundaryless corporation"

STARBUCKS CHANGING FOCUS AND THEN SCOPE • Introduction • Gourmet coffee reseller focusing on creating "Starbucks culture" • current market cap $1.6bn • Changing company focus • Built strong brand recognition through distinct culture building exercise • Created "customers as partners" philosophy • Joint branding and licensing agreements exercise creating faster product recognition • Starbucks/Pepsi frappuccino, Starbucks/Dreyers ice cream • Scope extension ideas • Extending service offering to include new products • gourmet lunches, Tazo teas, music • Established strong partnerships allowing access to alternate mediums of sale • partnership with United Airlines, Barnes & Noble, Craft Significant Scope Extension Limited Product Service Company focus "Creating a new customer culture, providing a suite of solutions "

CISCO CHANGING FOCUS AND THEN SCOPE • Introduction • Large networking solutions provider • Exponential growth through acquisition strategy • underlying growth philosophy is new product ideas • through acquisitions, partnerships, external; R&D • acquisition focused on small companies with customer • focus • Changing company focus • Acquisition focus on companies controlling customer intimacy rather than companies with technology capabilities • Worked with customers to tailor make networks • Customer advocacy cornerstone of culture • customer satisfaction based compensation • Moving from segment focus business model to product focus • Scope extension ideas • Moved from router only company to end to end networking solutions Significant Scope Extension Limited Product Service Company focus "Customer Advocacy is the company agenda "

CEMEX A COMPANY THAT PURSUED THE HYBRID APPROACH • Introduction • Cemex started as a Mexican cement company and is today the • 3rd largest cement producer in the world • vertically integrated into distribution of construction materials • largest steel and cement transporter in Mexico • Scope extension ideas • Broader product categories • cement cement + cement derivatives + construction materials • Extensive client support programs including • product education, delivery speed, inventory management, financing of project, infrastructure cost sharing • Reconfiguration of sales channel • introduction of Arkio, online/offline sales channel • introduction of Promexma program, own distribution centers • Changing company focus • Changed performance metrics to reward on customer satisfaction • Leveraging IT and internet capabilities to get closer to customers Significant Scope Extension Limited Product Service Company focus "Generating returns by providing comprehensive construction solutions to targeted customers"

What is a Solution? 63% of Fortune 100 Firms claim to offer solutions. Finally • Co-created value add • Integrated Offering • Creates some risk • Requires intimate customer knowledge • Is completely customized First Steps • Product Extension • Service Extension • Philosophical Extension Purchase Experience Product Needs Customer Guest Solution helps customers succeed in the marketplace by enhancing revenues, reducing current or future costs. Source: Adapted from “From Solutions to Symbiosis” Sharma, Lucier, and Molloy. Strategy and Business, 2002

100% 100% = 7 = 7 90% 90% 80% 80% 79% of all 70% 70% companies = 6 = 6 Percentage of Responses Percentage of Responses 60% 60% responded 50% 50% 5 ³ 40% 40% = 5 = 5 30% 30% 20% 20% = 4 = 4 10% 10% <= 3 <= 3 0% 0% Scale: 1 = Decreasing 4 = Not Changing 7 = Increasing Scale: 1 = Decreasing 4 = Not Changing 7 = Increasing The Proliferation of Solutions Change in shift from selling products/services Change in shift from selling products/services to selling value to selling value - - added solutions added solutions

Willingness to Pay Value Captured by Customer Price Value Captured by Firm Cost Value Captured by Supplier Supplier opportunity cost Challenges of Providing a Solution Solution must increase the Willingness to Pay and the price or decrease the cost to Serve to add value to the firm • Some Common Pitfalls • Firm provides more product features or services (solution) but customers are unwilling to pay for the features or additional services • Firm is unable to quantify the value added and thus is not remunerated for the effort • Customer requirements vary resulting in the need for an infinitely flexible system • Solution is not scalable • Firm is unwilling to bear higher initial cost necessary to create a solution

Challenges of Pricing a Solution Number of new systems users and frequency of use User fees and access fees Revenue from new systems + Fees + + Add on product fees and service Revenue with new systems Revenue from old systems + Revenue from related products and services Marginal Revenue - The Key is to generate new revenue or be able to charge a premium for the additional service +/- Customer Value of Solutions Offered Revenue from old system Marginal Cost Revenue without new systems + Revenue from related products and services +/- Marginal Investment Source: McKinsey Quarterly Putting a Price on Solutions, 2001, Number 3.

Vs. Vs. Vs. Vs. Challenges of Selling Solutions Product Selling Consultative Selling Product Performance Customer Performance Intra Organizational Coordination Inter Organizational Coordination Only Product Risk Performance Risk

Product vs. Service Content Delivery Traffic Server Sales a software solution for around $25,000 plus the required hardware Benefits: Easy to sell. Low upfront costs. Benefits: Software is easy to scale. Costs are fixed. Problems: Capital expenditures and risks are fully shouldered by Akamai - Model is difficult to Scale Problems: Huge upfront costs. Key Customer: AOL Key Customer: Yahoo!

Mega Aggregators- A serious attempt Offers the Physician one software, hardware and support to allow an office to move all records to electronic format. Scheduling Reporting Insurance Reimbursement Electronic Charting Electronic Prescription Compliance Co-pay

Industry Analysis Porter’s Five Forces Model Threat of New Entrants Bargaining Power of Suppliers Rivalry among Existing Competitors Bargaining Power of Buyers Threat of Substitutes

Additional Industry Analysis Tools • SWOT Analysis: Numerous Environmental Opportunities Overcome Weaknesses Grow Substantial Internal Strengths Critical Internal Weaknesses Restructure Diversify Major Environmental Threats

THE U.S. AUTO INDUSTRY’S PROFIT POOL 25% The automotive industry encompasses many value-chain activities. The way that profits and revenues are distributed among these activities varies greatly. The most profitable areas of the car business are not the ones that generate the biggest revenues. 20 15 operating margin 10 5 0 100% auto loans gasoline 0 new car dealers auto insurance service repair leasing used car dealers auto rental warranty auto manufacturing Share of Industry Revenue aftermarket parts source: Gadiesh and Gilbert, Harvard Business Review, May-June 1998