Download

1 / 25

250 likes | 301 Views

In 2013, the CFPB issued new rules under Regulations X and Z to enhance borrower rights, prevent foreclosures, and improve lender practices. Explore how outdated systems affect foreclosure outcomes, and learn about the new regulations impacting successors in interest. Discover how servicers are prevented from proceeding with foreclosure until complying with loss mitigation procedures. File complaints for investigations, request examinations, and check enforcement actions on the official CFPB website. Understand the importance of monthly statements in accordance with Reg Z 12 CFR 1026.41 for clear communication between servicers and consumers. Stay informed about the latest CFPB developments to protect your rights as a borrower.

E N D

Navigating CFPB Mortgage Servicing The CFPB Rules Affecting Foreclosure Nick C Thompson

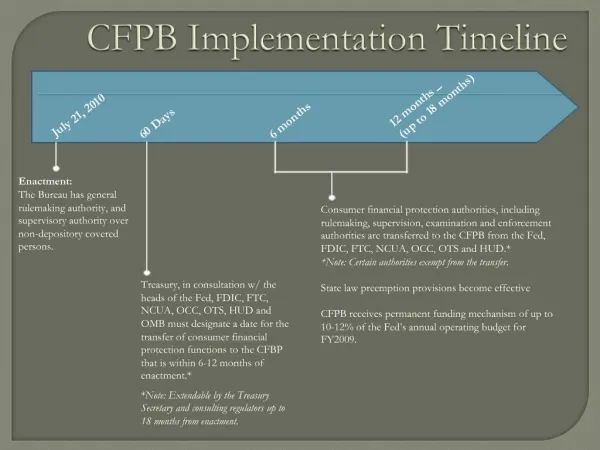

Link to the latest 1024 and 1026 regulations • In 2013 the CFPB issued new rules governing mortgages and foreclosures under Regulations X and Z. These rules were issued Jan 17th 2013 published Feb 14 2013 and became effective Jan 10th 2014. Several additional rules became effective on 10-2015. For the most current updates see the CFPB version at this link showing the date sections became effective. http://www.consumerfinance.gov/eregulations/1024-1/2015-18239#1024-1 .

The important CFPB sections 1024 and 1026 • The important CFR sections are 12 CFR 1024 (regulation x) and 1026 (regulation z). These rules strongly enhance the rights of borrowers and improve information to the borrowers, prevent foreclosures and define reasonable efforts on the part of lenders to prevent foreclosures. A June 22nd 2016 a press release from the CFPB confirmed a long known fact that a major cause of these errors and practices is faulty systems and outdated software used by lenders and servicers. This press release states outdated systems are an excuse and not a reason for these errors. Outdated software often causes foreclosures or delinquency to the benefit of servicers who profit from and bill for delinquency.

Developing CFPB the successor in interest • A major new development has been the developing trend to create protections for successors in interest. Until now only borrowers have had most of the protection from foreclosures. Persons who inherit property or obtain property pursuant to a divorce order had no status as a borrower and few if any rights. This forced these persons to file bankruptcy where in a Chapter 13 their interest in the property had a chance of being protected by catching up the mortgage for a widow or ex spouse who now owned the property. The CFPB has been developing and working on rights for these persons but regulations will not become effective until a year after the publication of these rights.

Servicer prevented from foreclosure The Major section of importance for foreclosure defense is the compliance section 12 §1024. 41 (a) regulating loss mitigation procedures. 12 §1024. 41 (a) fails to create a private right of action. Instead the Servicer is prevented from proceeding with a foreclosure proceeding until a lender follows all these procedures. It states: • Nothing in 12 § 1024.41 should be construed to create a right for a borrower to enforce the terms of any agreement between a servicer and the owner or assignee of a mortgage loan, including with respect to the evaluation for, or offer of, any loss mitigation option or to eliminate any such right that may exist pursuant to applicable law.

Filing a Complaint, Examinations • The CFPB investigates and regulates the industry along with performing examinations. Complaints requesting an investigation can be filed at http://www.consumerfinance.gov/complaint/. • Complaints may trigger examinations or enforcement actions. • The results of enforcement actions are published and circulated. http://www.consumerfinance.gov/privacy/system-records-notices/enforcement-database/ • Complaints may be filed for student loan, collection agendy or mortgage cases. Often after a complaint is filed the lender files are reviewed by the lender for problems and errors. (Scrubbing)

2016 Examination sections mirror recent regs • Module 1 Servicing Transfers, Loan Ownership Transfers, and Escrow Disclosures • Module 2 Payment Processing and Account Maintenance • Module 3 Consumer Inquiries, Complaints, and Error Resolution Procedures • Module 4 Maintenance of Escrow Accounts and Insurance Products • Module 5 Credit Reporting • Module 6 Information Sharing and Privacy, Default Servicing • Module 7 Collections and Accounts in Bankruptcy • Module 8 Loss Mitigation, Early Intervention, and Continuity of Contact for Foreclosure • Module 9 Foreclosures • Module 10 Examiner Conclusions and Wrap-Up

Clear Monthly Statements Reg Z 12 CFR 1026.41 • This section requires monthly statements and what must be included. Monthly statements from servicers must include the amount due, the breakdown of the payments, any recent transaction activity, next payment date, and a summary of the mortgage terms. • 1026.41(a)(2) Periodic Statements. • (2) Periodic statements. A servicer of a transaction subject to this section shall provide the consumer, for each billing cycle, a periodic statement meeting the requirements of paragraphs (b), (c), and (d) of this section. If a mortgage loan has a billing cycle shorter than a period of 31 days (for example, a bi-weekly billing cycle), a periodic statement covering an entire month may be used. For the purposes of this section, servicer includes the creditor, assignee, or servicer, as applicable. A creditor or assignee that does not currently own the mortgage loan or the mortgage servicing rights is not subject to the requirement in this section to provide a periodic statement.

Payments Promptly Credited Reg. Z 12 C.F.R. § 1026.36(c)(1)(i) A Servicer must credit a borrower’s account the date the payment is received under Reg. Z, 12 C.F.R. § 1026.36(c)(1)(i) [§ 226.36(c)(1)(i)]; and Frank Dodd 11 15 U.S.C. § 1639f. If servicers place partial payments in a suspense account, then the payment must be credited to the borrower’s account once the suspense account equals one full payment. • 1026.36(c)(1)(i) Periodic payments. No servicer shall fail to credit a periodic payment to the consumer's loan account as of the date of receipt, except when a delay in crediting does not result in any charge to the consumer or in the reporting of negative information to a consumer reporting agency, or except as provided in paragraph (c)(1)(iii) of this section. A periodic payment, as used in this paragraph (c), is an amount sufficient to cover principal, interest, and escrow (if applicable) for a given billing cycle. A payment qualifies as a periodic payment even if it does not include amounts required to cover late fees, other fees, or non-escrow payments a servicer has advanced on a consumer's behalf.

Early notice of Delinquency by Live and Written Contact 12 § 1024.39(a) • A monthly statement must contain information about any delinquency when the account becomes 36 days delinquent. This information must include the date the account became delinquent, the amount to bring the loan current, and the consequences. The servicer is exempt from this section however if the borrower is in bankruptcy or has sent notice under FDCPA section 805(c) (15 U.S.C. 1692c(c). • 1024.39(a) Live Contact.Live contact. A servicer shall establish or make good faith efforts to establish live contact with a delinquent borrower not later than the 36th day of the borrower's delinquency and, promptly after establishing live contact, inform such borrower about the availability of loss mitigation options if appropriate. • Except as otherwise provided in this section, a servicer shall provide to a delinquent borrower a written notice with the information set forth in paragraph (b)(2) of this section not later than the 45th day of the borrower's delinquency. A servicer is not required to provide the written notice more than once during any 180-day period”

Notice of Foreclosure Alternatives 12 § 1024.39 (b) Servicers shall contact a delinquent borrower with a written notice no later than 45 days after delinquency but not more than once within 180 days to include foreclosure options. • WRITTEN NOTICE REQUIRED. Except as otherwise provided in this section, a servicer shall provide to a delinquent borrower a written notice with the information set forth in paragraph (b)(2) of this section not later than the 45th day of the borrower's delinquency. A servicer is not required to provide the written notice more than once during any 180-day period. • CONTENT OF THE WRITTEN NOTICE. The notice required by paragraph (b)(1) of this section shall include: • A statement encouraging the borrower to contact the servicer; • The telephone number to access servicer personnel assigned pursuant to § 1024.40(a) and the servicer's mailing address; • If applicable, a statement providing a brief description of examples of loss mitigation options that may be available from the servicer; • If applicable, either application instructions or a statement informing the borrower how to obtain more information about loss mitigation options from the servicer; and • The Web site to access either the Bureau list or the HUD list of homeownership counselors or counseling organizations, and the HUD toll-free telephone number to access homeownership counselors or counseling organizations.

§ 1024.40 Continuity of Contact • A mortgage servicer must implement policies and procedures to ensure borrowers have Continuity of Contact. In the past a gatekeeper would take the mortgage modification application and then it would go to underwriting. Often the person taking the application would lose records or fail to maintain the records. This may have been due to how the process was structured. The system is very similar to Mortgage Broker or a Mortgage Banker’s application. • The servicer is responsible for having dedicated personnel to assist borrowers in loss mitigation options to avoid foreclosures. Sometimes referred to as direct, easy, and ongoing access to the employees responsible to assist avoiding foreclosure. The continuity of contact personnel must be able to readily access a borrower’s mortgage loan information necessary to move along the loan modification and the application status along with the account information such as the amount of the delinquency. This contact must adequately communicate information to the borrower.

12 § 1024.40 Continuity of contact. § a • In general. A servicer shall maintain policies and procedures that are reasonably designed to achieve the following objectives: • Assign personnel to a delinquent borrower by the time the servicer provides the borrower with the written notice required by § 1024.39(b), but in any event, not later than the 45th day of the borrower's delinquency. • Make available to a delinquent borrower, via telephone, personnel assigned to the borrower as described in paragraph (a)(1) of this section to respond to the borrower's inquiries, and as applicable, assist the borrower with available loss mitigation options until the borrower has made, without incurring a late charge, two consecutive mortgage payments in accordance with the terms of a permanent loss mitigation agreement. • If a borrower contacts the personnel assigned to the borrower as described in paragraph (a)(1) of this section and does not immediately receive a live response from such personnel, ensure that the servicer can provide a live response in a timely manner

12 § 1024.40 Continuity of contact. § b • Functions of servicer personnel. A servicer shall maintain policies and procedures reasonably designed to ensure that servicer personnel assigned to a delinquent borrower as described in paragraph (a) of this section perform the following functions: • Provide the borrower with accurate information about: • Loss mitigation options available to the borrower from the owner or assignee of the borrower's mortgage loan; • Actions the borrower must take to be evaluated for loss mitigation options, including actions the borrower must take to submit a complete loss mitigation application, as defined in § 1024.41, and, if applicable, actions the borrower must take to appeal the servicer's determination to deny a borrower's loss mitigation application for any trial or permanent loan modification program offered by the servicer; • The status of any loss mitigation application that the borrower has submitted to the servicer; • The circumstances under which the servicer may make a referral to foreclosure; and • Applicable loss mitigation deadlines established by an owner or assignee of the borrower's mortgage loan or § 1024.41.

12 § 1024.40 Continuity of contact. § b Retrieve, in a timely manner: • A complete record of the borrower's payment history; and • All written information the borrower has provided to the servicer, and if applicable, to prior servicers, in connection with a loss mitigation application; • Provide the documents and information identified in paragraph (b)(2) of this section to other persons required to evaluate a borrower for loss mitigation options made available by the servicer, if applicable; and • Provide a delinquent borrower with information about the procedures for submitting a notice of error pursuant to § 1024.35 or an information request pursuant to § 1024.36.

Applications for Mortgage Modification and Foreclosure Avoidance §1024.41 (c) and (d) • A borrower only has to submit one application for all of the available loss mitigation and foreclosure avoidance options. Servicers have to consider such applications for all the foreclosure avoidance options at the time of receipt. Servicers have to acknowledge receipt of the application within 5 days and they have 30 days to consider and respond to the application. • Under 1024.41 (d) Debtors are allowed to appeal decisions. A servicer is required to include the specific reasons for any denial. A general denial is not a proper denial and the options for appeal must be in the denial. The debtor has 90 days to appeal. Incomplete applications are not a basis for denial see 41 (c) (2) (iv) unless the borrower fails to respond to requests for additional information.

§ 1024.41 Fair Review Process § (a) through (e) • Servicers must establish procedures to ensure borrowers receive a fair review and evaluation for all loss mitigation options permitted by the investor for which the borrower may be eligible. In the process of the modification the servicer is prohibited from steering the borrower into a more profitable loan. • (b)(1) COMPLETE LOSS MITIGATION APPLICATION. A complete loss mitigation application means an application which a servicer receives with all the information that the servicer requires from a borrower in evaluating an application for loss mitigation options available to the borrower. A servicer shall exercise reasonable diligence in obtaining documents and information to complete a loss mitigation application.

Restrictions on Dual Tracking §1024.41(f) and §1024.41(g) Right to Appeal 1024.41(h) • The problem with dual tracking has been that many of the defenses available to the borrower can be time sensitive. While the borrower is working with the lender he is often told to delay filing an answer with complete defenses. Further it is difficult or impossible for the borrower to fund litigation and a foreclosure defense while making trial mortgage payments. Dual dual-tracking is when a mortgage loan servicer simultaneously forecloses while working with the borrower to avoid the foreclosure. Servicers are prohibited from filing a foreclosure until the mortgage loan is at least 120 days delinquent or while a mortgage modification or other application is pending

12 § 1026.20 (c) Interest Rate Adjustments for ARMS sections 12 §1026.20 (d)(2)(ix) through (xi) • Servicers must provide a disclosure before the first interest rate adjustment if the adjustment ends up with a change in the payment. The change must include an explanation of how and why the new payment was calculated when it takes effect and any alternatives if the new payment is unaffordable along with providing access to housing counselors. The protections are under sections 12 §1026.20 (d)(2)(ix), 12 §1026.20 (d)(2)(x) and 12 §1026.20 (d)(2)(xi).

Borrower’s Option to Avoid Forced Placed Insurance 12 CFR 1024.37 (c) • When a servicer wishes to obtain insurance at the cost of the borrower the servicer must first afford the borrower the option to obtain the insurance. The servicer must give the borrower two notices the first notice must be at least 45 days before the first charge to the borrower and the second at least 15 days before the charge. The notice must be in bold text. The second notice must include a good faith estimate of the costs. The servicer must cancel its insurance policy within 15 days of the receipt a notice that the borrower has obtained insurance which must include proof of insuranceRequirements before charging borrower for force-placed insurance. • Before a servicer assesses on a borrower any premium charge or fee related to force-placed insurance, the servicer must: • Deliver to a borrower or place in the mail a written notice containing the information required by paragraph(c)(2) of this section at least 45 days before a servicer assesses on a borrower such charge or fee;

Promptly Correct Errors and Provide Information 1024.35(e); 1024.36 and 1024.38(b) (4) (ii) • Servicers must acknowledge and respond to written notices from the borrower with respect to errors or requests for information. The servicer acknowledgement must be in writing and within seven days. Information requests and errors should generally be resolved within 30-45 days and a written response should be sent to the borrower. • The some of the specific errors are numerated under 1024.35 (b)

Record Retention 1024.38 (c) 1 A Servicer must retain the borrower’s records until one year after a loan is paid or transferred. Servicers must implement policies and procedures to ensure records are accurate and readily available. • RECORD RETENTION. A servicer shall retain records that document actions taken with respect to a borrower's mortgage loan account until one year after the date a mortgage loan is discharged or servicing of a mortgage loan is transferred by the servicer to a transferee servicer.

Servicing File Record Retention 1024.38 (c) 1 A Servicer must retain the borrower’s records until one year after a loan is paid or transferred. Servicers must implement policies and procedures to ensure records are accurate and readily available. • 2 SERVICING FILE. A servicer shall maintain the following documents and data on each mortgage loan account serviced by the servicer in a manner that facilitates compiling such documents and data into a servicing file within five days: • A schedule of all transactions credited or debited to the mortgage loan account, including any escrow account as defined in § 1024.17(b) and any suspense account; • A copy of the security instrument that establishes the lien securing the mortgage loan; • Any notes created by servicer personnel reflecting communications with the borrower about the mortgage loan account; • To the extent applicable, a report of the data fields relating to the borrower's mortgage loan account created by the servicer's electronic systems in connection with servicing practices; and • Copies of any information or documents provided by the borrower to the servicer in accordance with the procedures set forth in § 1024.35 or § 1024.41.

Small Servicer Exemptions from Foreclosure Avoidance & Forced Placed Insurance Sections • Two important exemptions exist for small servicers under 1024.17(k) for Forced placed insurance and under § 1024.41 (j) for the Foreclosure avoidance sections. • 1024.41(j)A small servicer shall be subject to the prohibition on foreclosure referral in paragraph (f)(1) of this section. A small servicer shall not make the first notice or filing required by applicable law for any judicial or non-judicial foreclosure process and shall not move for foreclosure judgment or order of sale, or conduct a foreclosure sale, if a borrower is performing pursuant to the terms of an agreement on a loss mitigation option. • §1024.17(k)(5)(ii)(B)Notwithstanding paragraphs (k)(5)(i) and (k)(5)(ii)(B) of this section and subject to the requirements in § 1024.37, a servicer that qualifies as a small servicer pursuant to 12 CFR 1026.41(e)(4) may purchase force-placed insurance and charge the cost of that insurance to the borrower if the cost to the borrower of the force is less than the amount the small servicer would need to disburse from the borrower’s escrow account to ensure that the borrower’s hazard insurance premium charges were paid in a timely manner.

Nick Thompson • Nick C Thompson • 800 Stone Creek Parkway Suite 6 Louisville KY 40223 • 502-625-0905 Fax 502-625-0940 • Office@Bankruptcy-Divorce.com • For additional information on Bankruptcy and Foreclosure including articles on income tax or student loans and bankruptcy see our website at www.Bankruptcy-Divorce.com