Download

1 / 21

400 likes | 1.23k Views

The Loanable Funds theory. We use the term “loanable funds market” to describe the arrangements and institutions by which saving of households is made available to borrowers. Factor income. Leakages must be recycled if total spending is to match full-employment GDP.

E N D

The Loanable Funds theory We use the term “loanable funds market” to describe the arrangements and institutions by which saving of households is made available to borrowers.

Factor income • Leakages must be recycled if total spending is to match full-employment GDP. • According to the Classical theory, the loanable funds market acts as a conduit to transfer spending power (S) from households to borrowing units (firms and government units). • Saving (S) is the “source” of loanable funds. Consumption Net taxes Saving

Why do households save? ? • To have a more secure future, to start a business, to finance a child’s education, to satisfy miserliness, . . . • To earn interest. We view interest as the “reward for saving” or the “reward for postponing gratification.”

The opportunity cost of spending now (measured in lost future spending) is positively related to the interest rate. Value of $1,000 in 3 years at alternative interest rates

Supply of Funds Saving = Supply of Funds Interest rate 5% 3% 0 1.5 1.75 Trillions of Dollars

Why do firms borrow? • To finance the acquisition of long-lived capital goods. • The rate of interest is the cost of borrowing or the price of loanable funds. • The investment demand curve indicates the level of investment spending at various interest rates. • As the interest rate decreases, more investment projects become attractive in the assessment of business decision-makers—hence, the investment demand function is downward-sloping with respect to the interest rate.

Demand for Funds by Business When the interest rate falls, investment spending and the business borrowing needed to finance it rises. Interest rate A 5% B 3% Investment Demand 0 1.5 1.0 Trillions of Dollars

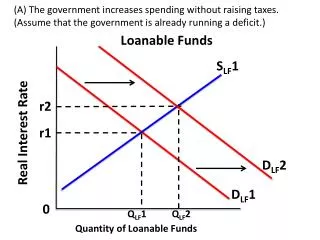

Public sector borrowing • Let G denote public sector (or government) spending for goods and services in a year • T is net tax receipts in a year. • If G is greater than T, the the public sector has a budget deficit equal to G – T. • If T is greater than G, then the public sector has a surplus equal to T – G. • If the public sector has a budget deficit, it must borrow.

Federal Government Budget Surplus (Deficit) in billions , 1955-2000 www.economagic.com

Public Sector Borrowing in Classica G = $2 trillionT = $1.25 trillionTherefore, Budget Deficit = G – T = $2 trillion - $1.25 trillion = $0.75 trillion Government Demand for Funds 5% B Interest Rate 3% A 0 0.75 Trillions of Dollars

Total Demand for Funds Interest Rate 5% 3% 0 1.75 2.25 Trillions of Dollars

Loanable Funds Market Equilibrium Total Supply of Funds (Saving) Interest Rate 5% E Total Demand for Funds (Investment + Deficit) 0 1.75 Trillions of Dollars

Why does the loanable funds theory guarantee the validity of Say’s law? S = IP + G - T Quantity of Funds Supplied Quantity of Funds Demanded Now, rearrange the equation above by bringing T to the left side: S + T = IP + G Injections Leakages

So long as the loanable funds market “clears,” leakages (Saving) will be offset to injections (investment and government spending).

Income ($7 Trillion) Income ($7 Trillion) Households Consumption ($4 Trillion) Saving ($1.75 Trillion) Loanable Funds Markets Net Taxes ($1.25 Trillion) Government Spending ($2 Trillion) Deficit ($0.75 Trillion Government Resource Markets GoodsMarkets Investment ($1 Trillion) Firm Revenues ($7 Trillion) Firms Factor Payments ($7 Trillion)

Fiscal Policy Changes in government spending, transfer payments, and taxes designed to change total spending in the economy and thereby influence total output and employment.

The Classical view of Fiscal policy Friends, we believe that fiscal policy is unnecessary and ineffective. The economy is doing just fine without meddling by Washington.

Crowding Out • Crowding out is the idea that an increase in one component of spending will cause a decrease in other spending components. • An increase in G may cause a decrease in C, IP, or both—that is, government spending may “crowd out” private spending.

Crowding Out With an Initial Budget Deficit Total Supply of Funds (Saving) B • Increase in G = AH • Decrease in C = AC • Decrease in IP = CH 7% A C Interest Rate H 5% D2 = IP + G2 - T D1 = IP + G1 - T 0 1.75 2.05 2.25 Trillions of Dollars

Effects of a Reduction in the Government Surplus S2 = Savings + T – G2 S1 = Savings + T – G1 Interest Rate B 7% H C A 5% D = Investment 0 1.25 1.55 1.75 Trillions of Dollars