Download

1 / 123

1.89k likes | 3.85k Views

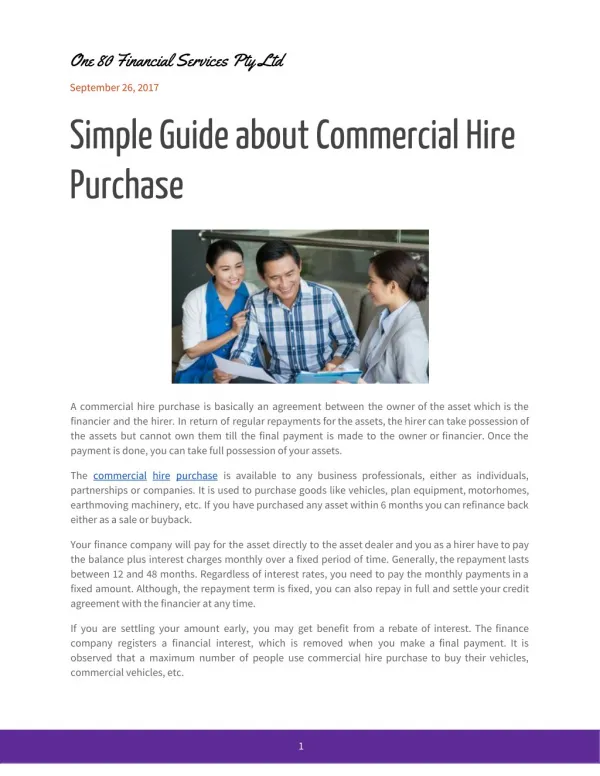

Hire Purchase Accounts. Hire Purchase. Hire Purchase (HP) is one of the payment methods of which the buyer use the goods without immediate full settlement of the price of the goods. With Hire Purchase Agreement. The HP selling price includes normal Cash Price PLUS HP Interest

E N D

Hire Purchase • Hire Purchase (HP) is one of the payment methods of which the buyer use the goods without immediate full settlement of the price of the goods

With Hire Purchase Agreement • The HP selling price includes normal Cash Price PLUS HP Interest • The seller agreed that the buyer could hire the goods by payments of ‘deposit’ and ‘instalments’

Hire Purchase Price = Cash Price + Total Hire Purchase Interest OR Outstanding Balance (including HP interest paid by instalments = Deposit (Down payment) +

Calculation of Hire Purchase Interest Straight line method Actuarial Method Sum-of-digits Method

Straight Line Method(Equal apportionment) • Interest is apportioned evenly over the number of installments agreed upon. HP Interest per instalment = Total HP Interest Number of total instalments

Example 1 • An asset is acquired on the following terms: • Cash price $9000 • Down payment $1000 • HP Price $12200 • Nominal rate of interest 10% • Four annual instalments $2800

Answer: Total HP interest = $12000-$9000 =$3200 HP interest payable per annum = $3200/4 = $800 OR An alternative way to calculate hire purchase interest ($9000-$1000)*10% = $800 Year HP interest Capital Instalments $ $ $ 1 2 3 4 + = 2800 2800 2800 2800 2000 2000 2000 2000 800 800 800 800

B. Actuarial Method • Interest is charged on the outstanding balance of the cash price after the down payment is made. • Equal instalments • Unequal instalment

1 Equal instalment Equal instament = HP price – Down payment No. of instalment • Example 2 • An asset is acquired on the following terms: • Cash price $9000 • Down payment $1000 • HP price $11096 • Interest 10% on outstanding balance • Four annual instalment $2524 (11096-1000)/4

Year HP interest Capital Instalments $ $ $ 1 2 3 4 6276 (9000-1000)*10% =800 1724 2524 2524 2524 2524 (8000+800-2524)*10%=628 1896 (6276+628-2524)*10%=438 2086 (4380+438-2524)*10%=230 2294 10096 8000 2096 4380

Unequal instalment Unequal instalment=Cash price-Down payment+Interest accrued No. of instalment (i.e.unpaid interest) • Example 3 • An asset is acquired on the following terms: • Cash price $9000 • Down payment $1000 • HP price $11000 • Interest 10% on outstanding balance • Four annual instament $2000+interest

Year HP interest Capital Instalments $ $ $ 1 2 3 4 6000 (9000-1000)*10% =800 2800 2000 2000 2000 2000 2600 (8000+800-2800)*10%=600 2400 (6000+600-2600)*10%=400 2200 (4000+400-2400)*10%=200 10000 8000 2000 4000

C. Sum of Digits Method • The HP interest is apportioned according to the digit assigned (descending order) • Using this method, more interest is charged in the earlier periods, less interest is charged in the later periods.

When n = number of instalments Sum of digits = n(n+1) 2 HP interest per instalment = Total HP interest* Digit assigned in the instalment Sum-of-digits of total instalment

Example 4 • A motor vehicle was purchased under a hire purchase agreement • Cash price $10000 • Hire Purchase $13600 • Instalments 4 months • Date of sale 1 October 1996 • Calculate the interest under each of the three cases: • (a) First instalment due at the end of month from the date of sale • (b) First instalment due at the beginning of month following the date of sale • (c) First instalment due at the date of sale.

Total HP interest =$13600-$10000=$3600 Sum of digit= 4*(4+1)/2=10 Case (a) and (b) Interest paid 1st instalment $3600*4/10=$1440 2nd instalment $3600*3/10=$1080 3rd instalment $3600*2/10=$720 4th instalment $3600*1/10=$360

Total HP interest =$13600-$10000=$3600 Sum of digit= 3*(3+1)/2=6 Case ( C ) Interest paid 1st instalment $3600*3/6=$1800 2nd instalment $3600*2/6=$1200 3rd instalment $3600*1/6=$600 4th instalment -

Hire Purchase Buyer Seller Assets account Hire purchase creditors account Hire purchase interest account Hire purchase interest suspense account Hire purchase sales Provision for unrealized profit Hire purchase debtors account Concept Chart

Acquisition of Assets on Hire Purchase • When an asset is acquired on hire purchase, there are 2 ways to account for this in the purchaser’s books. • Progress interest charge system • Interest Suspense Method • They differ mainly in the way they record hire purchase interest.

2 Method of HP Interest • Treatment • Progress interest charge system • Interest suspense method * • 3 method of HP Interest • Apportionment • Straight-line method • Actuarial method • Sum-of-digit method = 6 Version

Progress interest charge system • Interest is charged upon each instalment.

Notes : • Cut off of the financial period should be aware in order to • calculate the total hire purchase interest of the financial period • to be reflected in the P/L account as an ‘expense’ item • Each financial year may include up to 12 monthly instalment, • 4 quarterly instalment or 2 half-yearly instalment

Balance Sheet Presentation • For instance: after 1st instalment Paid • Progress interest charge system: Balance Sheet ( Instalment for 1st year) $ Current Liabilities HP Creditor (Instalment for 2nd year) X Instalment for 2nd year – Interest payable for 2nd year Long term Liabilities HP Creditor (Instalment for 3rd year and so on) X Outstanding HP creditor – HP creditor on current liabilities

For instance: after 1st instalment Paid • Interest Suspense Method: Balance Sheet ( Instalment for 1st year) $ Current Liabilities HP Creditor (Instalment for 2nd year) X Less HP interest suspense (X) Interest payable for 2nd year X Outstanding HP creditor – Instalment for next year Long term Liabilities HP Creditor (Instalment for 3rd year and so on) X Less HP interest suspense (X) Outstanding interest suspense – interest Payable for 2nd year X

Example Refer to textbook P.24

Example 6 • ABC Ltd. purchased a vehicle from Grace Ltd. on 1 Jan 1996 on HP agreement. The details were as follows • Cash price $9000 • Down payment $1000 • HP Price $11096 • Nominal rate of interest 10% on outstanding balance • Four equal annual instalments • First due 31 Dec 1996 • Depreciation 10% on cost • Using (a) the progress interest charge system and (b) interest suspense method, show transactions in books of ABC Ltd.

Answer (a): Total HP interest= HP price – Cash Price = 11096 – 9000 = 2096 Equal instalments = (11096 –1000)/4 =2524

Hire purchase Creditor (Grace Ltd) 1/1/96 Bank-deposit 1,000 1/1/96 Vehicle 9,000 31/12 Bank-instalment 2,524 31/12 HP Interest 800 (9000-1000)*10% 31/12 Balance c/d 6,276 9,800 9,800 Hire Purchase Interest 31/12/96 P/L 800 31/12/96 HP Creditor 800

Balance Sheet as at 31 Dec (Extract) 96 Fixed Assets 9000 Vehicle Less Pro for Dep Current Liabilities HP Creditor 900 8100 1896 2524-628 Long Term Liabilities HP Creditor 4380 6276-1896

Hire purchase Creditor (Grace Ltd) 1/1/96 Bank-deposit 1,000 1/1/96 Vehicle 9,000 31/12 Bank-instalment 2,524 31/12 HP Interest 800 31/12 Balance c/d 6,276 9,800 9,800 31/12 Bank-instalment 2,524 1/1/97 Balance b/d 6,276 31/12 HP Interest (6276*10%) 628 31/12 Balance 4,380 6,904 6,904 Hire Purchase Interest 31/12/97 P/L 628 31/12/97 HP Creditor 628

Balance Sheet as at 31 Dec (Extract) 97 96 Fixed Assets 9000 9000 Vehicle Less Pro for Dep Current Liabilities HP Creditor 900 1800 8100 7200 1896 2086 2524-438 Long Term Liabilities HP Creditor 2294 4380 4380-2086

Hire purchase Creditor (Grace Ltd) 1/1/96 Bank-deposit 1,000 1/1/96 Vehicle 9,000 31/12 Bank-instalment 2,524 31/12 HP Interest 800 31/12 Balance c/d 6,276 9,800 9,800 31/12 Bank-instalment 2,524 1/1/97 Balance b/d 6,276 31/12 Hp Interest 628 31/12 Balance 4,380 6,904 6,904 31/12 Bank-instalment 2,524 1/1/98 Balance b/d 4,380 31/12 Balance 2,294 31/12 HP interest(4380*10%) 438 4,818 4,818 Hire Purchase Interest 31/12/98 P/L 438 31/12/98 HP Creditor 438

Balance Sheet as at 31 Dec (Extract) 98 97 96 Fixed Assets 9000 9000 9000 Vehicle Less Pro for Dep Current Liabilities HP Creditor 900 2700 1800 8100 7200 6300 2086 1896 2294 2524-230 Long Term Liabilities HP Creditor - 2294 4380 2294-2294

Hire purchase Creditor (Grace Ltd) 1/1/96 Bank-deposit 1,000 1/1/96 Vehicle 9,000 31/12 Bank-instalment 2,524 31/12 HP Interest 800 31/12 Balance c/d 6,276 9,800 9,800 31/12 Bank-instalment 2,524 1/1/97 Balance b/d 6,276 31/12 Balance 4,380 31/12 Hp Interest 628 6,904 6,904 31/12 Bank-instalment 2,524 1/1/98 Balance b/d 4,380 31/12 Balance 2,294 31/12 HP interest(4380*10%) 438 4,818 4,818 31/12 Bank-instalment 2,524 1/1/99 Balance b/d 2294 31/12 HP interest(2294*10%) 230 2524 2524 Hire Purchase Interest 31/12/99 P/L 230 31/12/99 HP Creditor 230

Balance Sheet as at 31 Dec (Extract) 98 99 97 96 Fixed Assets 9000 9000 9000 9000 Vehicle Less Pro for Dep Current Liabilities HP Creditor 3600 900 2700 1800 8100 7200 6300 5400 - 2086 1896 2294 Long Term Liabilities HP Creditor - - 2294 4380

Interest Suspense Method • Interest is recorded all together at the beginning of hire purchase agreement and charge proportionally to the profit and loss account every year.

Example • Refer to textbook P.24

Example 6 • ABC Ltd. purchased a vehicle from Grace Ltd. on 1 Jan 1996 on HP agreement. The details were as follows • Cash price $9000 • Down payment $1000 • HP Price $11096 • Nominal rate of interest 10% on outstanding balance • Four equal annual instalments • First due 31 Dec 1996 • Depreciation 10% on cost • Using (a) the progress interest charge system and (b) interest suspense method, show transactions in books of ABC Ltd.

Answer (b): Total HP interest= HP price – Cash Price = 11096 – 9000 = 2096 Equal instalments = (11096 –1000)/4 =2524

Hire purchase Creditor (Grace Ltd) 1/1/96 Bank-deposit 1,000 1/1/96 Vehicle 9,000 31/12 Bank-instalment 2,524 1/1/96 HP Interest Suspense 2096 (11096-9000) 31/12 Balance c/d 7572 9,800 9,800 HP Interest Suspense 31/12/96 HP Interest 800 (9000-1000)*10% 1/1/96 HP Creditor 2096 31/12/96 Bal c/d 1296 2096 2096 Hire Purchase Interest 31/12/96 P/L 800 31/12/96 HP suspense 800

Balance Sheet as at 31 Dec (Extract) 96 Current Liabilities HP Creditor 2524 Less HP interest suspense 628 1896 (7572-1296)*10% 7572-2524 Long Term Liabilities HP Creditor 5048 668 Less HP interest suspense 1296-628 4380

Hire purchase Creditor (Grace Ltd) 1/1/96 Bank-deposit 1,000 1/1/96 Vehicle 9,000 31/12 Bank-instalment 2,524 1/1/96 HP Interest Suspense 2096 31/12 Balance c/d 7572 9,800 9,800 31/12 Bank-instalment 2,524 1/1/97 Balance b/d 7572 31/12 Balance c/d 5048 6,904 6,904

HP Interest Suspense 31/12/96 HP Interest 800 (9000-1000)*10% 1/1/96 HP Creditor 2096 31/12/96 Bal c/d 1296 2096 2096 31/12/97 HP Interest 628 (7572-1296)*10% 1/1/97 Bal b/d 1296 31/12/97 Bal c/d 668 2096 2096 Hire Purchase Interest 31/12/98 P/L 628 31/12/97 HP Creditor 628

Balance Sheet as at 31 Dec (Extract) 96 97 Current Liabilities HP Creditor 2524 2524 438 Less HP interest suspense 628 1896 2086 (5048-668)*10% 5048-2524 Long Term Liabilities HP Creditor 2524 5048 668 230 Less HP interest suspense 4380 2294 668-438

Hire purchase Creditor (Grace Ltd) 1/1/96 Bank-deposit 1,000 1/1/96 Vehicle 9,000 31/12 Bank-instalment 2,524 1/1/96 HP Interest Suspense 2096 31/12 Balance c/d 7572 9,800 9,800 31/12 Bank-instalment 2,524 1/1/97 Balance b/d 7572 31/12 Balance c/d 5048 6,904 6,904 31/12 Bank-instalment 2,524 1/1/98 Balance b/d 5048 31/12 Balance c/d 2524 4,818 4,818

HP Interest Suspense 31/12/96 HP Interest 800 (9000-1000)*10% 1/1/96 HP Creditor 2096 31/12/96 Bal c/d 1296 2096 2096 31/12/97 HP Interest 628 (7572-1296)*10% 1/1/97 Bal b/d 1296 31/12/97 Bal c/d 668 2096 2096 31/12/98 HP Interest 438 (5048-668)*10% 1/1/98 Bal b/d 668 31/12/98 Bal c/d 230 2096 2096 Hire Purchase Interest 31/12/98 P/L 438 31/12/98 HP Creditor 438