Swaps Chapter 6

Swaps Chapter 6. SWAPS Swaps are a form of derivative instruments. Out of the variety of assets underlying swaps we will cover: INTEREST RATES SWAPS, CURRENCY SWAPS, COMMODITY SWAPS, EQUITY SWAPS and BASIS SWAPS.

Swaps Chapter 6

E N D

Presentation Transcript

SWAPS Swaps are a form of derivative instruments. Out of the variety of assets underlying swaps we will cover: INTEREST RATES SWAPS, CURRENCY SWAPS, COMMODITY SWAPS, EQUITY SWAPS and BASIS SWAPS.

SWAPSA SWAP is a contract between two parties for an exchange of cash flows during some time period. The cash flows are determined based on the UNDERLYING ASSET

It follows that a swap involves 1. Two parties 2. An underlying asset 3. Cash flows 4. A payment schedule 5. An agreement as to how to resolve problems

1. Two parties: • The two parties in a swap are labeled as party and counterparty. • They may arrange the swap directly or indirectly. • In the latter case, there are two swaps, each between one of the parties and the swap dealer.

2. The Underlying asset is the basis for the determination of the cash flows. It is almost never exchanged by the parties. Examples: USD100,000,000, GBP50,000,000, 50,000 barrels of crude oil An equity index

2. The Underlying asset is called the NOTIONAL AMOUNT Or The PRINCIPAL Because it only serves to determine the cash flows. Neither party needs to own it and it almost never changes hands.

3. The cash flows may be of two types: a fixed or a floating cash flow. Fixed interest rate vs. Floating interest rate Fixed price Vs. Market price

3. The cash flows The interest rates, fixed or floating, multiply the notional amount in order to determine the cash flows. Ex: ($10M)(.07)=$700,000; Fixed. ($10M)(Lt+30bps); Floating. The price, fixed or market, multiply the commodity notional amount in order to determine the cash flows. If the underlying asset are 100,000 barrels of oil: Ex: (100,000)($24,75) = $2,475,000; Fixed. (100,000)(St ); Floating.

4. The payments are always net. The contract determines the cash flows timing as annual, semiannual or monthly, etc. Every payment is the net of the two cash flows

5. How to resolve problems: Swaps are Over The Counter (OTC) agreements. Therefore, the two parties always face credit risk operational risk, etc. Moreover, liquidity issues such as getting out of the agreement, default possiblilities, selling one side of the contract, etc., are frequently encountered problems.

Converting a liability from fixed rate to floating rate floating rate to fixed rate Converting an investment from fixed rate to floating rate floating rate to fixed rate Typical Uses of anInterest Rate Swap

Why SWAPS? The goals of entering a swap are: 1. Cost saving. 2. Changing the nature of cash flow each party receives or pays from fixed to floating and vice versa.

INTEREST RATE SWAPSExample:Plain VanillaFixed for Floating rates swapA swap is to begin in two weeks.Party A will pay a fixed rate 7.19% per annum on a semi-annual basis, and will receive the floating rate: six-month LIBOR + 30bps from from Party B. The notional principal is EUR35million. The swap is for five years.Two weeks later, the six-month LIBOR rate is 6.45% per annum.

The fixed rate in a swap is usually quoted on a semi-annual bond equivalent yield basis. Therefore, the amount that is paid every six months is: This calculation is based on the assumption that the payment is every 182 days.

The floating side is quoted as a money market yield basis. Therefore, the first payment is: Other future payments will be determined every 6 months by the six-month LIBOR at that time.

7.19% Party A Party B LIBOR + 30 bps As in any SWAP, the payments are netted. In this case, the first payment is: Party A pays Party B the net difference: EUR1,254,802.74 - EUR1,194,375.00 = EUR60,427.74.

Another Example of a “Plain Vanilla” Interest Rate Swap • An agreement by Microsoft to receive 6-month LIBOR & pay a fixed rate of 5% per annum every 6 months for 3 years on a notional principal of USD100 million • Next slide illustrates cash flows

The principal amount …………… USD100.000.000. The cash flows are………………... semiannual 5% FIXED SWAP DEALER MICROSOFT 6-month LIBOR

Cash Flows to Microsoft(See Table 6.1, page 127) ---------Millions of USD--------- LIBOR FLOATING FIXED Net Date Rate Cash Flow Cash Flow Cash Flow Mar.5, 2001 4.2% Sept. 5, 2001 4.8% +2.10 –2.50 –0.40 Mar.5, 2002 5.3% +2.40 –2.50 –0.10 Sept. 5, 2002 5.5% +2.65 –2.50 +0.15 Mar.5, 2003 5.6% +2.75 –2.50 +0.25 Sept. 5, 2003 5.9% +2.80 –2.50 +0.30 Mar.5, 2004 6.4% +2.95 –2.50 +0.45

Intel and Microsoft (MS) Transform a Liability(Figure 6.2, page 128) 5% 5.2% MS Intel LIBOR+0.1% LIBOR

SWAP DEALER is Involved(Figure 6.4, page 129) 4.985% 5.015% 5.2% Intel SD MS LIBOR+0.1% LIBOR LIBOR

Intel and Microsoft (MS) Transform an Asset(Figure 6.3, page 128) 5% 4.7% Intel MS LIBOR-0.25% LIBOR

SWAP DEALER is Involved(See Figure 6.5, page 129) 4.985% 5.015% 4.7% SD MS Intel LIBOR-0.25% LIBOR LIBOR

These examples illustrate five points: 1. In interest rate swaps, payments are netted. In the example, Party A sent Party B a payment for the net amount. 2. In an interest rate swap, the principal amount is not exchanged. This is why the term “notional principal” is used. 3. Party A is exposed to the risk that Party B might default. Conversely, Party B is exposed to the risk of Party A defaulting. If one party defaults, the swap usually terminates.

4. On the fixed payment side, a 365-day year is used, while on the floating payment side, a 360-day year is used. The number of days in the year is one of the issues specified in the swap contract. 5. Future payments are not known in advance, because they depend on future realizations of the Six-month LIBOR. Estimates of future LIBOR values are obtained from LIBOR yield curves which are based on Euro Strip of Euro dollar futures strips.

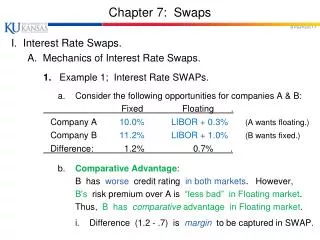

The Comparative Advantage ArgumentA firm has an ABSOLUTE ADVANTAGE if it can obtain better rates in both the fixed and the floating rate markets.Firm A has a RELATIVE ADVANTAGE in one market if:the difference between what firm A pays more than firm B in the floating rate (fixed rate) market is less than the difference between what firm A pays more than firm B in the fixed rates (floating rate) market.

Example:A FIXED FOR FLOATING SWAP • Two firms need EUR10M financing for projects. They face the following interest rates: • PARTYFIXED RATEFLOATING RATE • F1 : 15% LIBOR + 2% • F2 : 12% LIBOR + 1% • F2 HAS ABSOLUTE ADVANTAGE in both markets, but F2 has RELATIVE ADVANTAGE only in the market for fixed rates. WHY? The difference between what F1 pays more than F2 in floating rates, (1%), is less than the difference between what F1 pays more than F2 in fixed rates, (3%).

Now, suppose that the firms decide to enter a FIXED for FLOATING swap based on the notional of EUR10.000.000. The cash flows: Annual payments to be made on the first business day in March for the next five years. The SWAP always begins with each party borrowing capital in the market in which it has a RELATIVE ADVANTAGE.Thus: F1 borrows S EUR10,000,000 in the market for floating rates, I.e., for LIBOR + 2% for 5 years. F2 borrows EUR10,000,000 in the market for fixed rates, I.e., for 12%. NOW THE TWO PARTIES EXCHANGE THE TYPE OF CASH FLOWS BY ENTERING THE SWAP FOR FIVE YEARS.

A fundamental implicit assumption: The swap will take place only if F1 wishes to borrow capital for a FIXED RATE, While F2 wishes to borrow capital for a FLOATING RATE. That is, both firms want to change the nature of their payments.

FIXED FOR FLOATING SWAP • A DIRECT SWAP: • FIRMFIXED RATE FLOATING RATE • F1 15% LIBOR + 2% • F2 12% LIBOR + 1% LIBOR LIBOR+2% 12% F2 F1 12% The result of the swap: F1 pays fixed 14%, better than 15%. F2 pays floating LIBOR, better than LIBOR + 1%

2.AN INDIRECT SWAP with a SWAP DEALER: • FIRMFIXED RATEFLOATING RATE • F1 15% LIBOR + 2% • F2 12% LIBOR + 1% SD L+25bps L L + 2% 12% F2 F1 12% 12,25% F1 pays 14,25% fixed: Better than 15%. F2 pays L+25bps : Better than L+1%. The swap dealer gains 50 bps = $50,000.

Notice that the two swaps presented above are two possible contractual agreements. The direct, as well as the indirect swaps, may end up differently, depending on the negotiation power of the parties involved. Nowadays, it is very probable for swap dealers to be happy with 10 basis points. In the present example, another possible swap arrangement is: L+5bp L L+2% 12% F2 F1 SD 12% 12%+5bp Clearly, there exist many other possible swaps between the two firms in this example.

Warehousing In practice, a swap dealer intermediating (making a market in) swaps may not be able to find an immediate off-setting swap. Most dealers will warehouse the swap and use interest rate derivatives to hedge their risk exposure until they can find an off-setting swap. In practice, it is not always possible to find a second swap with the same maturity and notional principal as the first swap, implying that the institution making a market in swaps has a residual exposure. The relatively narrow bid/ask spread in the interest rate swap market implies that to make a profit, effective interest rate risk management is essential.

EXAMPLE: A RISK MANAGEMENT SWAP BONDS MARKET FL1 = 6-MONTH BANK RATE. FL2 = 6-MONTH LIBOR. FL1 LOAN 10% SWAP DEALER A BANK FL2 LOAN 12% FIRM A BORROWS AT A FIXED RATE FOR 5 YEARS

THE BANK’S CASH FLOW: 12% - FLOATING1 + FLOATING2 – 10% = 2% + SPREAD Where the SPREAD = FLOATING2 - FLOATING1 RESULTS THE BANK EXCHANGES THE RISK ASSOCIATED WITH THE DIFFERENCE BETWEEN FLOATING1 and 12% WITH THE RISK ASSOCIATED WITH THE SPREAD = FLOATING2 - FLOATING1. The bank may decide to swap the SPREAD for fixed, risk-free cash flows.

EXAMPLE: A RISK MANAGEMENT SWAP BOND MARKET FL1 10% SWAP DEALER A BANK FL2 FL2 FL1 SWAP DEALER B 12% FIRM A

THE BANK’S CASH FLOW: 12% - FL1 + FL2 – 10% + (FL1 - FL2 ) = 2% RESULTS THE BANK EXCHANGES THE RISK ASSOCIATED WITH THE SPREAD = FL2 - FL1 WITH A FIXED RATE OF 2%. THIS RATE IS A FIXED RATE!

PRICING SWAPS The swap coupons (payments) for short-dated fixed-for-floating interest rate swaps are routinely priced off the Eurodollar futures strip (Euro strip). This pricing method works provided that: (1)Eurodollar futures exist. (2)The futures are liquid. As of June 1992, three-month Eurodollar futures are traded in quarterly cycles - March, June, September, and December - with delivery (final settlement) dates as far forward as five years. Most times they are liquid out to at least four years.

The Euro strip is a series of successive three-month Eurodollar futures contracts. While identical contracts trade on different futures exchanges, the International Monetary Market (IMM) is the most widely used. It is worth mentioning that the Eurodollar futures are the most heavily traded futures anywhere in the world. This is partly as a consequence of swap dealers' transactions in these markets. Swap dealers synthesize short-dated swaps to hedge unmatched swap books and/or to arbitrage between real and synthetic swaps.

Eurodollar futures provide a way to do that. The prices of these futures imply unbiased estimates of three-month LIBOR expected to prevail at various points in the future. Thus, they are conveniently used as estimated rates for the floating cash flows of the swap. The swap fixed coupon that equates the present value of the fixed leg with the present value of the floating leg based on these unbiased estimates of future values of LIBOR is then the dealer’s mid rate.

The estimation of a “fair” mid rate is complicated a bit by the facts that: • The convention is to quote swap coupons for generic swaps on a semiannual bond basis, and • The floating leg, if pegged to LIBOR, is usually quoted on a money market basis. Note that on very short-dated swaps the swap coupon is often quoted on a money market basis. For consistency, however, we assume throughout that the swap coupon is quoted on a bond basis.

The procedure by which the dealer would obtain an unbiased mid rate for pricing the swap coupon involves three steps. The first step: Use the implied three-month LIBOR rates from the Euro strip to obtain the implied annual effective LIBOR for the full-tenor of the swap. The second step: Convert this full-tenor LIBOR to an effective rate quoted on an annual bond basis. The third step: Restate this effective bond basis rate on the actual payment frequency of the swap.

NOTATIONS:The swap is an m-months or m/12 years swap. The swap is to be priced off three-month Eurodollar futures, thus, pricing requires n sequential futures series. n = m/3; m = 3n. Step 1: Use the futures Euro strip to Calculate the implied effective annual LIBOR for the full tenor of the swap:

N(t) is the total number of days covered by the swap, which is equal to the sum of the actual number of days in the succession of Eurodollar futures. Step 2: Convert the full-tenor LIBOR, which is quoted on a money market basis, to its fixed-rate equivalent FRE(0,3n), which is stated as an effective annual rate on an annual bond basis. This simply reflects the different number of days underlying bond basis and money market basis:

Step 3: Restate the fixed-rate on the same payment frequency as the floating leg of the swap. The result is the swap coupon, SC. Let f denote the payment frequency, then the coupon swap is given by:

Example:For illustration purposes let us observe Eurodollar futures settlement prices on April 24, 2001. Eurodollar Futures Settlement Prices April 24,2001. CONTRACTPRICELIBORFORWARDDAYS JUN01 95.88 4.12 0,3 92 SEP01 95.94 4.06 3,6 91 DEC01 95.69 4.31 6,9 90 MAR02 95.49 4.51 9,12 92 JUN02 95.18 4.82 12,15 92 SEP02 94.92 5.08 15,18 91 DEC02 94.64 5.36 18,21 91 MAR03 94.52 5.48 21,24 92 JUN03 94.36 5.64 24,27 92 SEP03 94.26 5.74 27,30 91 DEC03 94.11 5.89 30,33 90 MAR04 94.10 5.90 33,36 92 JUN04 94.02 5.98 36,39 92 SEP04 93.95 6.05 39,42 91

These contracts imply the three-month LIBOR (3-M LIBOR) rates expected to prevail at the time of the Eurodollar futures contracts’ final settlement, which is the third Wednesday of the contract month. By convention, the implied rate for three-month LIBOR is found by deducting the price of the contract from 100. Three-month LIBOR for JUN 01 is a spot rate, but all the others are forward rates implied by the Eurodollar futures price. Thus, the contracts imply the 3-M LIBOR expected to prevail three months forward, (3,6) the 3-M LIBOR expected to prevail six months forward, (6,9), and so on. The first number indicates the month of commencement (i.e., the month that the underlying Eurodollar deposit is lent) and the second number indicates the month of maturity (i.e., the month that the underlying Eurodollar deposit is repaid). Both dates are measured in months forward.

In summary, the spot 3-M LIBOR is denoted r 0,3 , the corresponding forward rates are denoted r3,6, r6,9, and so on. Under the FORWARD column, the first month represents the starting month and the second month represents the ending month, both referenced from the current month, JUNE, which is treated as month zero. Eurodollar futures contracts assume a deposit of 91 days even though any actual three-month period may have as few as 90 days and as many as 92 days. For purposes of pricing swaps, the actual number of days in a three-month period is used in lieu of the 91 days assumed by the futures. This may introduce a very small discrepancy between the performance of a real swap and the performance of a synthetic swap created from a Euro strip.

Suppose that we want to price a one-year fixed-for-floating interest rate swap against 3-M LIBOR. The fixed rate will be paid quarterly and, therefore, is quoted quarterly on bond basis. We need to find the fixed rate that has the same present value (in an expected value sense) as four successive 3-M LIBOR payments. Step 1: The one-year implied LIBOR rate, based on k =360/365, m = 12, n = 4 and f=4 is: