Download

1 / 101

1.04k likes | 1.38k Views

ECONOMICS. What Does It Mean To Me?. FEDERAL RESERVE SYSTEM and MONETARY POLICY *History of Banking *Structure of the Fed *Nominal v. Real Interest Rates. HISTORY OF BANKING. 1780s. No national standard; each state responsible for it’s own currency. 1791.

E N D

ECONOMICS What Does It Mean To Me? FEDERAL RESERVE SYSTEM and MONETARY POLICY *History of Banking *Structure of the Fed *Nominal v. Real Interest Rates

HISTORY OF BANKING 1780s No national standard; each state responsible for it’s own currency. 1791 Charter signed for FIRST BANK OF THE UNITED STATES. (expired 1811) 1811- 1816 Period of instability; extreme recessions and peaks. 1816 SECOND BANK OF THE UNITED STATES. (expired 1836)

HISTORY OF BANKING President Andrew Jackson vetoes the recharter of the Second Bank of US 1832 1838-1863 Free Banking Era: Anyone may engage in banking upon compliance with charter requirements (wildcat banking) 1863 & 1864 National Banking Acts of 1863 & 1864: established national currency. 1865 Tax placed on bank notes; all national banks under federal supervision. (some continued under state charters)

HISTORY OF BANKING Panic of 1907 (et.al.) caused by overexpansion of credit, low bank reserves 1907 1913 The Fed was created after a series of bank failures convinced Congress that the United States needed a central bank to ensure the health of the nation’s banking system. 1929 Great Depression. (lowest = 1933) Over 5000 banks went bankrupt. 1933 President Roosevelt restores confidence in the banking system by passing the FDIC.

HISTORY OF BANKING 1940s- 1960s Period of government regulation and economic stability. Late60s -1970s New Laws regarding responsibilities of banks and consumers. 1980s Deregulation; S & Ls bankrupt. mid80s ATM banking; online information gives more stability as 24-hour cash availabilty and account information is available.

In 1913, Congress established the FEDERAL RESERVE SYSTEM The Federal Reserve system consists of 12 Banks for 12 districts in different parts of the country, each being a cooperative of the “member” banks.

For most practical purposes, “THE FED” is a government agency, however, it is set up separate and apart from the U.S. government.

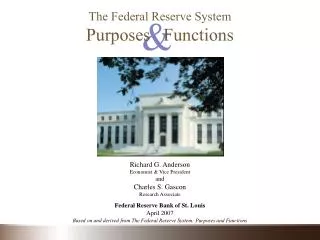

L to R: FRB of Boston, Minneapolis, and Dallas. Research for industrially advanced countries indicates that the more independent the central bank, the lower the average rate of inflation.

FEDERAL OPEN MARKET COMMITTEE (FOMC) (12) FEDERAL ADVISORY BOARD (12) BOARD OF GOVERNORS (7) 12 member banks ABoston F Atlanta KDallas GChicago LSan Francisco CPhiladelphia ERichmond IMinneapolis J Kansas City DCleveland H St. Louis BNew York

FEDERAL OPEN MARKET COMMITTEE (FOMC) (12) FEDERAL ADVISORY BOARD (12) BOARD OF GOVERNORS (7) 12 member banks KDallas LSan Francisco F Atlanta GChicago ABoston IMinneapolis J Kansas City H St. Louis BNew York ERichmond CPhiladelphia DCleveland

FEDERAL OPEN MARKET COMMITTEE (FOMC) (12) FEDERAL ADVISORY BOARD (12) BOARD OF GOVERNORS (7) 12 member banks ABoston F Atlanta KDallas GChicago LSan Francisco CPhiladelphia ERichmond IMinneapolis J Kansas City DCleveland H St. Louis BNew York

The excess profits of the Fed go to the U.S. Treasury. • The BOARD OF GOVERNORS are appointed by the President with the consent of Congress. However, neither the President nor Congress has the power to control the actions of the Federal Reserve.

For those appointed to the Fed: • A full term is fourteen years • One term begins every two years on February 1st of even-numbered years. (staggered terms) • A member who serves a full term may not be reappointed.

The CHAIRMAN and VICE-CHAIRMAN: • Are named by the President from among the members and are confirmed by the Senate. • They serve four year terms • A member’s term on the Board is not affected by his or her status as Chairman or Vice-Chairman.

FEDERAL OPEN MARKET COMMITTEE (FOMC) (12) FEDERAL ADVISORY BOARD (12) BOARD OF GOVERNORS (7) 12 member banks ABoston F Atlanta KDallas GChicago LSan Francisco CPhiladelphia ERichmond IMinneapolis J Kansas City DCleveland H St. Louis BNew York

The FEDERAL OPEN MARKET COMMITTEE (FOMC) • Is composed of the seven members of the Board of Governors and five Reserve Bank presidents. • The president of the FRB of New York serves on a continuous basis. • The president of the other Reserve Banks serve one-year terms on a rotating basis beginning January 1 of each year.

Traditionally, the Chairman of the Board of Governors is elected Chairman of the FOMC and the president of the FRB of New York is elected Vice-Chairman. • By law, the FOMC must meet at least four times a year in Washington DC, however, since 1980, eight regularly scheduled meetings are held per year.

At each regularly scheduled meeting, the Committee votes on the monetary policy to be carried out during the interval between meetings. They set policy regarding the buying and selling of government securities, such as bills, notes, and bonds. At least twice per year, the Committee also votes on its long-run policy objectives for growth in key money and debt aggregates.

Twice a year, as required by the Humphrey-Hawkins Act of 1978, the Board submits a written report to Congress on the state of the economy and the course of monetary policy, and the Chairman is called on to testify on this report.

The Purposes and Functions of the Federal Reserve System Federal Reserve System Payments System Supervision & Regulation Monetary & Economic Policy

Three Primary Functions of the Fed • Regulates banks to ensure they follow federal laws intended to promote safe and sound banking practices. • Acts as a banker’s bank, making loans to banks and as a lender of last resort. • Conducts monetary policyby controlling the money supply.

Federal Reserve Banks serve as bankers’ banks. In our system, “member” banks have deposits in the Federal Reserve, and these deposits are part of the member bank’s reserves.

The twelve Federal Reserve Banks Act as fiscal agents for the Federal government; Provide for the collection of checks; Hold the deposits of commercial banks.

The Purposes and Functions of the Federal Reserve System Federal Reserve System Payments System Supervision & Regulation Monetary & Economic Policy

What Does the Fed Do? • Bartering (??? BC) • Precious metals/gems • Precious coins • Coins • Currency • Checks (1600s) • Electronic funds transfer (1918) • Credit cards (1960s) • Debit cards • Stored value cards Payments System

Since we have many banks, a key problem is to assure that a check written on one bank will be accepted as a deposit in another bank. The Federal Reserve system assures this by controlling the reserves and CLEARING CHECKS and deposits among the different banks.

CHECK CLEARING is another function of the Federal Reserve. 1) Suppose you write a check in Portland, Oregon 2) The retailer will send your check to their bank. 3) The bank will send the check to THEIR Federal Reserve Bank, in this case, in San Francisco. 5) The Atlanta Federal Reserve Bank then sends the check to your bank in Coral Springs. 4) The San Francisco Bank sends the check to the Atlanta Bank based on the tracking number on the check.

What Role Does the Fed Play in the Payments System? Items Total Amt. Average (millions) ($billions) Trans Amt Currency 24,200 $719.9 NA Check 14,325 $14,593 $1,018.85 ACH 7,427 $15,457 $2,081 Fedwire 126 $469,899 $2,729,000 Funds *ACH: Automated Clearing House (direct dep, SS paym)

Number of Electronic Payments in 2000 and 2003 (Billions of Items)

Check 21 • Substitute checks • Make sure you have enough money in your account to cover the checks that you write. • Be sure to read and understand your rights to resolve errors under state and federal laws.

The Purposes and Functions of the Federal Reserve System Federal Reserve System Payments System Supervision & Regulation Monetary & Economic Policy

There are 3 ways the Fed conducts monetary policy: • Raise or lower interest rates • Raise or lower the reserve requirement • Buy or sell Treasury bills on the open market

During periods of INFLATION, the Federal Reserve needs to take money OUT of the economy or decrease the money supply, to make the economy SLOW DOWN. To accomplish this, the Fed will • Raise interest rates • Raise the reserve requirement • Sell Treasury Bills

Let’s examine why this tight money policy (contractionary) is necessary:

RAISING INTEREST RATES will cause YOU to pay more for your mortgage or car loans. It causes YOU to have less money to spend on other goods. When you spend less, businesses make less profit. This removes money and credit from the economy, slowing it down.

RAISING THE RESERVE REQUIREMENT will require banks to hold more cash in reserve instead of loaning it out to the public. This removes cash and the credit available to spend, lowering profits for businesses, and slowing down the economy.

SELLING TREASURY BILLS will cause people to spend cash for the investment which will yield them interest. This removes cash and the credit available to spend on goods, lowering profits for businesses, and slowing down the economy. T-Bills are sold in denominations of $1000, $10,000 and higher.

When the economy is growing too slowly or in a RECESSION, the Fed needs to put money INTO the economy or increase the money supply, to make the economy SPEED UP. To accomplish this, the Fed will • Lower interest rates • Lower the reserve requirement • Buy Treasury Bills

Let’s examine why this easy money policy(expansionary) is necessary:

LOWERING INTEREST RATES will cause mortgages and car loans to make your payments cheaper. It causes YOU to have more money to spend on other goods. When you spend more, businesses make more profit. This adds money and credit to the economy, making it grow at a faster pace.