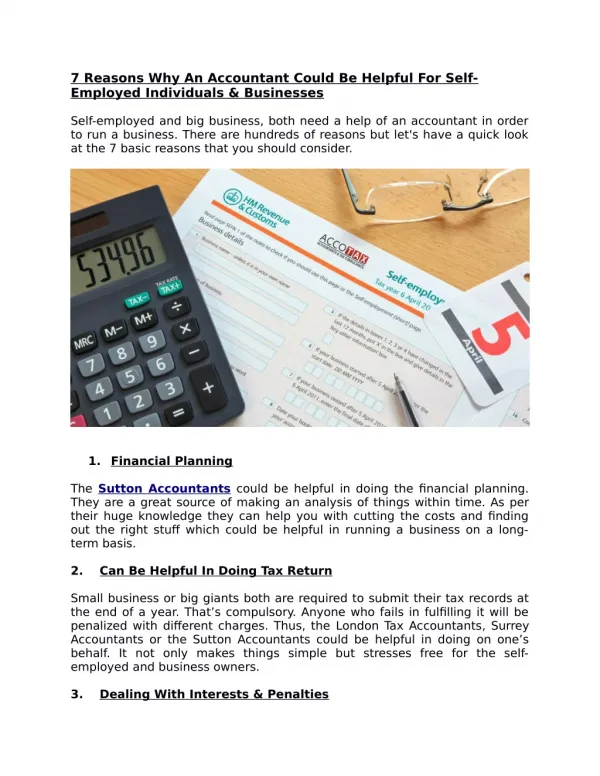

1 / 3

0 likes | 17 Views

Retirement management tools for self-employed individuals offer essential solutions for planning and securing financial futures. These tools encompass a range of options, including retirement savings accounts like SEP IRAs and solo 401(k)s, which allow self-employed individuals to contribute and grow their funds tax-deferred. Additionally, investment platforms and financial planning software provide insights and guidance for optimizing retirement savings strategies.

E N D

Retirement Management Tools for Self-Employed Individuals Planning for retirement requires proactive strategies and the right tools for self-employed individuals to ensure financial security in later years. Unlike employees with access to employer-sponsored retirement plans, self-employed individuals must take the initiative to build their retirement nest egg. Fortunately, several retirement management tools are tailored to the needs of freelancers, entrepreneurs, and independent contractors. This article explores some of the best retirement management tools available to self-employed individuals, highlighting their features, benefits, and how they can be utilized effectively. Individual Retirement Accounts (IRAs)

● Traditional IRA A Traditional IRA is a tax-advantaged retirement account allowing individuals to contribute pre-tax dollars, potentially reducing their taxable income. Contributions grow tax-deferred until withdrawal during retirement, at which point they are taxed as ordinary income. For self-employed individuals, Traditional IRAs offer flexible contribution amounts and investment choices. However, contribution limits apply, and early withdrawals may incur penalties. ● Roth IRA A Roth IRA is another popular retirement savings option, offering tax-free growth and withdrawals in retirement. Unlike Traditional IRAs, contributions to Roth IRAs are made with after-tax dollars, but qualified withdrawals, including earnings, are tax-free. Roth IRAs benefit self-employed individuals expecting a higher tax bracket during retirement. Like Traditional IRAs, contribution limits apply, but Roth IRAs also have income eligibility restrictions. ● Simplified Employee Pension (SEP) IRA A SEP IRA is designed for self-employed individuals and small business owners, offering a straightforward and tax-efficient way to save for retirement. Contributions to a SEP IRA are tax-deductible, and earnings grow tax-deferred until withdrawal. SEP IRAs allow for higher contribution limits than Traditional and Roth IRAs, making them an attractive option for those with fluctuating incomes or seeking to maximize retirement savings. Additionally, SEP IRAs are easy to set up and administer, requiring minimal paperwork. ● Solo 401(k) or Individual 401(k) Solo 401(k) plans are specifically designed for self-employed individuals with no employees except possibly a spouse. They combine the features of a traditional employer-sponsored 401(k) with the flexibility of a retirement plan for the self-employed. Solo 401(k) plans allow for both employee and employer contributions, enabling individuals to save for retirement while potentially reducing their taxable income. Contribution limits for Solo 401(k) plans are higher than those for IRAs, allowing for more significant retirement savings potential. ● Health Savings Account (HSA) While primarily intended for healthcare expenses, Health Savings Accounts (HSAs) can also serve as retirement savings vehicles for self-employed individuals enrolled in high-deductible health plans (HDHPs). Contributions to an HSA are tax-deductible and grow tax-free, and withdrawals for qualified medical expenses are tax-free. However, after age 65, withdrawals for non-medical expenses are subject to income tax but not penalties, making the HSA a supplemental retirement account. Summary

Planning for retirement as a self-employed individual requires careful consideration and proactive steps to build a secure financial future. Fortunately, several retirement management tools are tailored to the unique needs and circumstances of freelancers, entrepreneurs, and independent contractors. Individual Retirement Accounts (IRAs), including Traditional IRAs and Roth IRAs, offer tax-advantaged savings options with varying benefits depending on individual circumstances. For self-employed individuals with fluctuating income or seeking higher contribution limits, Simplified Employee Pension (SEP) IRAs and Solo 401(k) plans provide flexible and efficient retirement savings solutions. Health Savings Accounts (HSAs) can also serve as supplemental retirement accounts for those enrolled in high-deductible health plans, offering tax advantages for healthcare expenses and future retirement needs. By effectively leveraging these retirement management tools, self-employed individuals can take control of their financial futures and build a retirement nest egg that provides security, independence, and peace of mind. However, consulting with a financial advisor or tax professional is essential to determine the best retirement strategy based on individual goals, risk tolerance, and economic circumstances. Self-employed individuals can enjoy a comfortable and fulfilling retirement with proper planning and the right tools.